there’s a lot happening on social media and this subsidiary financials auditor’s note is the latest after Q2 results

Mangement is quite open in interacting with Investors regarding the allegations, which according to me is a positive sign. If they had something to hide they wouldn’t be open and welcoming.

Also the law firm that is appointed to do the Internal Review is reputable. https://www.skadden.com

Will keep the thread updated as and when I find more.

Disclosure : Invested and Looking to add more

2016 calendar of movies. There is no further bad news, yet its beaten down heavily.

Seems a classic value stock. Disc invested

If it is indeed so, then it can prove to be a multibagger this year given the beating it had taken in the last 4-5 months. It is able to churnout blockbuster movies and I don’t see the trend declining this year.

Hi Sandeep,

However the truth of the matter is accounting frauds, management ethics are a BIG ?

When is Q3 results coming ? Whats up with court cases & credit ratings degradation ? Not much news coming in. Can you throw some light.

Disc: invested

No. result is expected on Feb 15th or so. However, it is not yet announced on BSE website. Expecting some clarification regarding these accounting issues in their con call

Also they are going ahead with aggressive tie ups with bharti airtel, idea, reliance on movie straming+4G packs etc. Seems pretty smart Media Co. but lets wait & watch Q3 , comments by CR agencies & some more info

Main points of contention where markets have doubt are their amortization policy (50% in 1st year and rest evenly spread over 10 years), increasing debtors, sharing of revenues related to eros now between parent and indian subsidiary (as eros now is owned by eros plc).

Management said that they will decrease debtors by march and come up with sharing ratio and some other clarifications by March.

Eros has an enviable position in industry with 3000 titles. Its dominant position can be known by the fact that bajirao released with SRK dilwale. Movie making business has of late become an easy business with strong tailwinds blowing like never before in form of increase disposable incomes, increasing need for entertainment, various ways of monetisation ( eros mostly gets its cost recovered before releasing, digitsation ( genuine and increasing subscription figures helping channels to buy quality content), eros dominant partnership with industry heavy weights. This is a big competitive advantage for eros where no one can just come and take their positon.

Of course, management quality doesn’t look to be top notch but modus operandi doesn’t suggest they are crooks.

I am not worried about results of Q3 as I don’t think they will surprise negatively.

Will request you to dig further as this can be oppurtunity of the year.

Disclosure: Invested but I do take in to account price action as well. So will increase my holding once it starts exhibiting strength.

2 Likes

Just a clarification on the amortisation policy. I think for most big budget movies produced by Eros India, Eros India sells certain theatrical and digital rights to Eros international plc (USA) and 30% is amortised immediately in P&L of Eros India for this transaction. Of the remaining 70%, 60% (not 50%), is amortised in 1st year and rest over 9 years. So effectively, 1st year amortisation is about 30% + 60% of 70% = 72% - which is still a bit aggressive but more on the reasonable side.

I heard this on their latest concall of September 2015 results, towards the end. Please let me know if someone differs and do quote the source of the same.

Sachit

Yes.Eros is in an enviable position as far as the movie production and distribution is concerned. The incident at Goldman Sachs when Buffett took huge position in the company is eerily similar to what Eros is going through now.

Looks like a classic value stock.

I want to give a twist to the oft quoted gem of WB

"When a management with a shoddy reputation tackles a business with a reputation for great economics, it is the reputation of the business that remains intact"- WB.

Any opinions?

I did listen to september concall but couldn’t recall what you write about amortisation (72%). Are you sure about source? Meanwhile, I will listen transcript again.

Yup, sure about the source, and also remember the 72% figure. Although on the slight chance I may have misheard it, I will also listen to the call again.

I can confirm after talking to management it is 72% amortisation.

However, I’m cautious due to the fact that share price has come off after a sudden and substantial rise. That rise coincided with publicity around EROS NOW. Once it became clear that Eros Now is to form part of parent entity, some funds lost interest in domestic entity.Similarly, foreigners are wary of the revenue booking done in India entity etc. Management has promised to streamline the holding structure such that ALL investors participate at ALL levels.That process might take a long time to unfold, however.

Meanwhile, this management has to display good faith by paying regular dividends.The plea that cash is needed to go after growth can be made by almost every listed entity, what is special about Eros? In any case minority shareholders are interested in income, not necessarily interested in empire building a la the promoter.

That being said, valuation is extremely cheap, and I remain invested.

1 Like

Any reason for the spike on 1.2.2016 ??

Eros is a 30 year old company currently being run by second generation entrepreneur. It is one of the largest film studios in India and has deep relationships within the film fraternity. The studio model (releasing multiple films across genres every year) diversifies earnings risk materially.

There seems only moderate risk that the entire accounts are fudged. Management pedigree is not great, but not bad either. Also, the fact that Eros went ahead for a US listing in Nov’15 with fudged accounts seem very remote. That’s like shooting themselves in the foot.

I am confident that once the management focuses on FCF and dividends (as promised last year), the stock will go back to 15-25 PE range which is in line with other similar businesses (Lionsgate in US). Entertainment One Ltd. (eOne) is another similar business listed in Canada at PE of 8.5. The company has a very similar business model as that of Eros. However , there are key differences: eOne operates in mature territories (US, UK, Canada, Benelux countries) where film attendance is falling; in India, box office market is one of the most vibrant globally. Eros at ~8PE seems a steal.

However, we might have to live with some negatives - the reason of low valuation  - until corrected:

- until corrected:

- Complicated share structure

- No/very low/inconsistent dividends

- lack of FCFs

Discl: Invested with 5% allocation

1 Like

I’m finding the following situation not very understandable. Pls. help guys.

Eros on 31-3-2015, Rs. 2704 Cr. is the cash on books as per my reading. At CMP i.e. 153.80 (P/E of 6.17), the Market Cap comes out to be 1439.57.

Which means, that if the company has not entirely squandered cash at hand during this year, we are looking at a heck of a steal @CMP (47% discount to cash on books !!!).

Maybe I’m missing something because it looks too good to be true.

You are missing a lot. Please go thru Balance Sheet and Presentation as on 30-09-2015. They have issued debentures also in Dec. See the rating in respect of debentures. I could have given also the details here but it is not going to help you as an investor. Please develop the habit of drilling deep not wide.

4 Likes

BINGO!! And Yes I’m an Idiot of the first order. 2704 was a figure reported in Lacs, not Crores. Wont happen again, I promise!! Thank You!!

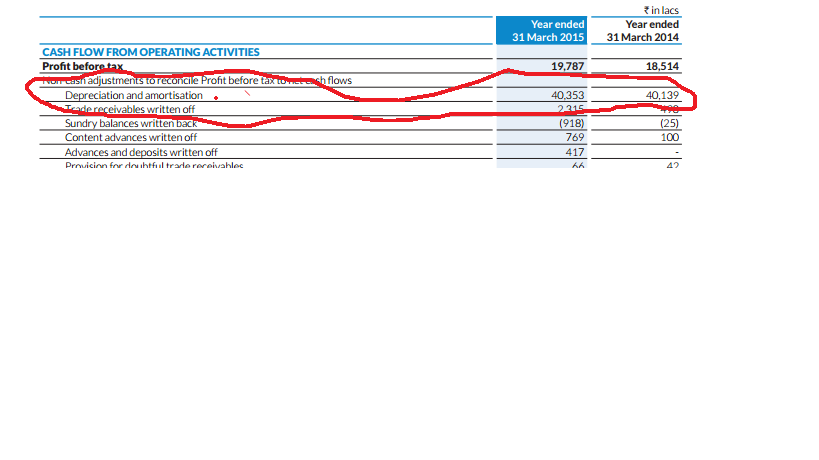

I tried to match the OCF for Eros to the Net Income. On a cumulative basis, Eros OCF is 4x of the Net Income over 05-15. Is this a normal thing?

Net Income 1076.25 Cr

Operating Cash Flow 4226.62 Cr

OCF/NI 392.72%

{kind=link}