FPIs exited. Smart foreign investors. Without getting unemotional, they exited on a profit. Fundamentals will always win.

That’s a very little amount that other FPIs hold. They have entered in Q3 and exited in Q4. I am not sure what have made them to exit in just 1 quarter. At the same time I see HCF increased the stake to 7.19% from 7.16%. Unless fundamentals deteriorate I don’t consider these FIIs exit as a case to worry. Waiting for Q4 results to take further actions/analysis.

“When the tide turns around, we will know who is swimming naked.” ~ Warren Buffet.

If anyone attended the AGM then please share notes from the meeting…

A meeting report from their largest institutional investor ‘Hidden Champions Fund’. This gives an idea into what they do and a kind of scuttlebutt

https://hiddenchampionsfund.com/2018/08/16/aug-updates/

2 Likes

I heard from a friend also on Valuepickr that when he had done scuttlebutt in agricultural fairs, there are many competitors to the company rather than the oligopoly/technology moat suggested by them. Their inability to take prices up also adds credence to this hypothesis.

Comsyn.pdf (1.7 MB)

Commercial Syn Bags Ltd listed on BSE SME platform is in FIBC bag manufacturing with 17000 tonnes capacity. For the half year ended Sept 18, it has reported a PAT of Rs.497 lakh. It has recently commissioned a 3900 tonnes food and pharma grade FIBC plant at Pithampura SEZ which has broken even at ebitda level for six months and will be PAT positive for full year.

Comsyn is expected to report PAT of 11 crs for full year and is available at Rs 49 crs market cap versus EMMBI’s expected PAT of 16 crs and Rs218 crs market cap.

Balance sheet wise too Comsyn has a much stronger and better balance sheet and metrics.

Will do a separate post on Comsyn soon.

Caution:SME Stocks are quite illiquid and have very high spreads.

Disc: am holding Comsyn

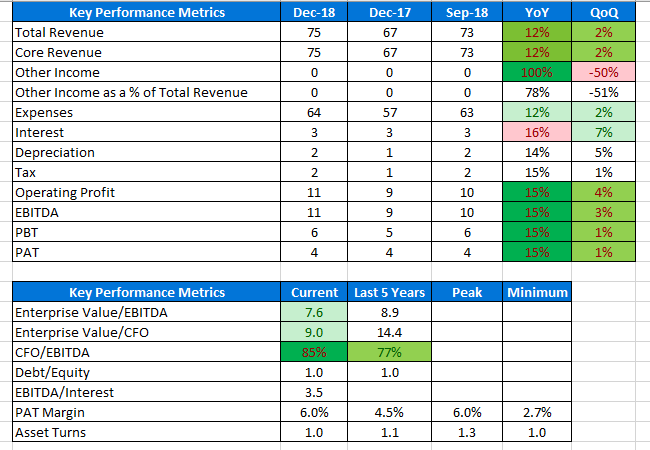

Decent Performance both on revenue and PAT. PAT margin improvement story continues with few BPS gains every quarter

Disc: Invested recently

3 Likes

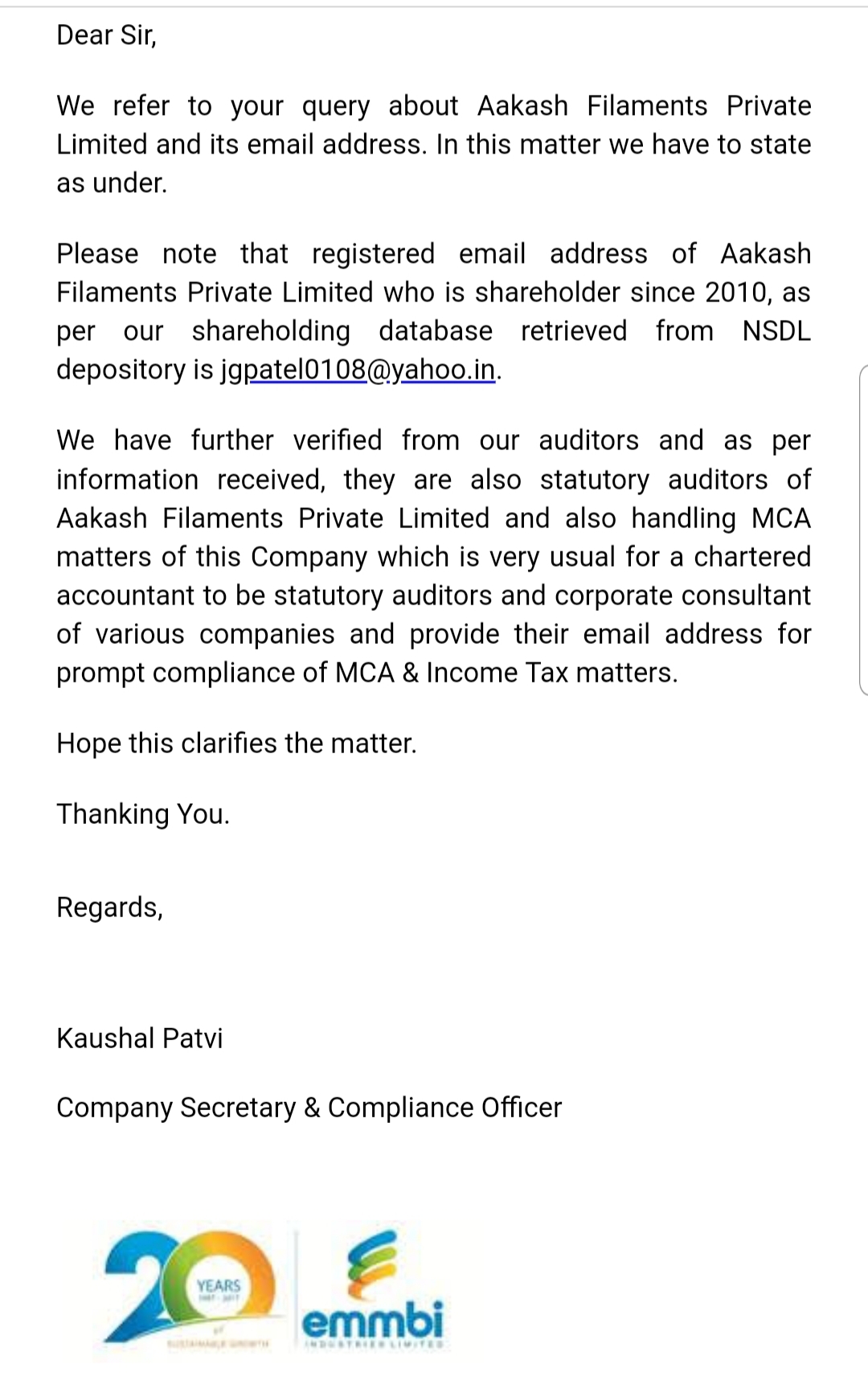

Hi guys, have been tracking this company as the business seems interesting.

Was just going through the shareholding pattern, and AAKASH FILAMENTS PRIVATE LIMITED is listed as a significant public shareholder.

This company shares its registered email ID (rsdaliya@gmail.com) with Emmbi’s auditors - R. DALIYA & ASSOCIATES. This seems rather unusual.

Would anyone have any insights on this?

5 Likes

from what i know auditors are not allowed to hold shares of companies they audit

My two cents…when the stock is down so much price wise …means the market knows more than what we could think off…just a perspective…not invested

For the past few months I started realizing that price reflect first then fundamental start showing most of the time…

I think we should never ever ever generalize and look on case to case basis. Else it would be difficult to justify why hdfc fell 65%, why kotak fell 80%. Why Amazon fell 94%. I get it where are you coming from and there is a merit in your point but that hypothesis needs to be strengthened by patterns, information and analysis beyond price ,specially when whole mid n small cap universe is falling. Coming to this script, overvaluation in mid n small cap stocks including this, fear of interest rate rise, dependence on crude though mgmt says otherways, accounting issues with R&D , overboard marketing by management, climatic conditions are some of the risks we must watch n factor while valuating

4 Likes

Agree…I missed something …wrong thread…my bad… I was putting my view for byke hosp…not for emmbi…I am tracking emmbi too…

Hi guys, got in touch with the company on the question I had earlier.

To their credit, they’ve replied promptly after verifying I was a shareholder.

Explanation seems simple enough, apparently the auditor is common. Not too sure what to make of the whole thing though.

Any views?

2 Likes

I’m new to the boards, so please pardon any errors. There seem to be pretty varied views on this company. One thing that seems odd, is with their Avana venture that is targeted to rural consumers and their growth engine, why is their website only in English. Would one not have local language content that internet-savvy rural users would be able to get to and use? Any insights?

Good point. this concern can be raise during concall or AGM.

Prashant

Emmbi wins the prestigious ‘India SME 100 Award’ and was awarded under India’'s Top MSMEs at the award ceremony recently held in New Delhi.

3 Likes

Its a paid article. Is it possible to get a summary of key/important points?