CONFERENCE CALL - from Capital Markets

Eicher Motors

To broaden the product portfolio, EML would introduce another new bike in CY2017

Eicher Motors (EML)held a conference call on 05 February 2016to discuss the Q4 2015 performance. The call was addressed by Siddharth Lal, Managing Director and CEOand Lalit Malik, CFO.

Key Points from the discussion:

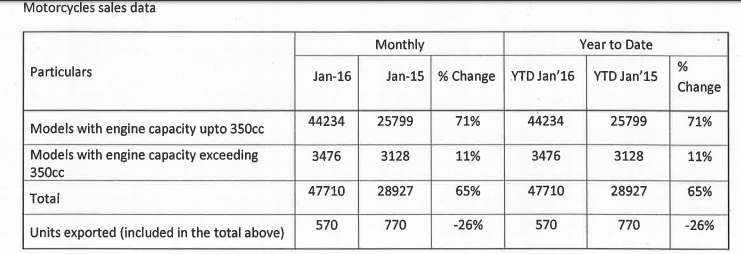

The demand for Royal Enfield bikes continues to remain strong with thecompany taking more orders every month as compared to sales volumes.

VECV volumes continued to improve given the uptick in the MHCV industry on

account of better freight availability and improved fleet operator sentimentsdue to subdued diesel prices. VECV posted second consecutive month ofdouble-digit growth in 4QFY2016.

Eicher is expanding the distribution of its recently introduced “Multix” vehicle.

Royal Enfield (RE) undertook a price increase of about 1% in January 2016 while

VECV increased prices by 1.2% in November 2015.

EML has received a board approval for commencing its third manufacturing

plant for RE. RE is targeting to have a total capacity of 9 lakh units by CY2018, given the ramp up at thesecond plant and commencement of the third unit.

EML has given productionguidance of 620,000 units for CY2016 and 780,000 units for CY2017.

Given the huge capacity increase of RE, the waiting period for bikes hasreduced from 4-6 months earlier to 3-4 months currently.

EML recently introduced an all new 411cc adventure bike “Himalyan”. It would be positionedas amid adventure tourer bike. This is an altogether newsegment as the current rugged off-roader bikes are in the higher cc segment.

The bookings forHimalyan would commence in mid-March 2016.

To broaden the product portfolio, EML would introduce another new bike in CY2017.

EML increased the dealership strength from 400 dealers in CY2014 to 500

dealers in CY2015 for RE. RE plans to have more than 550 dealers byCY2016.

EML is targeting export markets as a new growth driver for Royal Enfield. It is

eyeing potential in South East Asia and Latin American markets which have a

huge commuter bike base to boost exports.

VECV lost some market share in the MHCV space due to high discounting in

the industry. VECV market share slipped marginally from 11.7% in CY2014 to

10.6% in CY2015.

In 4QFY2016, VECV shippedabout 4,728 units as against 2,600 units in the corresponding quarter lastyear.