The CEO talks about it a little bit in the Q2 concall.

http://edelweissfin.com/Portals/0/Documents/Financial_Information/EdelweissFinancial-Earnings-Nov11-2016.pdf

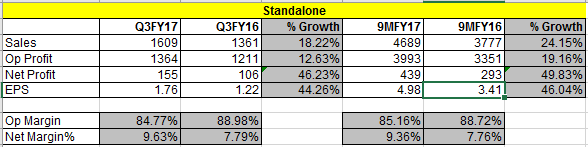

Q3 FY 17 Results

Key Highlights

- Consolidated PAT growth of 47%

- Ex-Insurance PAT growth of 40%

- Consolidated RoE: 15.4%

- Ex-Insurance RoE: 20.9%

- Ex-Insurance PAT CAGR of 37% over last 5 years

- Retail Book grew at 33%; Wholesale Book grew at 22%

- 9MFY17 NIM is 7.0%

- Awarded “SME Banking & NBFC Excellence Awards-2016”, (Chamber of Indian Micro Small and Medium Enterprises)

- On-Balance Sheet: INR~37,200 Cr; Total assets managed: INR ~139,700 Cr

- Comfortable capital adequacy ratio at 17.85%

- Positive asset-liability matching across durations

- Long Term Borrowings has grown from 5% in Mar’11 to 43% in Dec’16

- Raised ~INR 500 Cr from International Markets, through “Masala” Bonds

9 Likes

Please remove if it inappropriate post.

Hi,

Promoter Pledging should not be seen as a

Concern here due to exceptional management execution and quality.

“When stock market rises, some of their promoters have deleveraged by either paying off the loans or selling some of their stakes. Also, as the value of collaterals rose, they were also partially revoked".

Biocon is an example where promoter pledging has reduced from 66℅ to under 0.01℅ due to strong earning and stock price rise.

Stay Invested as you will see more upside due to growth pick up in Insurance and asset management space which they recently acquired from JPMorgan. Retail and wholesale book is strong too. Well diversified business with management focus to dilute risk.

Disc: Invested this week for next 3 years atleast.

3 Likes

thanks for sharing it!! a few things are surprising for me. Their wealth management piece hardly contributes to PAT despite being at decent size. One can look at it as lack of efficiency or opportunity for future. Few things stand out after Q3:

- Retail lending will get push in place of wholesale in the coming months/years.

- Wealth management could start contributing meaningfully.

the problem I see is that complexity of biz is unlikely to go down. Hopefully they would do a demerger at some point of time. Looks like a decent 2-3 yr opportunity.

Disc: Have taken initial exposure after waiting for long.

Wealth management business should not be seen as standalone revenue generator. The business model as i understand is revenue generation through cross selling to wealth clients, LAP, LAS, Advisory, AMC, etc. If we see FY 16 B/s the advisory fees is almost double than pure broking fees. Complexity is rather in web of subsidiaries than business, It was in capex mode till a year back and hope all guns fire. Decent quasi banking opportunity for next few years. Formation of Bad bank is risk to its one of the key business, ARC.

disc invested

True, on further reading I found that their yield from WM is 0.8-0.9% which is slightly lower than MOSL’s 1%. This is also a function of MOSL’s higher exposure to equity related biz. I think ARC could be very good thing for their own lending biz. They just have to offload it to own arm or handle it inhouse as they would become experts in this field few years down the line. Bad bank can not take full burden of all NPAs floating in the system. I am not worried about the idea which is a political minefield too.

Is Edelweiss not too diversified? Was reading their Feb Investor presentation and found that they are into Agri ware- house business as well. Bit surprising that a financial company would want to find opportunity outside its domain.

The insurance business is showing growth but does not adds anything to the profit. In fact a loss making entity in the group. I heard the management once commenting that Insurance business will take few years to break even.

Can anyone give their views on above please. Appreciated.

1 Like

Is it not too diversified?: I suggest to go through their AR of last few years. This is a very concious approach taken by Edelweiss to be in multi line of financial business and not in monoline. This is to counter cyclic nature of various business verticals of finance industry. Also unfortunately, in finance when growth is scarce, it is scored with quality deterioration of the business. Multiline helps to overcome this trap as well by firing few cylinders all the time based on positive business cycle and not taking undue quality risk on remaining for the sake of growth.

Agri Ware-house business. Unrelated business?: This is part of their Agri credit business. If they depend on other ware houses’ receipts for collateral, it is a bit of risk due to frauds. Such frauds are rampant from Americal Express Bank Case time till MCX time. hence it is a prudent decision to curtail risk from unknown to known.

Insurance Business.Not Profit making: That is the very nature of this vertical anywhere in the world. But that is where value lies after few initial years if risk is managed in the prudent way. Buffett made most use of FLOAT (premium money) to make further money. however, the beauty lies in assessing the insurance risk and doing no stupidity. hopefully they seem to have clear understanding of this aspect and keep communicating of same publicly as well.

Discl: Invested and hence likely to be biased…

6 Likes

Thanks for your comments @us121. I did check the AR and found the reasons for the diversification. Running too many financial products, to my opinion, dilutes the brand to some extent. Though I get the rationale.

I now get the idea of setting up the Agri wares.

Disc: Very small investment.

yes, diversification is by design that’s why it has failed to catch fancy so far despite the fact that everyone loves buying banks which are highly diversified lenders. There are individual admirers of MFIs and HFCs but not so for diversified NBFCs. Agri services is very good biz that gives headstart in rural lending where the market headed in the medium term.

Also, it is only other player along with MOSL to play transition to financial assets. Wealth Mgmt and MFs etc will bring non-linear earnings. I regret missing MOSL at lower levels.

Disc: Invested

Edelweiss Financial Services, a diversified financial services conglomerate, is in the process of selling its entire commodities business as it intends to make a fresh bid at getting a banking licence.

According to sources close to the development, after the NSEL scam, regulatory authorities were not comfortable with bidders for bank licences having sizeable exposures to commodities.

The sources said that Edelweiss Commodities had shut down its Singapore office and talks were on with several parties who would be interested in acquiring the business.

Last November, the Group had sold its agricultural commodities trading business, comprising both domestic and international operations, to Inditrade Business Consultants.

The business that Edelweiss is now looking to sell has a gold refinery and 265 warehouses. An Australian company has evinced interest in acquiring its gold refinery in Ahmedabad and the deal could be announced in March.

Edelweiss Commodities began operations in 2008 and set up offices in Dubai, Singapore, Africa and Canada. In FY16, the commodities business made a profit of Rs 65 crore.

In response to a questionnaire, a spokesperson for Edelweiss said on email: “As per Edelweiss’s philosophy and long held business strategy, we continuously reallocate resources including capital and people to better serve our customer needs and also where we see business opportunities. We are currently seeing very large scalable opportunities in credit, especially retail credit, as well as asset management and wealth management businesses and will continue to allocate resources towards these for maximum growth.”

Interestingly, when the Group entered the commodity business in 2008 it had said it wanted a play in bullion and agricultural commodities. Edelweiss Commodities set up a gold refinery in Ahmedabad and invested Rs 90 crore. The company also built significant warehousing capacity across India for agricultural commodities. The agricultural commodities business was set up to meet the warehousing and finance needs of producers and sellers. The company was also among the top importers of pulses in India.

The financial services conglomerate is now focusing on growing its retail and wholesale credit book. At the end of

nine months of FY17, Edelweiss Finance’s total credit book was at Rs 24,972 crore, of which the retail book is Rs 7,823 crore. The group is also present in wealth management services and asset management and has a asset reconstruction company that manages stressed assets.

3 Likes

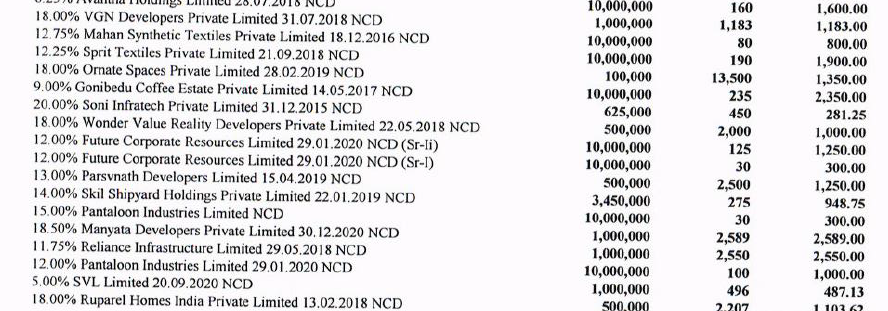

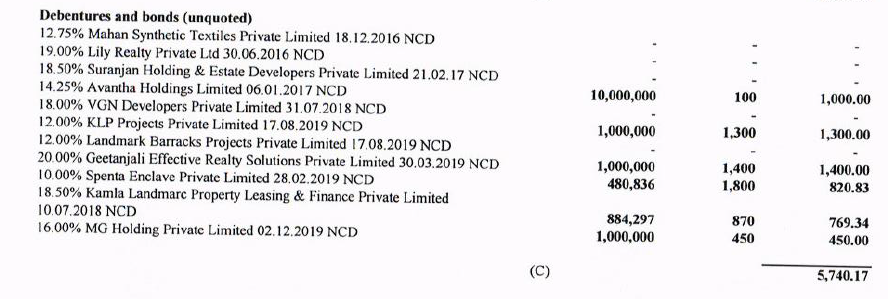

There is one question which I have and that has been a sticking point as far as Edelweiss is concerned and that is their assets in the subsidiary. Copy Pasting from the subsidiary ECL Finance Limited:

This is nearly 2400 cr + 570 cr is assets (more than 50% of Edelweiss’s net worth). To me most of these assets are in some of the most stressed sectors and the revival of such sectors is anybody’s guess. Some of the questions that I have to folks who are invested

a) What are your views on the quality and volume of these assets?

b) One of the reasons for having these assets is Edelweiss’s ARC business. Do you think that having both Asset and Liability within the same company but with different suubsidiaries is a sensible thing to do?

c) A decent portion of loan is between 15% to 20% interest rate. What do you think about the viability of a stressed asset generating return in excess of this?

2 Likes

What makes you assume that any mere mortal can gauge credit-worthiness of these loans without looking at balance sheet/understanding its business. Plus, it seems you assume these loans as unsecured by any asset, which most likely wont be true, most of these loans would be backed by assets.

Coming to these loans being 50% of book value, which I thing is quite normal, as the loan book itself is 25K cr odd (5x odd leverage). So these might be there SME loan book which would be approx 10% odd of the total loan book.

agreed Most of these are part of RE or promoter funding exposure in the form of debentures. These type of deals are quite normal and is being regularly done by IIFLs , Kotaks, Edewleiss of the world. Loans cant be sold and exit of exposure becomes difficult.

These debentures have active market in HNI and the structuring is usually quite secured with asset backup of 2 to 5 times depending on the underlying security and the structuring. Its part of their exposure. Its risky though but the essence of these deals is the structuring of the deal. Structuring of NCD is easier than loan and If i understand correctly legal option is also better than loan during recourse. (lawyer friends r welcome for their inputs).

1 Like

Well if I am in the business of investing in financials I would like to gauge the credit-worthiness of these assets, I would like to have a view (subjective) of the quality of assets. If these were govt. securities I would have been happiest, if these were of some reputed companies like Tatas I would have been fine. As I said most of these assets are from stressed sector it would make sense to understand them or to atleast question the management about them, the least I would do is look for their credit ratings.

I never assumed that these assets are not backed by assets and as I mentioned they are probably coming from the ARC business.

It is certainly not a discussion on whether they can lend to these companies or not but more on the quality and risk that these assets can result in. If someone sees no issues with this kind of book there is nothin g to debate.

Would love to understand more from you as my knowledge of such deals is limited.

As far as asset backup is considered my experience is that loans backed by assets and not by cash flows are a hard sell. I have heard a lot of financial institutions actually calling out stress in their LAP portfolios. Further there is also some anecdotal evidence of aggressive lending by Edelweiss (Bhushan steel?), also one of their recent ARC deal (speculated in Newspapers) was with one of the worst projects in Hyderabad (I stay here).

Just to conclude I admit I do not understand the business well and would be happy to be wrong.

8 Likes

Looks like Rashesh Shah is truly getting ready to apply for bank license

As I said it is not just the kind but also volum. At 360 cr the exposure does not look worrying for bank of size of Kotak.

Hi Anant it was just a snapshot, kotak does it in many other Balance sheets. Kotak prime is primarily a car financer, having said that it is riskier and structuring (inclusive of promoter guarantee, personal assets as collateral etc are usually part of these deals). These are further sold to fancy family offices and Ultra HNIs who have fancy to complex asset classes. As u rightly mentioned the cashflow vs collateral the crux here is underwriting the risk. So far they have managed well.