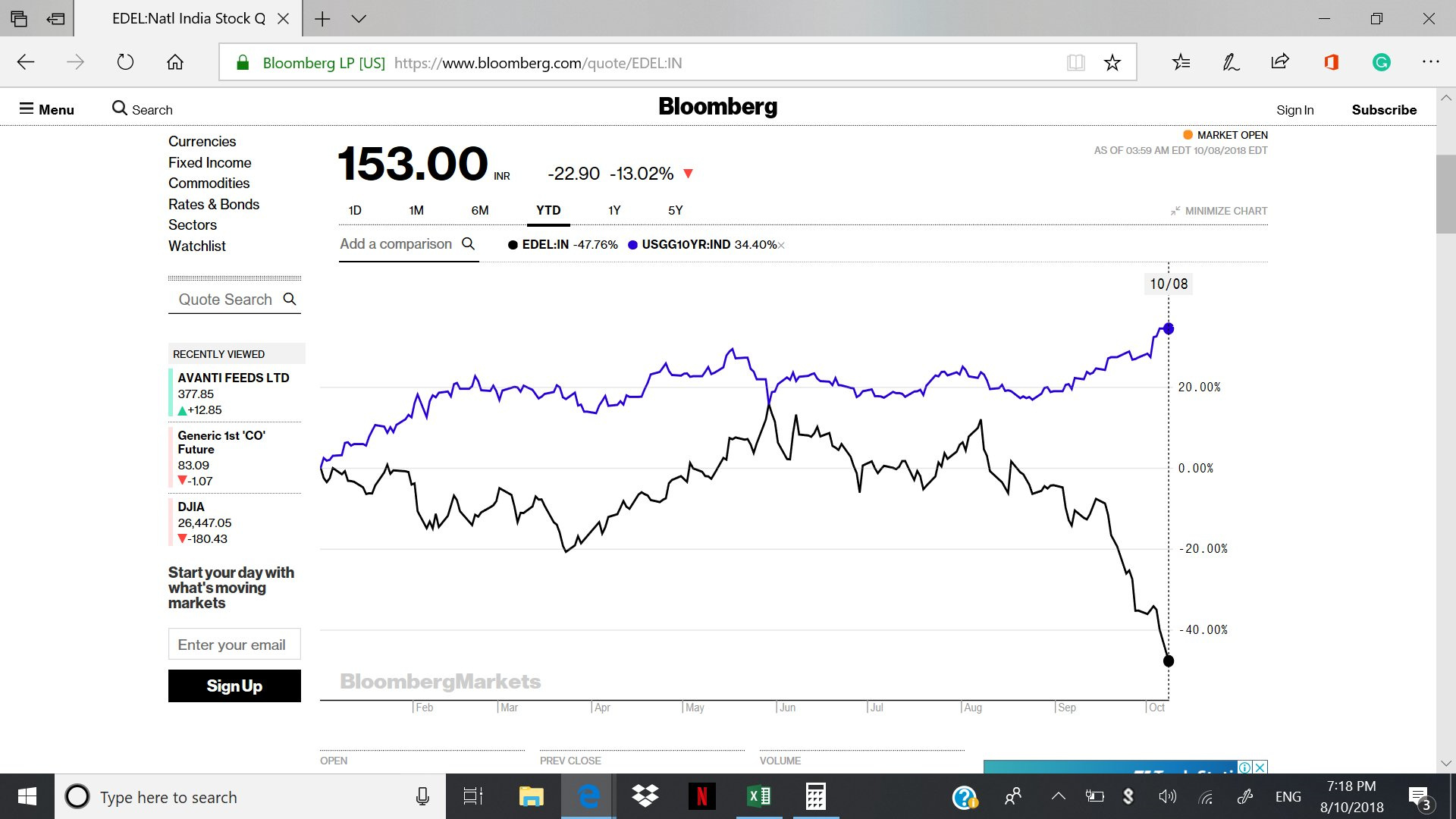

Edelweiss and US 10 yr yield. It converges on May 25th, 2018 when US 10-year yield drops below 2.8%, down from 3.13% earlier in the month. It’s clear that Edelweiss and NBFC going through de-rating in valuations as cost of funds rise in US. Definitely not IL&FS but yields in US.

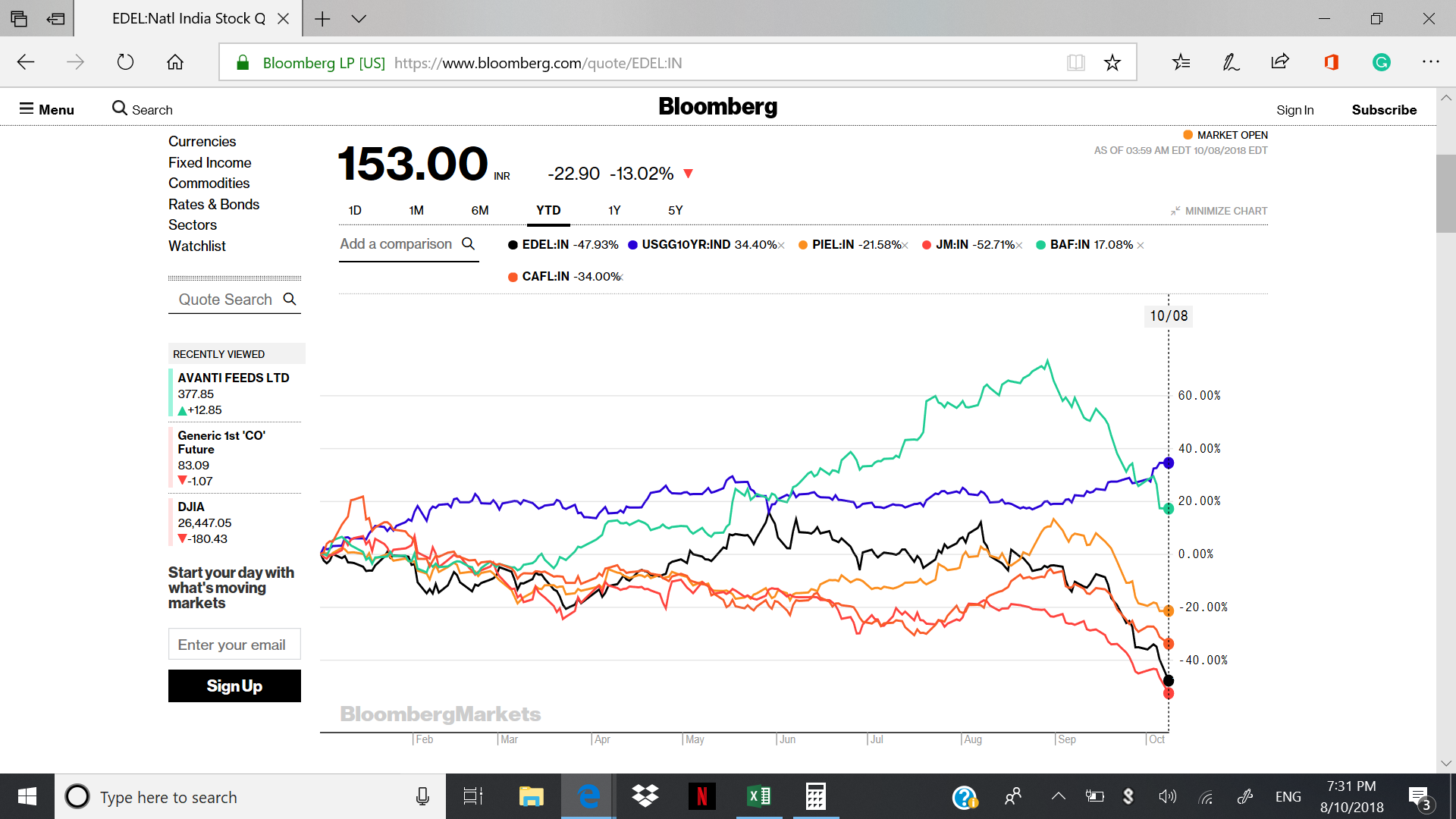

Clearly JM and Edelweiss showed more negative correlation with bond yields, less for Capital First and PEL bcoz of not being pure play NBFC has seen lesser correlation to yields rising. Bajaj finance is an outliner here rising 15% YTD.

It suggests that more risk lies on funding side on business with rising yields on edel, jm and capf and market is derating the stock to reflect future de-growth and adjusting P/BV to around 1.5-2 P/BV. Given IL&FS episode, you would see more scrutiny by RBI going forward which would increase regulatory costs.

Not sure you can confirm a correlation with 10 year yield. ALM at Edelweiss and peers is more diverse, and funding varies as per maturity bucket. Yields will also vary across tenor. Not sure what % 10 yr G-Secs are of Edelweiss funding.

Also regulatory costs are going to be set up of ALM reporting systems. RBI hasn’t clarified how/why of it but it may be similar to Net Stable Funding Ratio under BASEL III, which banks have implemented. It is a one time cost after which the ratio is reported on ongoing basis. Besides, regulations can be a positive for NBFCs as they de-risk the environment and protect the downside, as seen in NBFC-MFIs. The stronger, organized players will thrive in regulated environment.

I must admit that this is the first time I panicked after may be 2008 but no action so far. The way it is falling without any major company specific event is very unnerving. It doesn’t help when it is the largest holding. One has to give credit to Rashesh shah that he warned himself, in his last interview to CNBCTV18, that equity of NBFCs are adjusting to the new reality of tight liquidity and lower growth prospects. I still think he will outperform the industry.

AFS and HTM Classifications are based on Ind AS. Ind AS is applicable for NBFCs from FY 19 onwards.

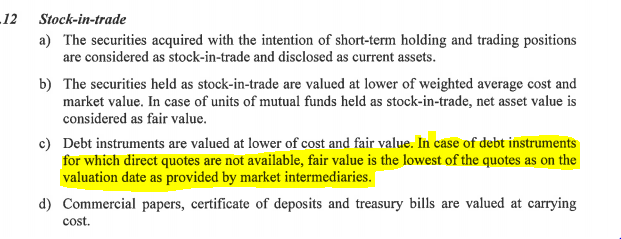

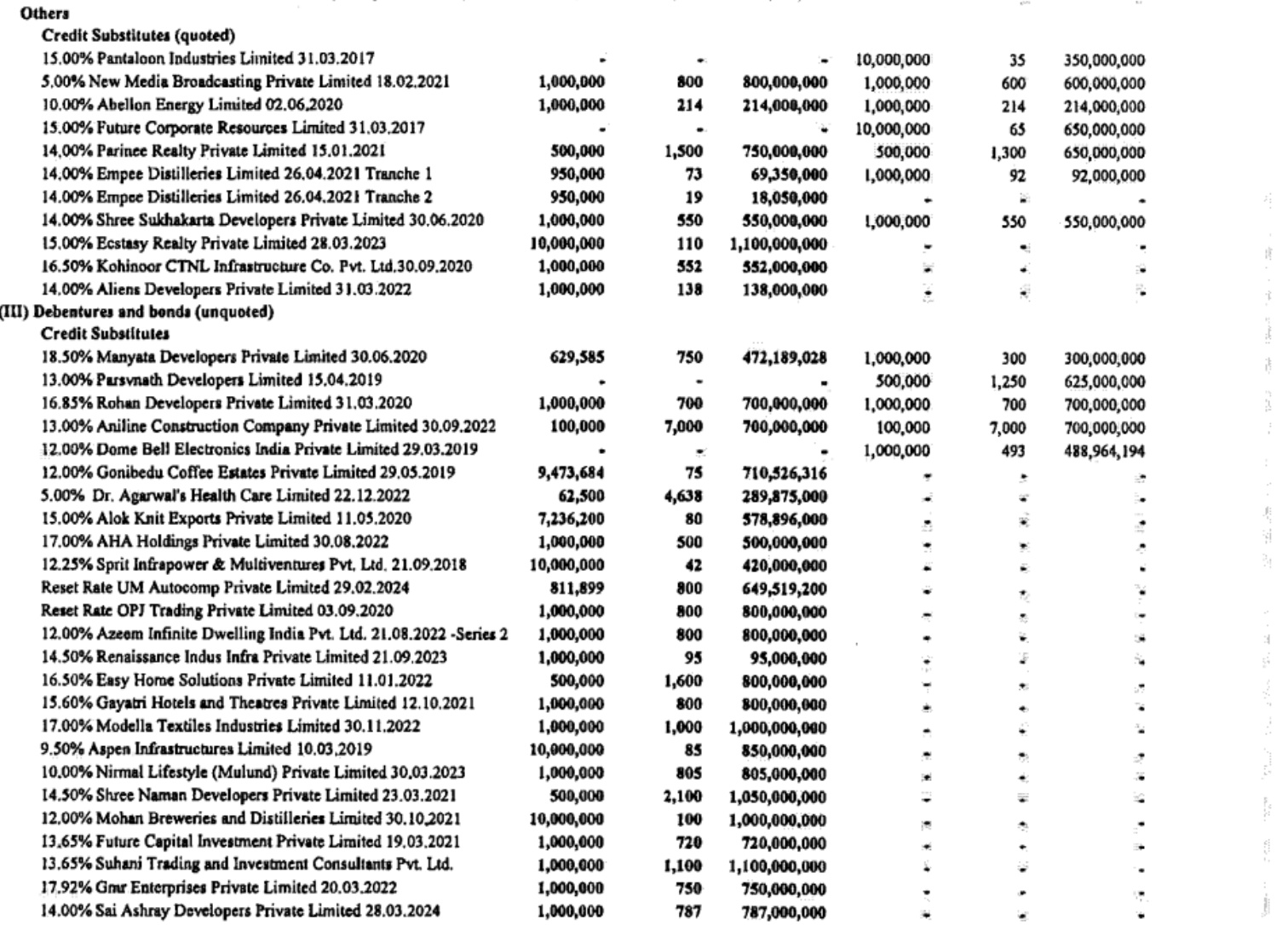

All NBFCs have used good old IGAAP for accounting, presentation and disclosure in Financial Statements of FY 18. IGAAP requires Investments (which are not the primary business of the entity) to be disclosed under Current and Non Current Investments. However, when an entity’s business itself is to invest in bonds and other securities - it must be shown under Stock in trade.

Now accounting policy basically states that when direct quotes are not available, there is no MTM required!

Im sure there would be a significant mark down in both Stock in trade and ‘Investments’ once the Company starts using IND AS.

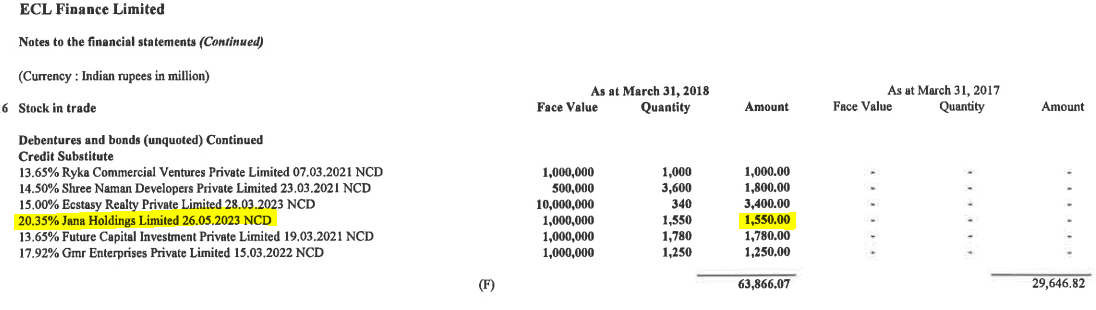

The ‘Stock in Trade’ schedule of ECL Finance offers a significant opportunity to analyze the credit quality of the RE loan book since names of the borrowers are disclosed.

Most of the borrowers are Private Limited Companies and their Financial Statements can be downloaded from MCA website by paying Rs. 100 (Wise to download after 31.10.2018 since thats the due date to upload FY 2018 financials)

Details of security cover can be accessed free of cost of checking the details and value of charges registered again on MCA website or independent websites like Zaubacorp.

Of the very few publicly available Financial Statements, I am curious to know whether the investment of Rs 155 crores in Jana Holdings is still a standard asset or classified as an NPA.

Glaring errors on page 11 of the investor day presentation, not a great document otherwise either, with a lot of macro jumbo-mumbo. I expected better.

Disc: Tracking

This is also in the same category as ECL Finance and looks like was being financed by short term liabilities. One another interesting snippet is company’s investment in ICICI securities IPO at 520:

Thanks for sharing. Try looking into Ecap Equities Limited and Edelweiss Commodities services limited.

Ecap equities has pledged assets to NBFCs. I don’t understand why a NBFC would want to raise money from other NBFCs.

I went through debenture documents of Ecap equities but don’t understand why they cant raise money from banks like Axis Bank who have a strong capital market book.

The valuation norms for stock in trade of ECL finance is lower of weighted average cost and market price. Suffice to say even though some of those debentures are listed. There is no trading happening whatsoever.

This gives away lot of hints what’s coming… one word another painful adjustment ahead. Key takeaways

Liquidity tightening

Stricter ALM

Possible changes in leverage ratios.

This will make private banks particularly competitive against NBFCs which can’t raise public deposits. Also, very clear that it will impact growth for the next 6 months when they could reprice their assets.

Banks don’t lend directly to risky sectors but they lend to NBFCs that lend to risky sectors. I find this curious. Did the overall risk in the system reduce because the risk is now distributed along the credit chain? Will a NBFC blowup protect the banks in any way other than delay the contagion? If the private banks are leveraged 10x historically and are still at the same leverage but lend to NBFCs that leverage themselves 7x, hasn’t the overall leverage in the system gone up substantially?

The declining RoE of private banks due to declining RoA and increasing GNPA shows that things aren’t looking good. What if NBFC blowup happens and private banks’ RoA turns negative like the PSU Banks? I think the negative news flow in Axis, Icici and now Yes bank is a pointer in that direction. What is happening now is being called a liquidity crunch but that is not the cause but an effect of excess leverage in the system. The capability of the economy to service its debt is coming down and the only solution is deleveraging. Exactly how it’s brought about will determine if there will be blowups or if the deleveraging will be beautiful.

The article posted above containing Mr Rashesh Shahs interview has already explained this part.

Suppose a Bank has Rs 100 equity and leverages 9x against this. It will have a Loan book of Rs 1000 (Rs 900 + Rs 100). Suppose the Banks lends this entire Rs 1000 to one NBFC which has a 7x leverage. This means that against his borrowing the NBFC must keep aside

another Rs 142 of its own equity (1000/7). Therefore, the total equity cushion against this Rs 1142 of Asset of NBFC is Rs 242 (100+142).

You can do the math, the overall leverage (Debt to Equity) in the system infact Reduces.

The risk which increases is dependency on each other, which is all together a separate discussion.

To assess overall leverage in the economy, there are other indicators such as Credit Growth vs GDP growth, Capital Adequacy ratios required by Regulators, Leverage of Central Bank etc.

Exactly ,some of the banks were lending heavily to nbfcs and were also purchasing asset pools from them ,PSU banks too among them. This may not be double financing, but the overall risk seems to increase .In the light of IL&FS fiasco already they have started reviewing these facilities and market rates for these NBFC s are definitely going to increase.

And the Real Estate could be the first one in the cleanup list. They have been delaying the deleveraging for so many years. The economy could slow down a bit because of this credit crunch as it will cause the people and businesses to delay their spending.

Good discussion. Let’s use the same example. The total debt in the system is 900 + 1000 = 1900 and Equity is 100 + 142 which means D/E is 1900/242 = 7.85 (that’s assuming the equity of the NBFC itself wasn’t financed by leveraged debt, which I presume can happen in a QIP) so the 9x leverage of banks and 7x leverage of NBFC’s means that the total leverage in the system is 7.85, best case. Now look at this way - If the bank wasn’t ready to lend the 1000 to a risky sector, now the NBFC is willing to lend 1142 to the same risky sector and somehow the bank is absolutely OK with this because the responsibility for end use/collection is not with it. This is what I meant by rising risk with the reduction in responsibility.

It is not that Bank does not lend because it is a risky sector. No bank has capabilities to lend to all kind of businesses/people. Skills and reach required to do loan against gold are different from housing loan or consumer durable loan or micro finance etc. That is where these NBFC come into picture where they have specific domain expertise. This is not different from any other Industry… We have Maruti, Bajaj Auto, Hero and all big names but they do not make all auto components. They focus on the core design, marketing and assembly and that is why so many auto ancillary came up and thrived. Both exist together and are complement to each other. I believe there is no breakage in basic model of Bands and NBFCs… only thing that will happen is some non-efficient player may die and efficient ones will recover and thrive back in few quarters though they may not get the same valuations if sector goes thru PE de-rating.