I was wondering how much can Edelweiss make from the Essar deal. The above explanation is good but it doesnt talk about the extension of timelines in debt resolution. So below is the list of loans of Essar that Edelweiss bought. As per Essar steel website, the exposure of Edelweiss ARC is about 7400cr. I have compiled this from few news articles and I see that some of the numbers vary depending on the source.

550cr in march 2015 from hdfc bank.

70cr in Dec 2015 from federal bank.

1600cr in jun 2016 from ICICI Bank. Discount was about 50%.

1000cr in sep 2016 at 55%discount from axis.

1600cr in July Aug 2017 from Indian overseas bank at 50%.

1000cr in aug18 at 30%discount from hdfc Ltd.

These components must be getting booked regularly all along.

Now what additional amounts can Edel get would be from the below part. And it does appear that Essar steel resolution can go to about Rs 75-80. So would total IRR be around 30%? Sounds unrealistic

Here is my calculation. For calculation of lumpy benefit, I have assumed 3 years for HDFC, Federal bank, 2 years for ICICI, Axis and 1 year for IOB amounts.

| Loan bought at (cr) | Seller | Discount | When? | Edel investment | Additional IRR assumption | Lumpy benefit |

|---|---|---|---|---|---|---|

| 330 | HDFC Bank 550cr | 40% | Mar-15 | 49.5 | 12 | 70 |

| 42 | Federal Bank, 70cr | 40% | Dec-15 | 6.3 | 12 | 9 |

| 800 | ICICI, 1600cr | 50% | Jun-16 | 120 | 8 | 140 |

| 550 | Axis, 1000 | 55% | Sep-16 | 82.5 | 6 | 93 |

| 800 | IOB, 1600cr | 50% | Aug-17 | 120 | 8 | 130 |

| 700 | HDFC Ltd, 1000cr | 70% | Aug-18 | 105 | Negligible | |

| Total | 441 |

The total lumpy benefit is coming to 441cr, which looks a bit too much. Maybe this is where the timeline of resolution would effect the additional IRR, eg HDFC Bank exposure bought in 2015 would not earn additional 12% IRR ?

Can anyone help? @dd1474 @desaidhwanil

I think they do have clause of sharing upside with banks from which the loan was bought. I am not sure how do they book profit after concluding the deal. I think it happens when they get the fund reimbursed helping them redeem security receipts. So whole P&L booking could be spaced out.

You need to look at Q1 annualised RoE in ARC div. which touched whopping 25% and there is every reason to believe that in some of the upcoming quarters it could even touch 30% in this div. so IMO 30% is not unrealistic. This is also because some of these asset resolutions are getting bunched together. I was going through credit report of their ARC div and what I found very heartening that 57% of all loans/assets they have bought or managed (~43k cr) are resolved so they would become productive sooner than later. They have gone of another round of 10-15k cr fund addition in ARC which shows confidence in their biz model.

Yes…I remember reading somehwere that the ARC gets about 20% extra carry on the additional recovery that happens. This 20% generates the additional IRR and is booked at the time of final settlement. This is the lumpy part that I am trying to estimate for Essar exposure. I maybe completely off but if this calculation happens to be approximately correct, then it can be a large kicker, given that FY18 PAT was 890cr.

By the way…Edel holds 60% in the ARC so the 440cr will translate to 264cr

Broadly, I agree that Edel ARC is in a sweet spot. Many accounts are finally getting resolved so there will be lot of positive surprises in numbers. Also, the recent deals are moving to more cash components and therefore the large players will be able to grab these. The competition has been increasing with foray of many international players. But the market size is enormous.

yeah, they 3 sources of funds in ARC. 1) Equity and debt from owners Edel, CDPQ and HNIs 2) Managed funds from other investors typically AIF or wealth management looking for high yield fixed rate instruments 3) They also raise own debt.

Equity holders get 2% fund management charge + performance fee after hurdle rate. They also raise debt to deploy into companies at the cusp of revival at very high ROA. Equity size of ARC is 6-7k cr so even 3% RoA on 43kcr will make 20% RoE which looks perfectly possible in the medium term. It was widely reported in media that in one deal i.e. Binani cement they were supposed to make 500cr worth of profits

Sorry but I am not able to understand the methodology that you have used to arrive at additional IRR calculation. Can you please explain it a bit more? Also, I feel the template is too simplistic and we are working with limited information and lot of assumptions. So unless we are privy to deal details in each case, it is very difficult to project a number. However, I think 30% IRR is quite possible on case to case basis where evertthing work in their favour (steel cycle). Also, as we know, the key thing in getting deisred IRR is the timeline for resolution and as the resolution is delayed, IRR gets diluted. Also, like we do, we have to look at the IRRs on portfolio basis and I think they should be generating more than 20%IRR on portfolio, which is very respectable.

Hi Dhwanil,

Thanks for the comments. Here are the steps that I followed for the calculation

-

Collect approx numbers from news articles on the loan bought and discounts from different banks. I assumed 40% in cases where discount info was not available. Eg HDFC bank loan of 550cr was bought at about 40% discount so that comes to 40%*550= 330cr.

-

Now Edelweiss contribution in this would have been 15%, ie 15% * 330=49.5cr.

-

Then I assumed an IRR based on the info as per concall. For eg, In case of HDFC bank loan which was bought at 40% discount, and the recovery is 80%, then IRR can be about 30%. So I took additional IRR to be 12%.

-

This 12% IRR in 3 years would give 49.5cr* (1.12)^3= 70cr

Maybe I made a mistake in last step. I should calculate 30% IRR on 49.5cr and deduct the regular interest that would have been booked by now. Possibly it should be = 49.5* (1.3)^3 - regular fee and interest income in 3 years

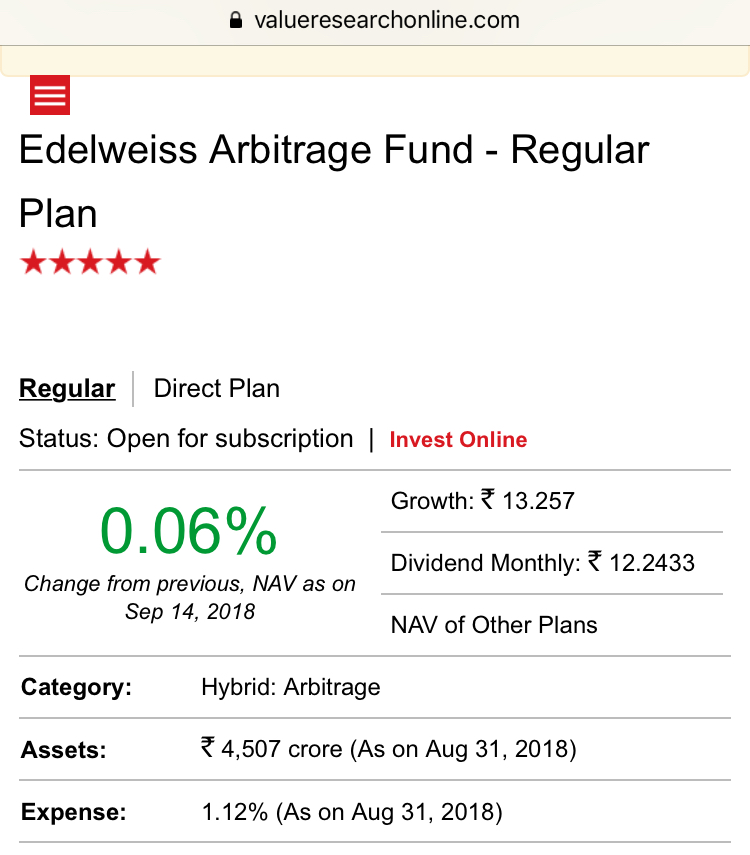

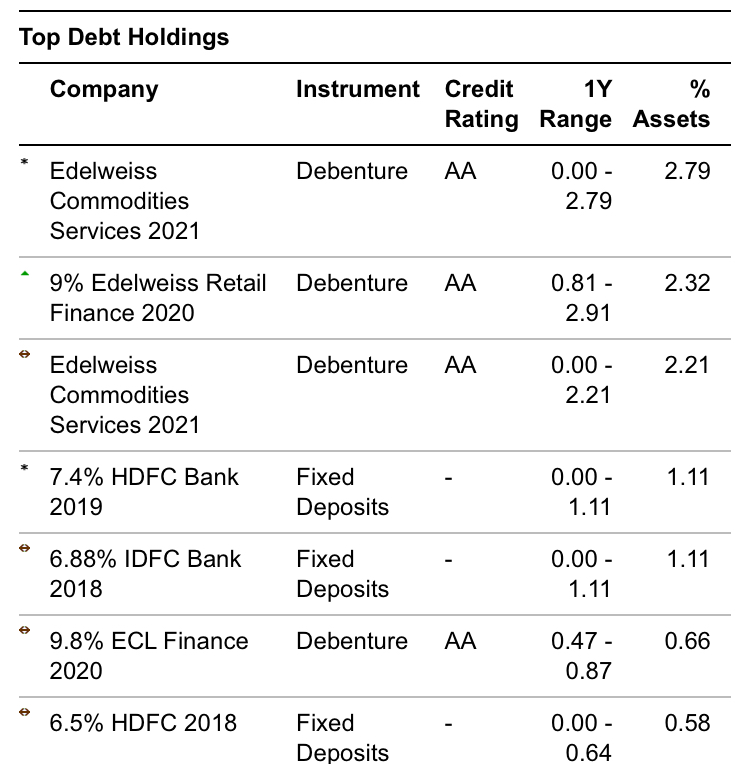

In Asset management - most of Edelweiss funds are performing poorly in terms of AUM, Performance, Ratings.

The top performing Fund - Edelweiss Arbitrage Fund has suspiciously large exposure to Edelweiss Group Companies

Bonds.

Also in Wealth management - majority revenue comes from broking/ distribution - which is likely to face serious threat from new technology, discount brokerages, new competitors like PayTM

I’m finding it hard to believe that Edelweiss will perform above the industry average in these two businesses

Sorry, i didn’t understand the issue. You have chosen a fund which is 5 star with 4.5k cr of AUM which can’t be called small. Regarding holding in Edel debt securities, it is completely immaterial for Edel whoever holds outstanding debt once it has been issued. Allocation is also typically small. You need to keep in mind that Edel acquired JPM funds and they were under performing. They have very few schemes which are Edel original. I don’t track MF universe closely but funds have started doing relatively better after Edel acquired them. BTW, Edel arbitrage fund is 4th in terms of returns over 3 year.

I just made a fund house search on edelweiss on value research and can see few funds from edelweiss in 4 star ( large cap And a mid cap ) and 5 star ranking ( arbitrage fund,govt security etc)

They just started scaling up this business so we can expect ( and hope ) that they will only improve from here on.

As I write they aggressively scaling up their branch network ( I know as we are in discussion with them to supply some equipments required for branch rollout ) .

I don’t know branches will be of brokerage/insurance or other business of edelweiss though.

So let’s wait and see how they scale up their business.

Rashesh Shah has been alluding to this for some time now…the trend seems to be only strengthening with every qtr.

India is primed to double its size to a $5-trillion economy from $2.5 trillion at present over the next seven to eight years. Edelweiss Financial Services Ltd., with its fingers in all aspects of the country’s financial market, is the stock to bet on, said Stallion Assets’ Founder Amit Jeswani.

With the latest mayhem on market , this needs to be re validated.

Do you think there is any issues with edelweiss too ?

BTW …He also recommended Diwan to his customers …only fyi.

So my mantra is never take any one on face value and do your own duedeligence before getting in to or out of anything.

After all every individual is human and hence can get influenced by bias,greed ,fear and other emotions so .

Edelweiss will face headwinds too –

Rising bond rates

Hit on MF distribution revenue from wealth management side

Souring of sentiment regarding MF inflows

Further weakness in Capital market revenues

…so on

Most of these are in common with other NBFCs but thankfully none of these are going to be permanent issues.

I did’t say buy or sell because of the short term issues. Be careful for the next few months is my strategy. Amidst all this frenzy in the domestic market we have forgotten that US 10Y yield has crossed 3% again which is not a great sign for domestic bond yields. Could this bring down the growth machine to 25% from 35% that is perfectly possible.

Disc: Invested

Two days back company has conducted large event for their employees all across a very first one till day …where chairman conveyed some key messages it was a full day event and all employees were expected to attend over video conference / in person etc.

I will be meeting few of them on Monday and shall update what Rashesh shah and other top executive had conveyed to employees …after all they are adding 2000 odd employees this year to their current base of 10000 employee base of last year .

It’s imp and critical to keep communicating with all to keep them motivated and to give directions around area to focus.

I am happy to see such initiative happening at company in which I have 2nd highest holding with superb level of management integrity ( no negatives yet ) .

Cheers

The following post is mainly to understand the impact of the events that have happened in the last week and the way it impact specifically related to the one of their subsidiary ECL finance limited and the short term (Stock in trade) of debentures that ECL carries.

There were two interesting developments that happened in the last few days:

- ILFS being downgraded from AA+ to BB on September 8 and then to D on September 17

- DSP selling DHFL debt at around 200 bps lower due to lack of liquidity or buying interest in DHFL.

Now why does these two event have anything to do with Edelweiss? Besides the generic issues like hardening interest rates which impact every financial Edelweiss carries a large amount of ‘Stock in trade’ of sub standard debt in its subsidiary ECL finance ltd.

-

How significant is ECL finance ltd?

Out of 890 crores PAT that Edelweiss had last year 462 crores came from ECL Finance. ECL Finance as per last year AR has a net worth of 2939 crores and Assets of 26755 cr. -

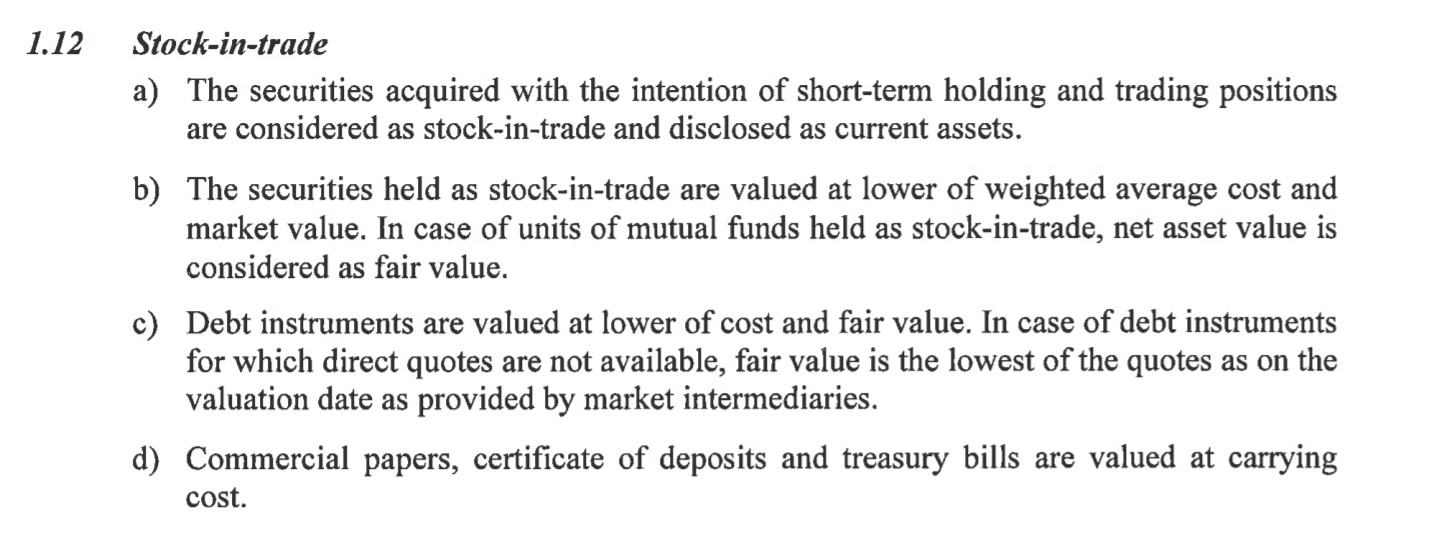

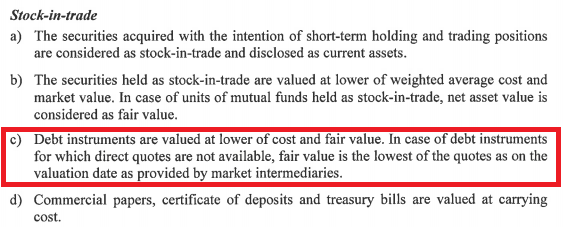

What is Stock in Trade?

Stock in trade as per ECL finance annual report is:

-

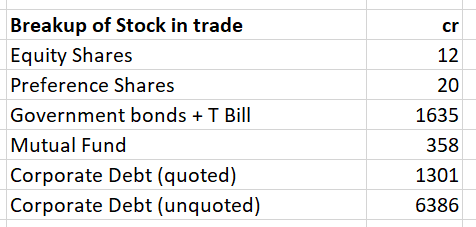

How significant is Stock in Trade?

Out of the total assets that ECL Finance has i.e. 26755 cr , Stock in Trade is 9713 cr or 36% nearly.

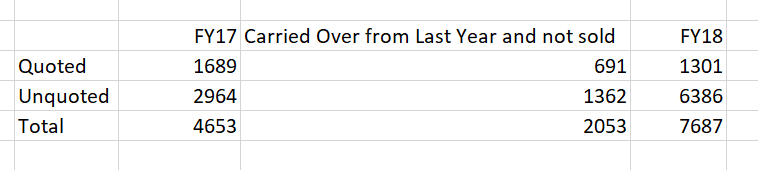

So Stock in Trade is significant and is short term . One look at Stock in Trade and it is clear that it is dominated by sub standard debt. A rough break up is:

So a total of 7687 cr of Stock in Trade is in Corporate debentures. A brief look at this Corporate debt gives an impression that it is really a high yield debt of low quality. There are ofcourse some good names here and there like Shriram/Piramal/Edelwiss group companies/Indiabulls/DHFL/Yes but they are far and few. A crude analysis gives out that around 10% to 12% of corporate debt is in somewhat well know. From a business standpoint too it makes sense to have this kind of debt because short term borrowing would be costly (to acquire this debt) and this kind of debt if one can sell could give a 5% to 10% kind of spread.

The other interesting thing to look at is how much of Stock in Trade was carried over from last year FY17 and was not sold in FY18 in the corporate side. Holding which are present in both FY17 & FY18 can give an idea about that. Roughly this is how the nos. look:

So out of 4653 cr of Stock in Trade ECL Finance could not sell roughly 2053 cr nearly 44% of the corporate debt.

ECL Finance gives the carrying value and market value for quoted debentures and since the market value is higher than the carrying value there is no impact on balance sheet. Incase of unquoted debentures we need to take it on good faith.

Looking at some of the corporate debt ECL Finance has it is easy to see that some of it has had ratings downgrade and most of quoted debt doesn’t trade actively.

If we look at most of the debt matures in CY19/CY20/CY21. So any assumption that Stocks in Trade debt if it is not traded will mature does not hold.

Finally a few questions to those who understand debt markets and accounting:

- How can one mark to market the corporate debt that ECL Finance has when it does not trade in the market? Also incase of rating downgrade which has happened in some cases like the ones below what is the right course of action?

2.The major way in which this ‘Stock In trade’ seems to be financed on the liability side is Short term borrowings + Loans from related parties + CBLO + Other current liabilities (maturing term loan + maturing NCD + book overdraft). Now incase of a liquidity squeeze how does this scenario play out since there are no buyers for this kind of corporate debt? Will this not create an ALM scenario?

3. For those invested in Edelweiss the general answer to the quality of debt has been that there are multiple covenants and the underlying assets should be sufficient to address the debt. The argument is based on faith in management and an underlying assumption that they are doing the right thing. Assuming the argument holds good implying Edelweiss can do fine in the long term but isn’t there an underlying dangerous assumption on the short term liquidity not falling apart.

Discl: No holding. ECL Finance’s corporate debt has always been a concern.

ECL Finance Annual Report FY18: Top Finance Company in Mumbai, India | Best in Investment & Advisory Services - Edelweiss Finance

Great post @Anant and thanks for sharing your findings! Will share my understanding on some of the items below:

Well, as it says below, “incase of debt instruments for which direct quotes are not available, fair value is the lowest of the quotes as on the valuation date as provided by market intermediaries”. If the lowest quote from intermediaries is below cost, they will write it down and run the difference through P&L since its “held for trading” and stock in trade is part of current assets.

I noticed your examples, ABT, Saha, Shree, and Parinee all are quoted corporate bonds. They would take their quotes from market on book closing date and then compare with previous value in the books. Would mark up or down the difference and enter the difference in the P&L (other income). To answer your question - rating downgrade would have pushed bond price down and they would have had to write them down (if quote is available or else go with intermediaries quote).

Just FYI - I noticed them marking down their holding in Nspira Management Services Pvt Lt bond. Below is the screenshot.

As you are aware of - exposure to such high yield bonds (if not Masala or Junk bonds) is not bad as long as they are paid appropriately for the risk involved in it. I hope they were purchased at significant discount to the par value and also hope that BMU (balancesheet management unit) did appropriate due diligence of underlying collateral and ability for the management to pay back the principal. Crucial thing to find out would be, if these corporates are paying coupon (if there is one) on time. I hope Indian debt debt market experts reading my comment would shares his/her insight with us on the corp bonds in question. ![]()

Excellent question. IMHO - no one except BMU would know how the ‘stock in trade’ is financed. Here an investor has to trust the management and its execution capability to ensure ALM is maintained all the time. Hence, as we know, conservative management is super critical in lending business.

Views/questions/comments invited. Thanks

Disc: invested and views may be biased.