was going through the Q1 con call transcript and found keen interest of Motilal Securities in knowing outlook for Capital market, home finance and wealth management biz. In all three segments they are competitors though

It has diverse biz which is difficult to value using a single metric. Consolidated ROE is not usable ratio since Insurance is at a fundamentally different operation with own accounting treatment. Do you use RoE to value insurance biz? Best is to do SOTP and arrive at correct valuation. I remove 2-3x of embedded value from the market cap to arrive at PE (~20x TTM)vs. ex-insurance RoE (20%+). On that basis it looks like less than fairly valued. Ex-insurance RoE has only one direction i.e. up since cost/income ratio in lending and savings products is coming down with scale and sweating of capital. It is generating extraordinary RoE in AMC/capital markets and even ARC which is part of lending. I was going through their wealth plus ulip product in the insurance vertical which has been a big hit.

These all are Bullish view points. What about CAR ? It seems , Edel need to go through another set of dilution within 12-15 months which will again tapper off ROE again. The valuation Gap which was is in 2016, that was met (Rose 3 times). If there is no improvement in ROA further , PB re rating is not possible.

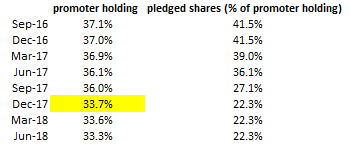

Go to the shareholding details of the Company available on the BSE site and open the shareholding details for the comparison periods (Sep & Dec). Check out the qty of total shares of the company and the shares held by the promoters for the two periods.

You will notice that while promoters shareholding (qty) is unchanged, the total outstanding shares for the company has increased, hence the % held by promoters has come down.

If you are curious why the total no of shares have increased, google will tell you that in 2 min (hint: QIP).

I have few contacts in the company a we are one of the IT supplier to them, they plan to hire around 2000 people this year across all business verticals ( that’s around 20% addition, current employee strength is 10000) , people have already started coming on board and we are under pressure to deliver the basic IT equipment etc. that’s needed by them.

looks like if all goes as per plans they can grow really fast from here on for next 3-4 years at least as some of the business that they are in are at inflection point. i.e. ARC etc.

Buy side of FIIs requests it for their decision making and ease of global comparison/benchmarking. The company might be raising another round of funding before 2020 so it helps to get valuation.

A good example of power of simplicity (explaining things simply) - thanks Mr. Rashesh Shah.

How the payoff works in an ARC model (under 85-15 structures)?

On an average when we buy a Rs.100 loan we buy it at let say Rs.40 that has been the average. A loan which is in the bank at Rs.100, the purchase price for ARC is Rs.40 and up till now a large part of the book has been under 85-15.

When we buy something at Rs.40 we put a Rs.6 of our capital into that and the other Rs.34 is bank’s capital or the bank’s security receipts in that. Now we have AUM of Rs.40 and our capital invested of Rs.6.

On that Rs.40 we get fee, on the Rs.6 we get some interest also because these are credit assets which are earning some interest or the other or an average on the Rs.6 that we invest, we end up getting between Rs.1-1.10 as annual return which is what we call the 16% to 17% current normal yield.

If you recover more than Rs.40 so if we buy it at Rs.40 and we recover exactly Rs.40, then on the Rs.6 we invested, we will get a 16-17% yield.

If that Rs.40 gets settled at say Rs.30 we make a loss on that then our yield falls down from 16%-%17 to 11-12%.

If that Rs.40 becomes Rs.20 then the yield falls down to almost equal to 0 which means we get back only the Rs.6 capital because on that fixed capital we will lose Rs.3 but we will get Rs.3. So, effectively we just broke even on that is on the downside.

On the upside, when we buy something at Rs.40 and we settle at Rs.50 we should get an incremental IRR of about 3% to 4% cost on that.

And if we buy it at Rs.40 and we settle at Rs.60, we should get another 3% to 4% points IRR.

So, if you buy it at Rs.40 and settle at Rs.40 you make about 16%-17%, if you buy at Rs.40 and settle at Rs.50, you get 21%, if you buy at it 40 and 60 cents to a dollar you end up getting 25% IRR so that is the broad way of estimating this.