If the idea is to compare businesses in terms of business quality, I think removing cash makes sense as that will give an accurate picture of business machinations. I did something similar to compare Dr Lal Path labs and Thyrocare. In terms of CoC on cash/investments in mf etc, I agree with @bheeshma that an indicative 15% should do. Going any more precise on that I think is futile due to the law of diminishing returns for practical purposes while it might make sense in an academic exercise if the evaluation depended on it.

2 Likes

The problem is, I already use 15% Kc for all my Valuations anyway (Regardless of excess cash or not), unless the market-implied Kc is higher.

I agree that this is just nitpicking, but I’m interested in the theory. While theory may not be very useful always, it helps in extreme cases like Apple (As Prof. Damodaran himself had discussed).

Thank you for the feedback again.

2 Likes

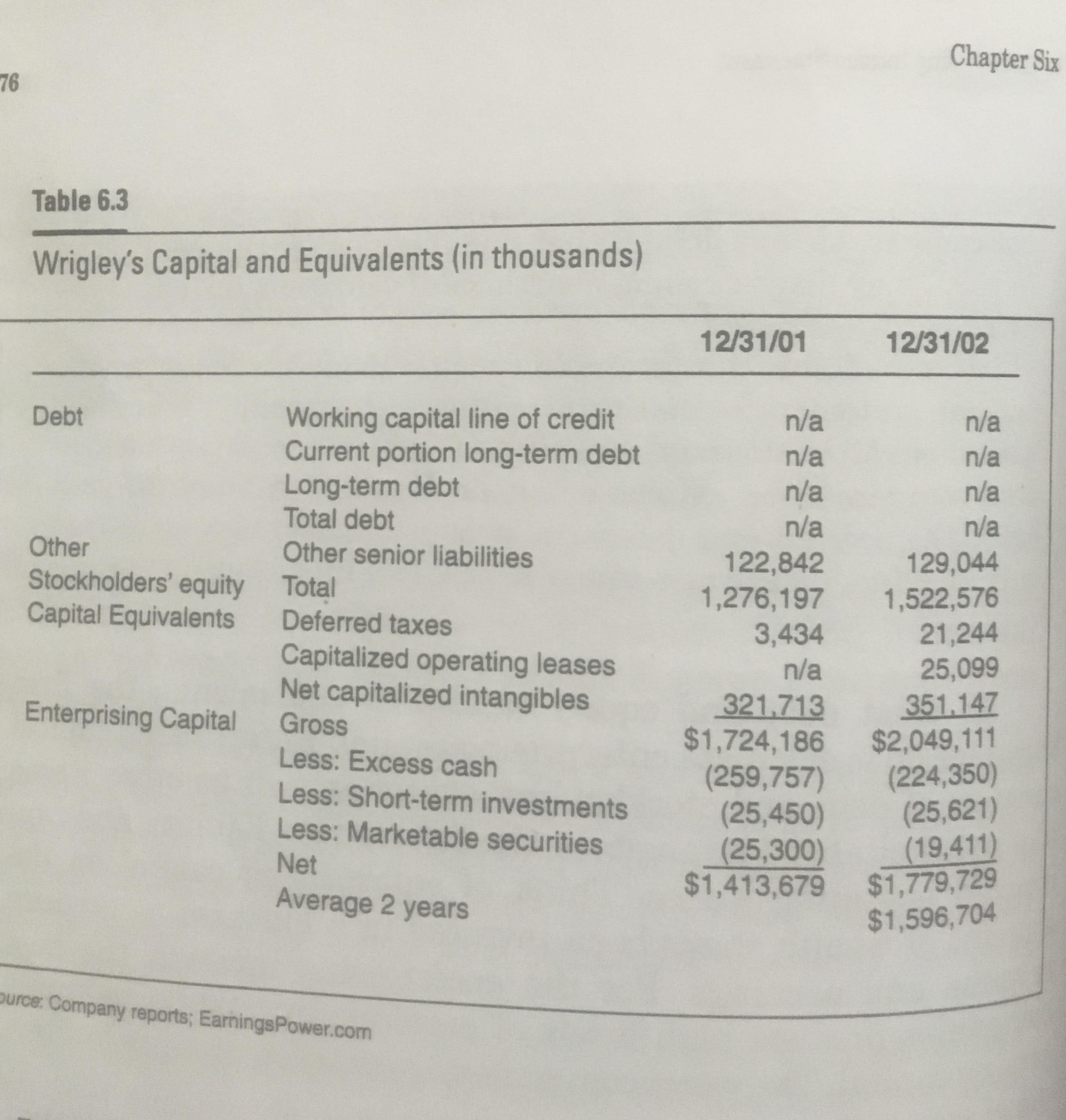

A snapshot form the book “Its earnings that count” by Hewitt Heiserman Jr who introduced the Earning Power Box to evaluate the earning quality of the companies using Defensive Income Statement and Enterprising Income Statement. This table provides how an Enterprising Capital is calculated which is needed in arriving at Enterprising Income Statement. Enterprising income is also referred as EVA as I understand.

In the table shown the excess cash is mentioned and it is defined as any cash above 2% revenue. This is stated in general and might have to be revisited based on the context.

PS: I have started reading this book and have not practically used it much. But book is very interesting and seems to provide a framework to evaluate our portfolio quality and take buy/sell/hold decisions based on how earning quality for the companies is changing.

Br, Sudheendra

1 Like

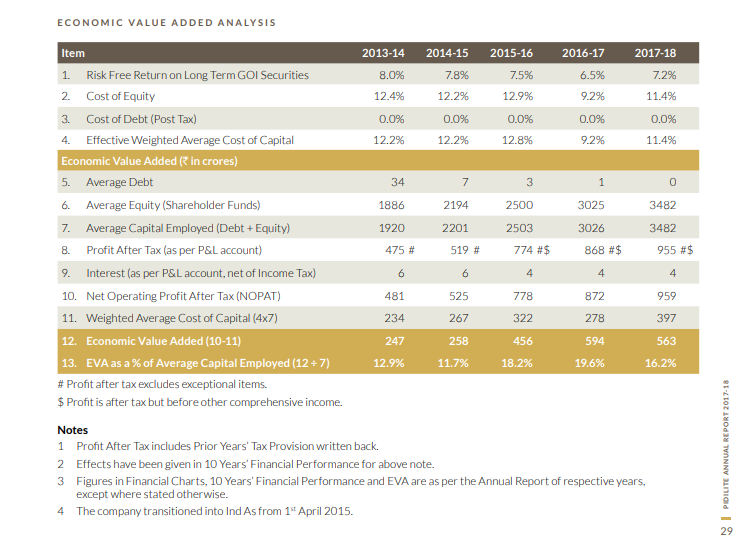

@dineshssairam , @bheeshma Taken this from Pidilite AR . Can you let me know how to evaluate this business through EVA figure ?How to get an idea about the current valuation on EVA Basis?

I have basic idea that EVA is the incremental difference in the rate of return over a company’s cost of capital. It assesses the performance of a company and its management through the idea that a business is only profitable when it creates wealth and returns for shareholders, thus requiring performance above a company’s cost of capital.

In my opinion, EVA is really iffy, mostly because Cost of Capital itself is really iffy. Market-implied, mechanic Cost of Capital can be used by CXOs to evaluate prospective projects, but it is really not suited for the minority investor in the business. More of my views on Cost of Capital here.

I personally use a flat 15% Required Rate for my Valuation purposes (As @bheeshma and @phreakv6 have also indicated). But think about what would happen if every business manager started demanding at least 15% return on their projects. There would be a recession for lack of employment and industrial production. As a business manager, you make decisions for millions of people around the world. An a minority investor, you only think for yourself. So, both these actions are justified.

As far as EVA and Value are concerned, the theory is that:

- If a company’s Return on Capital is above its Cost of Capital, it creates Value with Growth

- If a company’s Return on Capital is below its Cost of Capital, it destroys Value with Growth

But do all companies earning Return on Capital above their Cost of Capital make good investments? Of course not. There are also other questions that remain unanswered:

-

What is the return you personally demand on the Value created? Case in point, for every Rs.100 of Cash Flow, the business manager, assuming a 12% cost, may think he created Rs.833 of Value (100/0.12). However, if your personal demand for returns is 15%, you would calculate a Value creation of only Rs.666. You could see how both the approaches could change the expected price of a stock.

-

What is the risk associated with the Value creation process? Are you sure that the company will keep at it continuously? Won’t there be down years or regulatory troubles? You can’t foresee these, of course. But you can allow for a substantial Margin of Safety, thereby providing yourself a cushion. I personally use at least a 30% Margin of Safety on my Valuations.

Finally, BuffetFAQ is a wonderful collection of a lot of things Warren Buffet and Charlier Munger have said about business, valuations and everything else. At the risk of sounding boring, I would suggest that you read thought the website instead of trying to find a correlation between EVA and Stock prices.

The following thread contains the Valuation model I use to judge prospective investment opportunities (Basically an excel version of the answers I gave above):

Oh and before I forget, I made a replica of the Pidilite EVA calculation you posted. This could come in handy as a sample model for anyone interested in this thread: Pidilite EVA.xlsx (11.8 KB)

3 Likes

Much Helpful. Really appreciate.

1 Like

Excellent Presentation by Pidilite in their AR on Cost of Capital & EVA: