Any idea why the OPM are high compared to its peer Aro Granites ? Does the company has its own quarries ?

Aro Granites commands OPM of around ~10% and Divyashakti is having around ~16% and it looks both the companies are 100% export oriented units. Aro granites doesn’t have it’s own quarries. It sources from Rajastan/Tamilnadu and some portion is imported.

Look at Madhav Marbles and Granites, debt free company. Micro Cap, I bought at PE < 6, now trading at 8. Good Cash Flow but low promoter Holding of 38℅. Do some relative qualitative comparison with divyashakti.

Madhav Marbles and Granites Ltd does look interesting. Do note that 100% of the promoter holding is pledged. ROCE of 5% is unimpressive. Book value is 135 against CMP of 50 and dividend yield of 2% is also a positive. Looks like better days are ahead for the company.

Disclosure: Not invested

Madhav Marbles jumped close to 18℅ today. Exited from the stock completely. Volumes are not sustainable and the stock is volatile. It is available at cheap valuation and good dividends yield with cash flow positive. Good solid company but thinly trade. This company is a fantastic hedge during volatile markets. I have seen it through brexit, demonitisation and other macro events.

I will revisit it again. Good entry point is 45-55 range. Usually stay in that range.

DSG - Divya Shakti Group – a 900 crore (USD 180 million) conglomerate with a significant presence in Construction, Granites and Teak. more

Although Divyashakti Granites is a 100% Export Oriented Unit (EOU) of the group, it caters to all the requirements of the Group’s construction activities.

Valuation perspective: also here

With DSG expanding its real estate portfolio in Hyderabad and the sector slowly picking up India, Divyashakti Granites is well-poised for growth. As a novice investor, request VPs and existing investors for feedback and to share more insights.

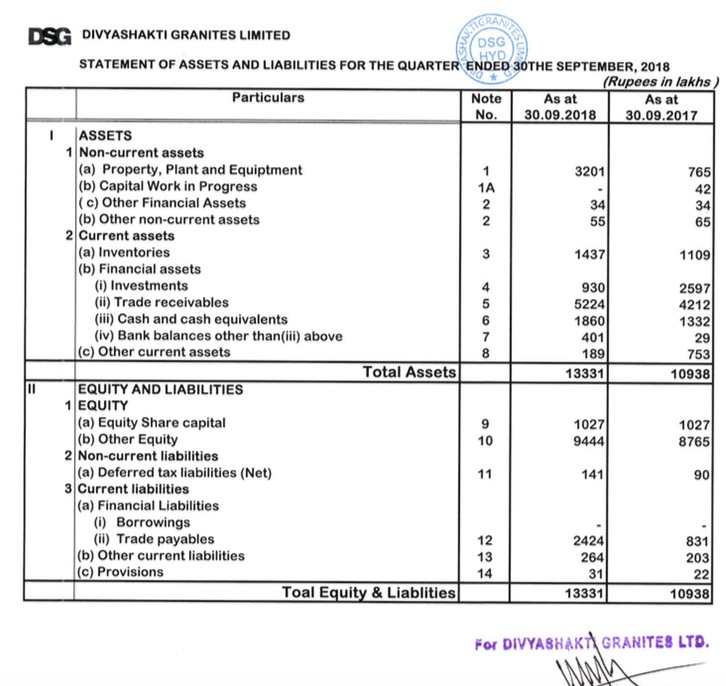

Promoter Holding up from 57.91 to 60.75.

With bad march quarter results and promoter holding up seems something fishy.

We may be in for a surprise soon in this counter I believe.

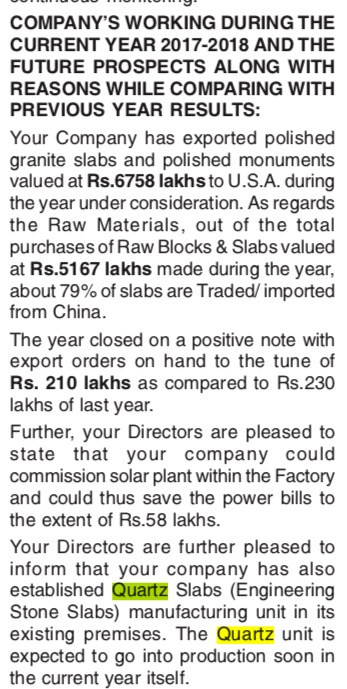

Seems to have done significant capex of 4x the net FA. Management have not mentioned any details about the capex except that they have established any quartz slabs manufacturing unit.

This is interesting. A quick back of the envelope calculation is as follows. They have added Rs 25 Cr in fixed assets. Engineered stone is a high returns business and is growing very fast in the US. Comparable company is Pokarna and taking that as base we can see Rs 25 Cr adding to top line once peak utilisation is achieved. Gross margins are at 40-50%. That gives us 10-12 Cr gross profit. Less depreciation at 10% is 8-10 Cr. At 33% tax rate, we can see an addition of Rs Rs 7Cr approx. Which is considerable given current bottom line.