The first thing I am finding risky (may not be amateurish) is your conviction to hold only 5 stocks with only 1.5 years experience in the stock market if I am correct. It would generally take a lifetime to build up conviction to have a portfolio of only 5 stocks. I had a portfolio of 8 stocks which I have now increased to 25 stocks after reading a number of posts in Valuepickr. Remember even market darling like infosys failed to give reasonable returns over the last number of years(it may not be a market darling now).

By position sizes, I meant diversification. That is not holding more than 20% in a single stock or let’s say 40% in a sector. It is also important to spread your investment either by averaging up or down (based on your investment thesis) and not invest all at one go.

There is a separate thread discussing best reads in investment books. I highly recommend you to read this thread. My top 5 investment basic books and why?

Really liked your investment philosophy of sticking to a checklist.I am in the markets for 10 years now and i too ran a concentrated portfolio but not with not so good returns but learnt a few lessons

I can give some insights from my experience

1.Running a concentrated portfolio during bull market doesn’t test you much but during bear market it gets pretty tough.

2. Getting rid of losers was difficult in a concentrated portfolio due to the high level of conviction in one’s ideas and risk management was tough in a downturn.

3.I found winning sectors in market change in cycles and have the right allocation in those sector leaders is very helpful.A very experienced and talented investor could have a sector agnostic concentrated portfolio only based on individuals but for people with less experience i found it was a better idea.

But i have also seen less experienced people with a proper strategy and emotion less mentality achieve magical returns in a concentrated portfolio so i wouldn’t totally shoo you away.Its just that the investors who have this kind of temperament is very rare.

If you are taking such a huge risk, then at least the returns should be commensurate. I mean, it makes sense to concentrate investment to as high as 35% in one single scrip if you are betting on a particular story, due to which you are expecting huge growth in EPS.

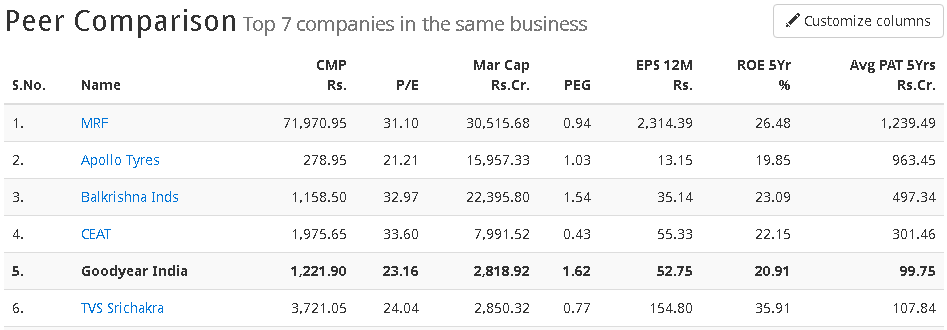

By my post, I meant that MRF and Ceat showed mind-boggling growth in price in the recent past. But, Good Year did not. And it is not likely to do so in the near future. Then why take the risk?

On the other hand, if you are aiming for stability and mediocre returns, then you are better off to diversify in many good scrips or invest in the Index, where return to the tune of three times the FD rates is achievable with near zero risk.

Not at all. I don’t mind, as long as the comments are helpful.

As I mentioned in the post, I don’t want such a concentrated portfolio myself. But I don’t want to diversify just for the sake of it. I am already tracking a few companies in different sectors. If they fall within my comfort for valuation, I’ll immediately spread my money.

Thank you for your comments @paraacbe. I will consider them as and when I require it. I just have one question: If the companies I hold are performing well (Regardless of whether it is in a concentrated portfolio or not) and are within my valuation limits, should it really matter how they are performing in the market? Especially in the context of bear markets, even if my holdings are getting beat, should my default response be to buy more of my own holdings / other stocks which can provide me better returns? I just want to understand why bear markets are difficult to manage (Except for the mental pressure maybe).

True about the first part, although I think that is a very specific example. I responded earlier saying that I would definitely load up on MRF, Eicher Motors and Page Industries should 2009 happen again. As long as we stay in a status quo, MRF and Ceat are overpriced according to my estimates. Do you have proof or some kind of estimate backing up your second statement? I’d love to hear it instead. Past performance is no indication of future performance. Being in a site filled with many investment gurus, we should agree to that statement without a doubt.

To be clear, I intend to ask you to share your reasons for believing so strongly that Good Year will show strong growth in the coming quarters. Please justify your strong belief, which you have shown by investing 35%.

By no means do I suggest that MRF or Ceat are to be purchased now. I used them as reference to show that good year is not a scrip which gives strong up moves, which is why I do not understand from where is the conviction coming.

It would be easy common sense answer to say that you hold great businesses and you should buy more in bear market but bear market workings are different in real.Good companies doesnt’ necessarily mean great stocks as stocks could stay down for really long periods of time.For e.g the case of RIL before current run,it stayed at cheap valuations for a very long period of time and if you hold something like that in a concentrated portfolio, it would lead to underperformance for a long period of time and trust me it will require a sage like detachment to hold the portfolio. Also bear market doesnt mean everything stays down ,for e.g. in 2009 -2014,entire market was in a bearish phase but pharma sector had a great bull run .In 2009 ,they were called defensive stocks and were out of flavour,so if one missed out on them in their concentrated PF,its a big opportunity missed .

Moreover these are pointers i could say from my experience.Concentrated portfolio is like a double edged sword,needs very careful management unlike a diversified one.

Poor @dineshssairam is getting pilloried for Goodyear. Questioning the source of conviction is right, however, questioning the allocation based on price performance is not really value-investing. Also, the price performance is anchored to 2009, whereas Dinesh made it clear he is an investor since last 1.5 years. If we look at the price performance since last 18 months, he has actually made the right choice.

However, when one looks at the growth of the two companies in terms of sales and profits, then that’s a different story. Dinesh - why does Goodyear have a stronghold in Agricultural tyres? Do you have insight into it?

A bigger question I have is, why do Indian tyre makers rely still on Natural rubber with its dependence of natural elements and not on synthetic rubber, which is more controllable in terms of cost ? Are you aware of any company planning to go the synthetic route?

I don’t understand why I have to believe that Goodyear India will show strong short term movements. Isn’t the crux of value investing buying great companies at a good price? Goodyear India is a great company. According to my valuation, it was available at a good price and hence I bought it. As far as holding it for the long term is concerned, I believe that there is a lot room for mechanization in Indian farming industry (Especially wrt Tractors). Research reports suggest that only about 20% of the demand for tractors have materialized and as such, there’s a long road ahead. Goodyear India is poised to fulfill a major part of that demand, being the leader in the tractor tyres segment. That’s really how I go about identifying investment opportunities in stocks, as I have already mentioned (1. Identify economic need - Mechanization of Indian Agriculture, 2. Identify Industry - Tyre, 3. Identify Companies - MRF, Ceat, Goodyear India, JK Tyres, TVS Srichakara etc., 4. Identify investment opportunity - Goodyear India).

True, but isn’t it folly to try and predict which stock will be laggards and how long they will stay down? All we can do is assign a price to the stock and buy/sell based on our research. I guess I’m simply trying to ask, if a company is great and the value you assign to it is far greater than the market price, shouldn’t you accumulate it, regardless of what type of market it is (And isn’t such accumulation much more logical to do in a bear market anyway)?

I have a few friends whose parents work on family farms. I’d be lying if I said they only prefer Goodyear tyres for their tractors, but they all seem to have a similar opinion in stating that Goodyear is one of the biggest names in the tractor segment. I have no insights into the innovations in the tyre segment. However, as a matter of practice, I regress a company’s raw material prices to their Operating Profits. Goodyear India seems to effectively handle price fluctuation in rubber and has been able to maintain its OPM regardless. I don’t have the regressed chart with me, but I guess you can look at them side by side:

I have learned from your posts. Thank you for taking time to respond. Good Year is a great company, with a reliable management. There is pretty much assured capital safety.

Positives:

In the last ten years, they have had almost all years of positive Free Cash Flow.

Zero debt.

Transparent management. No skulduggery. The economy has been bad for most part of the decade, therefore the growth of sales of the company were also mute. No harm in that. They didn’t do any furnishing of the books to paint a different picture. Much thanks for that.

As a result, this company could be called “Bear Proof”. Due to good fundamentals, the fall will be limited.

However, my concern is (here comes) the company does not promise growth. Therefore, its PEG is high 1.62

Allow me to present an alternative, which too has all the above goodness of Good Year and also promises growth: TVS Srichakra Ltd.

By no means am I suggesting that it be bought right away. But, in a correction, when its PE is between 10 and 15, TVS will be a great bargain. Pls revert with your views.

Good year PEG is the highest. Means, one would pay the most for one unit of growth. Whereas, PEG for MRF, Ceat, TVS Srichakra is better, in fact, they are better on other metrics as well. (I do not mean that to suggest that they be bought right away; waiting for correction is prudent)

All in all, you may still prefer Goodyear because it may fall in your circle of competence. However, for me, I have no such advantage. Therefore, I hold a different view.

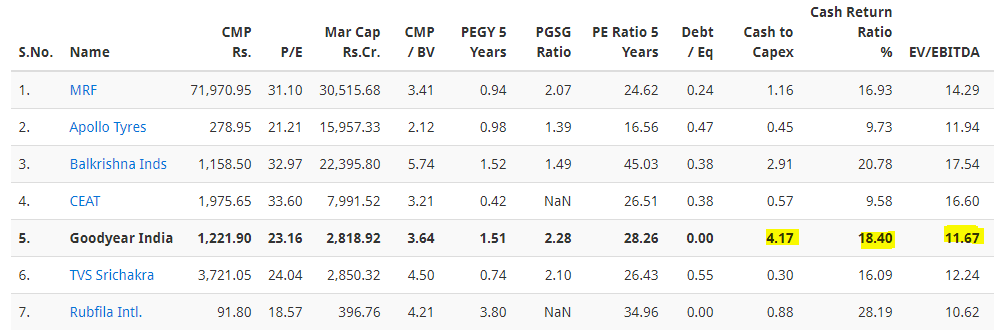

With all due respect, the P/E and by extension, the PEG Ratio, are good enough for filtering out bad stocks. But as far as making an apples-to-apples comparison is concerned, I place the EV/EBITDA Ratio well above all valuation ratios put together, simply because the EV/EBITDA covers two important aspects of the company’s financial status that the other ratios don’t: debt and depreciation (Capex). The EV/EBITDA is very difficult to game when compared to the Price Ratios as well.

Now, you can add EBITDA Growth to the denominator of all these EV/EBITDA values to arrive at a figure similar to the PEG, but you can clearly see why Goodyear India scores a lower EV/EBITDA (Therefore making a better target): it has lesser capital requirements and literally no interest obligations. This is also evident from the exceptionally high Cash to Capex and the CRR (CRR is the post-tax Owners’ Earnings on Invested Capital, a Ratio famously known to be used by Warren Buffet). In a capital intensive industry, I much prefer a company which can produce an industry-standard Returns while locking up lesser cash in its long-term capital than the industry. They can always use this additional cash to buy growth via acquisitions or build growth via geographic diversification.

Even then, I agree that MRF also makes a great bet. But the final answer to all price-related questions (At least to me) is my own valuation model. MRF was simply too costly. My valuation put MRF’s fair value at ~Rs. 53000 when the stock was around ~Rs. 62000. So unless, MRF comes back down to ~Rs. 61000 (Rs. 53000 * 1.15 - 15% increase for a year passed), I will not consider buying it.

I only ever use the Ratios to filter out bad stocks. I don’t use them to make valuation decisions.

I have understood your perspective. I appreciate you sharing your thought process.

You have correctly considered the Valuation part, and the bit about the company’s ability to generate FCF, but what remains to be considered is a very important feature, for which the market readily pays a pretty penny: The Future Growth.

In other words, once we establish that the company is good, with a reliable management and a dependable business model, we need to see that for the price we are paying, which company is giving the most:

Future Growth.

It is my opinion that, Goodyear is priced low, even in this bullish environment, because the market does not believe that it will grow at a pace as good as its peers.

I suggest, once we settle on the fact that the overall health of the company is good enough and management is reliable, we should shortlist them for purchase only if they have ability to capture growth in near future.

Donald, too, emphasized on this point here. Read point #8.

I have seen Donald’s post before. But it talks about capital protection, doesn’t it? Correct me if I am wrong. Here is what I believe about growth when it comes to investment:

I think I mentioned this exact quote somewhere above as well. All growth comes at a price and the actual question is “How much are you willing to pay for that growth?”, which circles back to valuation i.e. Growth is already part of valuation.

I agree with Donald in saying that the market assigns more price to high-growth stocks (Regardless of the type of market - I feel), but in the very long term, the market tends to pick up after value. It may take more time in under-developed markets like India. But it happens nevertheless. In short, I don’t care how the market values Goodyear India one or two years from now or what type of market it will be in. I have invested in the hopes that I earn my calculated value in PV terms.

Please note that I’m talking about all this from my theoretical knowledge. Practical knowledge (Which I lack) is much appreciated here.

Thank you for writing. The PGSG is the Profit-Growth-to-Sales-Growth-Ratio. I personally use 10-year average Profit and Sales Growth percentages to arrive at the Ratio. In technical terms, this is also called as Degree of Total Leverage.

If DTL is between 0.75-1.25, it means that the company’s profits are protected from external shocks (Well, at least historically). However, that’s not always the ideal situation.

In an inflationary world, DTL > 1.25 is preferred, because you are basically spending at historical rates (More Fixed Expenses, Debt at lesser interest) and earning at the new inflation-additive rates. In contrast, in a deflationary world, I’d prefer having a lower DTL.

Since central banks always aim to keep inflation at a minimal level (4-6% is the current RBI target), I would say, anywhere from 1.5-2 DTL would be ideal (Higher is not better, though). But that’s my own highly subjective opinion. If you could not be bothered about all this, theory suggests that you stick to companies with a DTL of 0.75-1.25.

Not only capital protection during bear markets, but also share price appreciation during good markets.

As per WB, quoting from the article,

“Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return.”

If the growth of company A is 15%, and for another its 4%, then it is going to make a huge difference in the very long term. No debate in that.

However, if ones wants to buy a stock in spite of knowing that it lacks in future growth, then lets do it admittedly.

Warren Buffet is talking about Cash Return Ratio in that quote, which Goodyear India is able to comfortably generate at industry-standard levels, even while requiring lesser than industry-average Capex. Help me understand how that quote relates to sales or profit growth. Thank you.

Again, I mention that all growth has a price. If Company A grows at 15% and Company B grows at 4% and they both are equally priced, I will buy Company A, agreed. However, that’s not the case at all in real life. The market would have already assigned a higher price to Company A. So the question really becomes “Which company is undervalued given specific growth prospects?”