I have largely sold out of DHFL. While I would still wait for the appointed committee’s response to the allegations, I believe the environment is getting more and more difficult for DHFL to bounce back. With their Bond yields trading at steep discounts, it would not make any sense for a lender to lend to them directly. They could just purchase the bonds instead. If DHFL does manage to raise funds from a lender, it would be in terms unfavorable to the company, which again isn’t positive news to a shareholder.

This episode has reinforced two things for me:

-

Highly leveraged businesses will remain the riskiest of all. A small change in perception could snowball into creating a massive roadblock in their operations. This is why I always tend to keep them as a smaller portion of my overall portfolio.

-

I should be more thorough in evaluating a company. Although the Cobrapost allegations were new to everyone, literally none of us know enough to comment on whether they were true or false. They may turn out to be one or the other, but the point is, I should have done more work. This is entirely on me.

In other news, I purchased sizable quantities in Heritage Foods and smaller quantities in Dhabriya Polywood and Cera Sanitaryware. As mentioned earlier, I have around ~20% Cash left and by the end of March, I should end up with at least ~40% in Cash. I am tracking a few more companies as well in my watchlist. I hope I find one with a wide enough Margin of Safety by March or April (Including the ones already in my portfolio).

Hi @dineshssairam Are you still holding Mirza international? I was trying to find details about their investor presentation or Q3 concall(if it happened). But couldn’t find any detail.

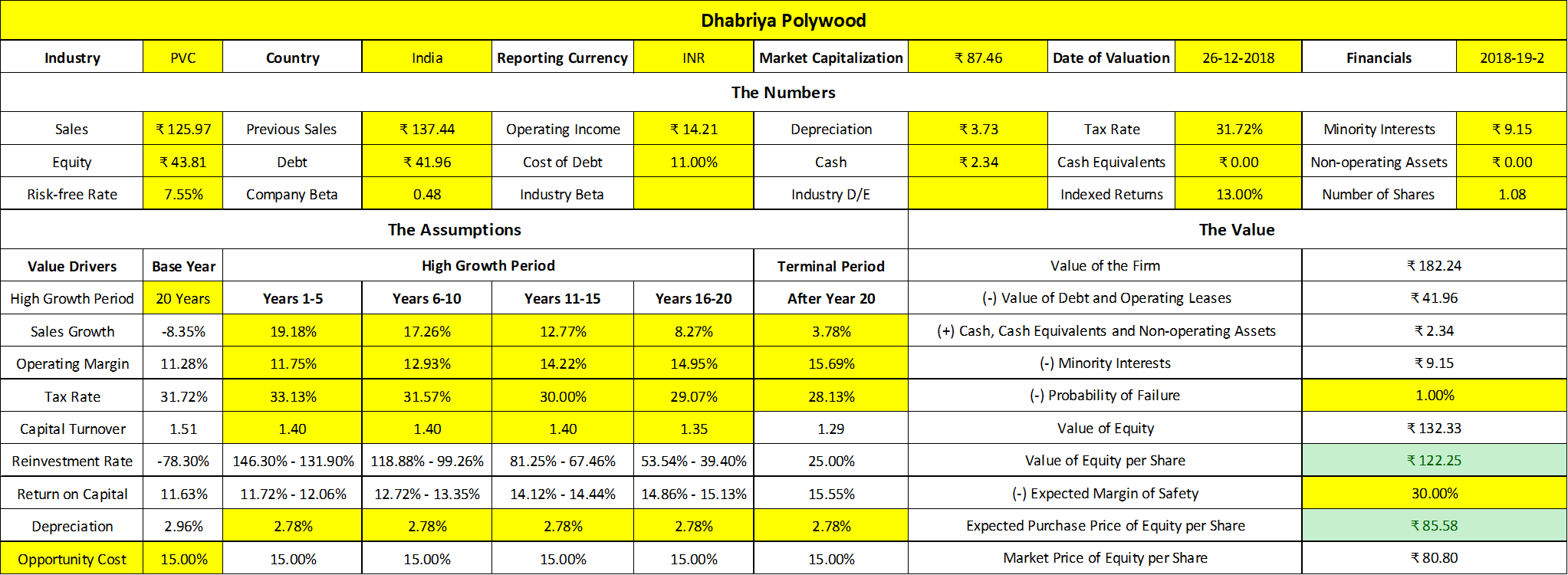

Hi @dineshssairam can you throw some light on the rationale of Dhabriya plywoods, my personal take is there is an abundant growth opportunity in the space they are operating, wanted to know your investment thesis in terms of valuation etc as I am rookie in that, thanks.

Yes, I still hold Mirza. It’s about ~3% of my PF. But as mentioned earlier, I am not adding to the position until I am convinced they can generate money from their retail portfolio. Right now, they are burning cash like crazy. When I initially invested in it, I wasn’t aware that they’d go all-in in to retail like this.

I hope this helps:

Thanks @dineshssairam any pointers on the valuation that you might have arrived before getting into this.

I have a suggestions regarding your PF and style.

You tend to overthink a lot. And you have this thought process that everything can be quantified through excel. You completely ignore qualititative facts. If everything could be quantified valuations would be a walk in the park. Just hire a few number crunching excel junkies and you have the keys to valuations.

Valuations is an art. You cant quantify everything. I hope the experience with DHFL was a humbling one on that front. You cannot value a poor lender. Lending is a commodity business where costs are everything on top of that. Let alone dodgy corp governance. But that seemed to have been priced in as per your models right. I do agree, there is a point upto which corp goverance can be priced in. If you cant trust the reporting then what are you crunching on excel is the question.

You cannot quantify everything.

Also Buying a dhabriya at a similar valuation to that of greenply in a similar space is something I would like to question. Do clarify …

Just my opinion since you wanted feedback on your pf and style. You are a great investor already and I think way ahead of the average well informed Indian investor.

The key tracker for me would be the Debt level, which is a bit higher than what I would be normally comfortable investing in. The company produces very good cash flows, but the interest cost eats a chunk of it The promoter has promised to pay down the debt in the coming quarters. I would be monitoring that action closely.

We cannot quantify everything. But we should try to. I don’t know if that made sense or not. But this is exactly what I have been saying in several places. Management Quality or Company Quality isn’t something that floats in the air. We should try to understand how they affect the company and how it translates into value. I’m not claiming that I can do it successfully every time, but I will do it every time regardless. After all, investing in stocks is a game of probability. There’s nothing deterministic about it.

I will wait for the response from DHFL’s appointed committee as I have already mentioned. But yes, if one believes that the numbers of a company are cooked / incorrect, one should not Value the company at all.

However, my reason for selling DHFL so early wasn’t because I don’t trust the numbers (I’m still on wall about it until the official response comes out and it will be based on how well placed their arguments are), but because the environment in which DHFL conducts business is becoming a quick-sand of sorts every day. I believe it will be very hard for DHFL to pull itself out without damaging the underlying business very badly.

Big corporate actions like a Demergers are always tricky. I’m trying my best to wrap my head around how value is created/destroyed in moments like this. But as of now, I would much rather avoid a company which is going through that phase, than risk doing a valuation of which I have only a half-baked knowledge.

Of course, the industries are quite similar. So, if a stock like Century Ply, for instance, provided a similar Margin of Safety compared to a stock like Dhabriya Polywood, I would swap it for Century Ply in a heartbeat. Perhaps when dust of the demerger is settled and Greenply / Greenpanel get into 1-2 years of functioning as a separate entities, I might be more knowledgeable in valuing them.

Hello dinesh sir are you tracking tyre sector closely particularly jktyre it is available under book Value and one fourth of revenue

Not really. The only company I’m tracking in the CV space is MRF.

Just curious. What makes MRF worth tracking? Is there a competitive moat? Brand name maybe, or is there more to the story?

I have a friend who works high up in MRF’s Marketing Department. One day, I happened to have a lengthy conversation with him about how things are done at MRF. The way he put it really impressed me.

I don’t want to reproduce the entire conversation here, but a summary would go like this:

- The decision making group of people are tightly held and so, decisions are taken in a swift manner. Even the Middle Management is not involved in this process, so as to make it quicker.

- Innovation is given an equal footing along with hard work.

- Customer queries are handled ASAP i.e. If 100 customers have complained that X model tyre is slippery at very high speeds, the next model of tyres are specifically produced to not be slippery at very high speeds. Of course, he also said it’s not possible to solve every problem, but they pick the ones worth solving.

- A couple of examples of how MRF was able to maintain Pricing Power with their suppliers because of the brand.

- A couple of examples of how customers prefer MRF because of the brand and how MRF is good at picking market segments in which to sell in.

We discussed a few other related points. But the amazing thing was when I got back and looked at the financials of MRF, I could relate a lot to the story he had just told me. When I hear or find out stories about a company and I could put them easily next to its numbers, I’m hooked from that moment.

Of course, price is always the bigger question for me. Right now, I don’t think MRF offers enough Margin of Safety. I would likely wait for a 18-20% drop from here and then start nibbling (If at all the drop happens in the first place).

Its already at 52 week low i think…It has poor ROE and poor sales growth

Thanks. Good to know it has pricing power with both suppliers and customers owing to its brand. That does make it worthy of deeper study.

An 18-20% fall will definitely make it reach a safe place technically, as that is where it broke out in September, 2016.

Goodyear India posted lackluster results today, largely on the back of a sharp increase in Purchase of Stock-in-Trade. This also happened last Quarter too. Seeing as how Goodyear India only purchases Stock-in-Trade for their CV Trading business and not for their Farm Tyres business, it looks like they are stocking up on CV tyres to be sold later on.

Meanwhile, MRF also posted muted results for the last two Quarters, because of a sharp increase in Cost of Materials Consumed, meaning their RM procurement had become costlier. I just checked out CEAT’s past two Quarter results and their RM prices also seem to have increased.

All of this, of course, indicates to increasing rubber prices.

Interesting times ahead for the tyre industry, I think and a very good time to start looking at your cards for investment opportunities down the road.

Could not fully understand your final view… still bullish on Goodyear India?

Thanks.

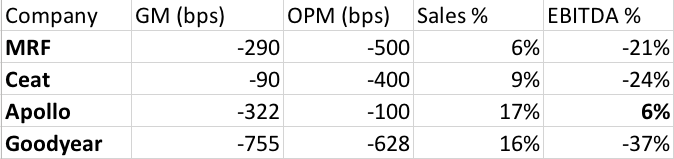

Looking at the tyre players’ December quarter reminds me of Tolstoy’s opener in Anna Karenina - “Happy families are all alike every unhappy family is unhappy in its own way”

It looks like MRF wasn’t able to grow sales much and the RM costs bit while the OPM took the worst hit because of lack of sales growth.

Ceat was the least hit on the RM front but that means little when sales doesn’t grow much which means that they took a bad hit on the OPM which made their EBITDA degrow almost as much as MRF.

Goodyear took the worst hit on the RM front among the four and since their OPM was the lowest among the 4 in the quarter, the sales growth of 16% still couldn’t save its EBITDA which dropped the worst among the 4.

Apollo seems to have fared the best among the 4 having grown its EBITDA despite the RM hit mainly because of the big topline growth.

One quarter is nothing to draw from but for tyre companies, this quarter on will separate the x from the y (that phrase has become so trite).

Yes, of course. I was just pointing towards a possible industry trend, that’s all. I am still bullish on the fact that Indian Agriculture needs a massive overhaul with consolidation of lands parcels and automation / removal of manual labor. I’m not the best person to judge when this will happen, but this is the ‘perfect state’ and it has to get there sooner or later. Let’s see.

That’s why I noted that it’s interesting that Goodyear India’s low OPM isn’t due to higher RM costs (Which would be attributed to their Farm Tyres Sales). It’s due to an unnatural increase in the stocking up of CV Tyres (Purchase from Goodyear’s other subsidiaries and held for trading within India–low Margin trading, basically). The Cost of Materials Consumed (Attributable to Sales of Farm Tyres) has indeed increased too, but not nearly as much as MRF’s or CEAT’s. It’s too early to tell why the management is doing this, though. I would personally wait for the management’s commentary in the AR.

A breather would probably be the fact that in Q2, their Cash Equivalents was still as high as ~Rs. 580 Crores and their Working Capital position very comfortable (Negative, if I’m not wrong). in Q3, the Depreciation has only increased Marginally, meaning they didn’t do a lot of Capex too. So, regardless of slow quarters, they’re largely able to maintain the excellent strength in the Balance Sheet.

We also have to note that the Ballabgarh plant remained closed for several days in Q3, due to the Delhi government’s orders to stop production w.r.t. the pollution issue. I think this could have been another reason why the management chose to stock up on CV tyres so much. But I’m just grasping at threads here. It would be much better to just wait for the Annual Report for all explanations.