It’s a bit patronising, however cost of capital and discount rate one uses to value stocks are very different things

Anyway I think I’ll wait for the full book when you publish one not just cost of capital lesson

If you could elaborate a bit more, that would be helpful.

The Discounting Rate is your Cost of Capital or vice versa. If I may list down the process, it would go like this:

- If I don’t invest my money in this specific company, where else would I invest it with the same amount of Risk?

- If I invest it there, what is the likely return I will make?

- If I use this Rate of Return as the Discounting Rate for the previous stock’s valuation, what is its value?

- Does this value provide me enough Margin of Safety?

And so on. At least, that’s how I understand Cost of Capital.

If you have a different view where Cost of Capital and the Discounting Rate are disparate concepts, I think it would be an interesting POV to discuss.

2 Likes

Discounting Rate and Cost of Capital is the same for all practical purposes, if you use it to value stocks. The main bone of contention is in the usage of “beta” to arrive at the discount rate to be used in the valuation of cash flows.

if you breakdown beta into its individual components its basically correlation multiplied by volatility. When you look at beta this way, it becomes clear why it may be not useful to a certain class of investors (who are in the minority) it makes sense for the majority due to the way people view the stock markets.

People generally ( even the accomplished ones ) get perturbed with market falls and if you have significant money invested in a co and it falls by 50% overnight and the market falls by lets say 10%, the normal tendency is scale back on the optimism even though one may still overtly be optimistic. If the market is going up and your favourite stock is stagnating, then one quickly loses interest in extolling its virtues.

There is absolutely nothing wrong in having this point of view but when does portfolio changes looking at price action then implicitly one is confirming the validity of Beta as a measure of risk.

To re-iterate there is nothing wrong in letting the stock price tell you the future course of action , however then one should actively use CAPM because its a straightforward measure of risk and one rooted in accepted statistical principles and the common way people invest in stocks.

Where “beta” is futile is if you have better and different business insight not commonly available to the normal public and are willing to wager on it coming to pass. For such investors, beta should be ignored. So it logically follows that if you are not a adherent of “beta”, then you should have some unique way of looking at the investment. Else, in my view use beta to calculate the cost of capital/discount rate.

Just my views on this (as the discount rate is probably the most important factor in formally valuing a co)

Bheeshma

2 Likes

I agree with this largely. Let me quote myself from the above mentioned blog post:

With all that said, I still feel like there are some loose ends I would like to address:

I generally don’t use the CAPM or arrive at a WACC using a similar method. WACC is useful as a hurdle rate for companies. The CEO, who decides on new investments thinks for the company—indeed, he thinks for millions of people around the world. So it would make no sense for him to ask the above questions. Therefore, using a scientific method to arrive at a WACC is the most logical course of action for the CEO (We could argue days on end about whether the Five-factor Model is better than the CAPM or not). Similarly, it would make no sense for an individual investor to consider using the WACC, because an individual investor thinks only for himself and not for millions of people around the world. In essence, the CAPM generalizes Risk. However, Risk is very, very personal. In fact, it’s my humble opinion that we haven’t even scratched the surface with understanding Risk. The article Averse to reality by Nobel Laureate Dr. Richard Thaler should be a good starting point for you to understand what I’m trying to say.

If you are adamant about using the CAPM to arrive at the Cost of Capital, use the Bottom-up Beta-based CAPM instead. It solves at least one problem with the CAPM—Specific Financial Risk.

Do You Know Your Cost of Capital? is a wonderful article by the HBR that glances over how one could arrive at a near-perfect Opportunity Cost for an investment. It involves too many moving parts in my opinion, but hey, incremental knowledge never hurts.

Buffett FAQ is a treasure trove of what Warren Buffet and Charlier Munger have ever said about Investments and Valuation. You might very well find a better answer than mine in there.

When in doubt, use a Margin of Safety. Demand 3% extra. Demand 5% extra. Demand 10% extra. Discount like nobody’s watching.

1 Like

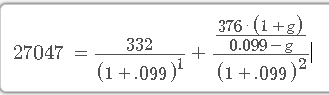

Beta looks so much into past performance, its the equivalent of saying the market has been historically valuing the stock at a PE of x and if the current PE is below x its a buy. Anyway the beta argument is probably immaterial. Everyone’s required rate of return is going to be more than the risk free rate of return. Lets for the sake of seeing past the beta argument agree that everyone’s required rate of return is 9.9% as per the spreadsheet.

The spreadsheet has 2 more issues, firstly if there are marketable securities and investments on balance sheet they are ignored. Probably a spreadsheet preparation error as cash equivalent are shown as zero. This issue than goes into the second issue of recapitalisation which is calculated at 3pc because cash equivalent is zero, all differences are taken as fixed assets

Anyway, if I take from last years’ p&l, gross profit (-) interest (-) depreciation to arrive at net profit

(For an honest management over long run recapitalisation should equal depreciation)

I get last years figure of 332.

Reverse calculate growth with the below formula, the market is pricing a growth of 8.6% as per link below:

Although its still high, if GDP is expected to grow at 7-8pc for a foreseeable future, then Page would be expected to grow atleast as much as GDP and hopefully more

Disc: Not invested in Page

Beta is just one part of the equation. The Risk-free Rate and the Market Risk Premium also play a part. All three of these are in constant flux and together, form the ‘P’ in the P/E Ratio. I don’t understand how using the Beta to calculate the Cost of Capital equates to doing a rather bad Multiples valuation. Please explain if possible.

What part of a high level assessment did you not understand? Clearly I didn’t perform a complete valuation. Me and @iivans were having a general conversation about Valuations and I happened to show him how I might have valued Page in 2013. If you follow my valuations (Which I realize you may not), I do include Short term investments as a part of the value of a company.

Depreciation is done on Fixed Assets alone. Current Assets, especially Cash does not have a Depreciation. Cash is measured at Book Value always. More of my opinions on this in case you are interested:

I personally think every single part of a company’s value should be looked at and justified separately during the valuation process. If you think no justification is required and a click-of-the-button solution is the better way around, then I don’t mind. If this method of valuation works for you, all the better. More power to you.

2 Likes

Hello Edward, your calculation seems very interesting. Can you please explain this fomula.

Based on this calculation, the current valuation expects company grows at 8.65% for how many years?

His formula is based off your sheet

Instead of arriving at valuation it plugs in the value already known (market cap) and gets growth

Your sheet puts a growth and then arrives at market sheet

If you wouldn’t use excel npv formula or if excel did not have this built in, you’d use this

@dineshssairam if you havent read already https://www.moneylife.in/article/how-loans-to-promoters-and-poor-disclosure-was-used-to-boost-net-worth-loan-book-and-valuation-of-dhfl/55885.html

ok so the company has the keep growing at 8.65% fowever to maintain its current value. In other words, it has to do more than 8.65% per year to command a higher valuation. I find it a big strech, but everyone has to bet on their respective conviction - so we come a full circle to my initial conclusion

The primary accusation of this article is that the deal was so crooked that it was specifically hidden from the public eye. An investor only has to look through the financials and/or Annual Reports of DHFL to understand that this clearly isn’t the case.

Form AOC-2 of the 2016-17 Annual Report includes a detailed description of the deal.

The Subsidiary filing for 2016-17 contains the financials of the deal.

CARE’s Ratings summary would have also contained the details of the deal (Of course, this one I’m assuming based on regular practices of the Ratings business).

The company cannot be held liable because the investor cannot spend time to read through the reports and numbers for the year. With that said, I agree that the deal is complex. I just don’t buy the core argument that this was intentionally hidden from the public eye.

The way I see it, the entire BFSI industry and more so, the NBFC industry will be observed under a lens until noise of the ILFS crisis / Yes Bank situation lingers. It’s the way media works. If they were really convinced that something foul was going on, why wait until now to report it? It happened some time back and the same ‘analysis’ could very well have been performed back then.

Disclosure: DHFL is 9% of my Portfolio. I purchased it one more time during the recent fall. I may not add further, unless it falls considerably. This has nothing to do with the valuation or anything else, but my personal thumb rule of not letting a BFSI firm be way more than 10% of my PF.

4 Likes

Think the issue is as much about disclosure as much as the fact that the part of net worth is actually sourced by debt thereby taking up the leverage even higher. Only question is - what percent of total capital is infused in this fashion. If its negligible, it doesnt affect the financials - just a question on governance and practices which I guess is more than priced into today’s price.

On an unrelated subject, yields have now softened by 0.6-0.8% and hence costs for further fund raising, if any, should come down to that extent. Only issue is, I was speaking to someone holding a good chunk of their bonds and the liquidity for it is very poor.

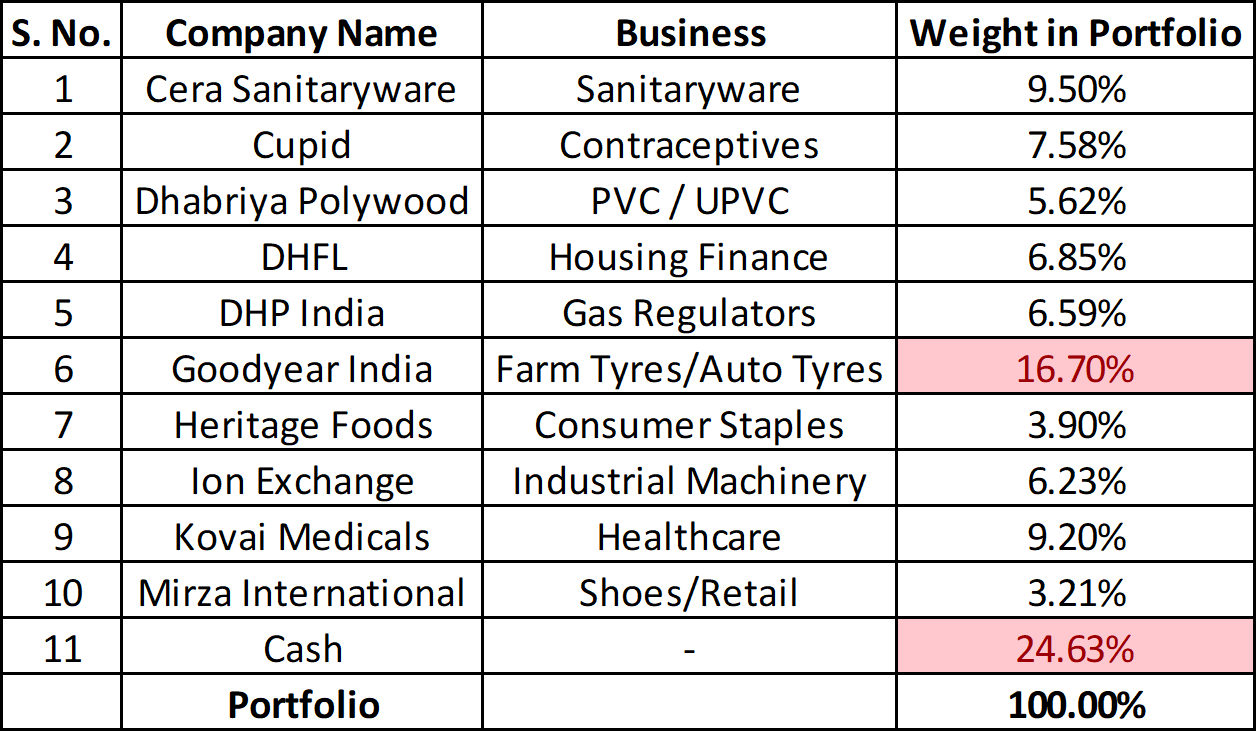

Portfolio update:

I have a sizeable amount of cash coming my way. So, I have started nibbling again. I’m planning to ‘park’ at least 10-15% of my overall PF in a liquid/debt fund, as I’ve always wanted to.

Some notable changes to the PF:

- Entered Dhabriya Polywood. It’s a small company selling PVC/UPVC doors and windows. They have a decent market share too and have a passive advantage of being an organized player in an otherwise largely unorganized market. A good optionality is in the form of Dstona, a brand for their fake marbles that they’re trying to create for their new plant. Regardless of Dstona picking up, I think it’s a decent bet.

- Almost doubled allocation in Goodyear India. Goodyear India remains my core bet. So, no surprise that I’d do this.

- Increased considerable amount of allocations in KMCH, Ion Exchange and Cera Sanitaryware.

- Increased allocation to a tiny extent in DHFL and Cupid.

As far as Heritage is concerned, I missed the bus when it hit Rs. 419 during the recent midcap correction. I’d love to add more if it falls closer to Rs. 450-470 levels. I didn’t increase stake in DHP India, but again would love to if it falls back to my original purchase price around ~Rs. 490-500. I would like to keep the stake in Mirza pretty constant until I’m convinced about their plans in Retailing.

Here is how my PF looks currently:

8 Likes

Ion exchange - formed in 1964 and became whole Indian company in 1985. Why still the market cap is only 560 crores? Is it pointing to the competence of management? Is it a value trap? Just asking and worth mulling

With due respect, that’s an extremely silly way to see things. One of India’s largest FMCG players, Hindustan Unilever Limited, created very little wealth for Shareholders from 1997-2010. That’s 13 years and no movement in the share price. This doesn’t automatically make HUL a dummy company and the promoters incompetent. In fact, the company has been largely value accretive ever since.

I buy stocks based on cash flows I think the company will earn and a very conservative price I’m willing to pay for those cash flows. If I do this, is it completely assured that the market will notice the gap somewhere down the line and buy the gap? It’s likely. But is it unconditionally true? Of course, it’s not. Nothing is unconditional.

I said it elsewhere and I’ll say it again. Price is 100% in the past and Value is 100% in the future. I’m paying for the future and not the past. My upside is the gap between the price paid and the actual value. My downside is (Apart from the obvious issue of me being wrong in pricing the stock), the market not noticing the gap. I get both the upside and downside by making the purchase. I can’t have one or the other.

The market can stay irrational longer than I can stay solvent. That’s the risk for every investor.

7 Likes

hey dinesh

your portfolio looks solid and may give you market beating returns. i was having a look at good year india and would seek your views for investment in the same.

- why did you choose goodyear , there are other which have been executing their business with good results like mrf and tvs sri chakra. what different is goodyear doing or what makes it your only bet from the tyre spce.

- past performance of goodyear has been avergae to above average at best. sales have hardly doubled in last ten years and the same goes for the bottomline. where do you see incremental profits and cash flow coming from. from a valuation perspective the stock is decently priced at pe multipple of 18.

- The automotive downturn has just kind of begun from the last festive season, any ways or means that sugggests that it will not be a pro longed one.

regards

divyansh

Well, I’m not betting on CV tyres with Goodyear India. I’m betting on Farm Tyres. In the CV tyres segment, I’d buy MRF at the right price. At this point, CV tyres are a good optionality for Goodyear India, but not the major thesis for investment.

The company hasn’t grown as much in the past becasue there has been no real push towards automation in Indian agriculture. But I think this is only inevitable. The current setup is vastly non-profitable to many farmers. Indian agriculture is in dire need of a mass conglomeration and automation across every state.

Besides, Warren Buffett once said that the key to measuring quality in a company is consistent greater-than-industry RoCE and RoE, not consistent profits. Capital Allocation skills are key, because if a management is good at that, they can create the maximum wealth when there are tailwinds and preserve wealth when there are headwinds. This is obviously very helpful for long term investment.

1 Like

I have been dealing in agriculture related products for last many years. I feel if you’re focusing on tractor tyres , the scenario is not very positive.

We are in a bubble zone in as far as tractor tyres are concerned. Companies are selling tractors with very easy credit terms even to small farm holders who don;t even need tractors .How these small farmers would pay back , that is big question mark.

Tractor as a status symbol has played out upto its full extent and now it’s time for this bubble to burst. Can foresee hard times ahead for tractor manufacturers ,financing companies as well as for accessories suppliers.

(the above scenario is playing across India . Wanted to enter this business ,hence did lot of inquiries )

The only respite is replacement market for big farmers.

10 Likes

Is it possible that stock price does not move for a few years despite good RoE and RoCE? If so what good is a stock for retail investors unless the company pays dividends? Wipro took 19 years to reach the same price again, but in the 19 years it posted good RoE and RoCE, but it is yet to reach its highest price. I know it was quoting at astronomical PE but my question is about the reliability between RoE, RoCE and price.

@dj123 There was a good discussion on Good Year in this thread, check that if you are interested.

This is a interesting news. I know how difficult it is for small farmers to buy tractors. I didn’t know the situation was in “bubble territory”. If you could point to articles or papers showing the same, it’ll be helpful. Thank for your views in any case.

Regardless of a slow down, I think Goodyear India is fairly cheap. I mentioned that there will be an inevitable move towards automation in agriculture, but of course I didn’t Value Goodyear India using figures far better than what they have historically managed. I valued it conservatively. If there’s a bubble really waiting to burst, I think it’ll just be another good opportunity to buy the stock.

My core thesis is that Indian agricultural lands need consolidation and automation inevitably. If you think there’s something wrong in my assumptions along these lines, please feel free to correct me.