is it finalized that at what price prom. will do Pref allotment? (95-100 Rs). I thought it is linked with some formula with VWAP of historcial share price

Based on that price I think it’s around 100 bucks

Here goes the official announcement - the price is 101.88.

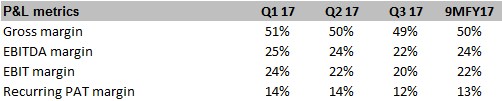

Company has announced Q3 results. Numbers are decent.

EBITDA margins continue to remain above 20%… Q3 last year had a shut down hence comparison would not be right.

Company seems to be on track to do ~ 17-18 Crores of PAT this year.

Few questions that need further investigation

-

What has been the volume growth for the company in this quarter?

-

EBITDA margin declined sequentially to 22%- any thing structural here?

-

Any update on Sulfones and contribution of that to the revenues?

3 Likes

I am doing some more research on DMCC- found an interesting document on one of their products - called Diethyl Sulfate. It is consistent with what the management is saying- getting into products where there are not many players. In this case globally three players are there as per this document. The source of this document seems to be Government hence seems a reliable source.

The document mentions few interesting points

DMCC is the only manufacturer of the product in India

They are increasing the capacity to 6000 tonnes p.a in the light of global export opportunity

Product at a PBT level has margins ~ 18% (this could be different for different manufacturers)

DMCC seems to be backward integrated for a key raw material - Chlorosulphonic acid

Global demand is 60,000 tonnes p.a, growing at 2-3% p.a - DMCC’s mfg capacity would be 10% of the global demand.

Global Manufacturers include - Union Carbide Corporation,USA, Coyne Chemical, USA, Jarchem Industries Inc., USADIETHYL SULPHATE.pdf (88.4 KB)

9 Likes

The company mainly produces Sulphone based chemicals prices of which have gone up from Rs.250 to Rs.600 a kg in the past few months. However the prices needs to be tracked closely if it will continue to remain strong. Most of the chemicals stocks rallied due to china effect however they are slowly resuming business again, so lets see what would be the effect on the chemical prices.

Any views on Borax Morarjee merging into DMCC? Borax is being valued at Rs 22 cr based on the 1:2 merger ratio. DMCC gets a company with break even ebitda and a debt of over Rs 22 cr. The balance sheet of DMCC will only deteriorate.

Though some talk of Borax having a land bank. Maybe someone can provide more details on this. Otherwise, the merger seems negative for DMCC.

Running notes of the recently held con-call of DMCC. There maybe some errors here

20th March 2017

Didn’t make sense in having two chemical company by same promoters

and we see financial benefits else why do this

Borax

- 50yr old co, 1963

*Formed as JV with US Borax and DMCC in 50:50; JV dissolved in late 1970s when India was looking to take MNCs out of the country

- Boron chemicals, borax, boric acid, zinc borate - fire restraint paint

New entity –

Plant of Borax at Dahej and DMCC at Roha

Lot of free land at Dahej, only 10% used of total revenue potential

Land of 100k sqmt, 1/3rd is used

Dahej is chemicals city

Usage of Borax plant –

New plant built over last 2-3 years, Some of the equipment shifted from ambernath but building etc brand new

Products manufacturing – continue to make borax products form borax plant

40-50% of 13Cr P&M is already there and DMCC won’t have to put its money

DMCC plant at Roha – will continue to operate

Costs savings from merger – Admin and other OHs, not quantified yet

Newer product will be made at the plant where there are cost/logistics advantages

Lower interest costs

Way forward for Borax -

#1 brand in India in Boron products (boric acids, borax decahydrate)

Will re-inforce the brand and push more products to existing customer base

Idea is to grow in boron speciality (like in DMCC), there is lot of scope for growth in the market

Will launch new products only if it has a payback of 3 years

Losses –

China slowdown – china is biggest importer of boron and global suppliers started dumping boron chemicals in India

Profitability of borax –

Decahydrate is commodity

Boric acid SQ is speciality

Margins vary from 10%-40%

Indo Borax has better margins –

Unusually low price on boron products which shall reverse

High interest expense for us

No comments on why our RM costs are higher then theirs

Borax RM – all boron imported, no local availability

Negative profits since FY13 – last few years transitioning time, ambernath plant took more time and money than envisaged

Tax benefits of Borax losses – purchase method and hence losses of borax won’t carry forward to DMCC

Pref shares in borax –

9Cr in Borax is held by promoter and will convert it into equity, dividend will be waived

2.8Cr held by employee welfare trust – dividend can’t be waived and conversion can’t happen; will pay dividend and repay loans when company can do that

DMCC maintenance shutdown – likely to be in Q1’18

Sulphuric acid plant shuts down every 15-18 months

Cant set up new SA plant at Dahej

Enhancing storage capacity but effect will be there

Borax turnaround – expect performance to improve next year also and interest cost reduction is key

Expect borax to become breakeven soon

Target to bring margins in line with DMCC

Rajasthan plant at DMCC – SA plant there many years ago, operating as SSP plant in last 15 years until last 1-2 years

No plans to revive and not much financial value

ambernath plant is in the process of being sold

no land with DMCC at ambernath

US is biggest export market followed by EU and China

Borax – price differential vs imports –

Business is done through distributors, several in each state

Approvals are product specific

2 multipurpose plants at Roha and rest are dedicated plants

Capacity utilizations –

With incremental investment of 2-3cr utilization of better margin products can be increased

Current revenue potential of dahej plant – 60-70Cr of revenues without putting any capex, similar to historical revenue numbers

R&D focus area - Micro nutrient, zinc borate, glycol borate

Debt on borax - 18.9Cr is of Borax alone I guess

Capital allocation going forward – in general we will invest in speciality, does not matter which chemistry it is

DMCC – as backward integrated as possible

Technology, quality and cost effectiveness is as good as anybody on the world

Ability to handle these chemicals safely without damaging environment is proven now

Customer appreciate it

55% domestic, 45% exports

Market share – for 3 products we are #1/2/3

Benzene suplhonate chloride 40% global share

Sodium vinyl sulphone

Diethyl sulphate –

These 3 products contribute bulk (~75-80%) of speciality which is 65% of total revenues

Volumes – no comments; in our business tonnage does not matter, if product takes longer to make then realizations will increase

New multipurpose plant – 600-700 tonnes combined this year so far

New launches @ DMCC - global market is few 100 crores and is high margin product, no other player in India

Timeline of merger – 6 months from now

Appointed date – 1 April 2016

Volume in Borax – few thousand tons, as its not very high

boron - 40000/ton

65000/ton – boric acid

Capex needs – new multipurpose plant takes 10Cr but not planned anything as of now

SA is needed for some boron products

7 Likes

I was going through the annual report for FY-2015–2015-16 and found something encouraging in Directors report (Reproduced below):

-

The Company’s speciality chemical business is driven by extensive product R&D and process innovations which are significantly different from those in case of commodity chemical business.

-

With specialisation in chemistry, rather than a particular end use,your co. is attempting to insulate from the business cycles of any one Industry. With specialisation in multiple and multipurpose process and the new products,your Co. IS BETTER INSULATED FROM THE CYCLICAL FLUCTUATIONS IN THE CHEMICAL INDUSTRY.

Concall Transcript: http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/15ecab2d-3f2b-4f74-b51a-93bf45974654.pdf

Notes from the concal [ 22.03.2017]

DMCC

- Founded in 1919; primarily into fertilizer (SSP - Single Sulphur Phosphate)

- heavy losses from adverse impact of govt subsidy on other fertilizers.

- Key raw materials: Sulfuric acid with different organic products - benzene, phenol, ethanol.

- Intermediates : Oleum, Cholorosulphuric Acid, liquid Sulphur Trioxide.

- Produce downstream specialty chemicals.

- Globally DMCC has 3 products with significant market share.Benzene Sulfonyl Choloride (40% global share),sodium vinyl sulfonate(25% global share), diethyl sulfate (20-25% global share). These constitute 80% share of specialty (which is 70% of overall, rest is commodity)

- Diphenyl Sulfone, one of the products Dihydroxydiphenyl Sulfone (DHDPS) can be import substitute - in discussion with customers, no significant traction yet. Globally few hundred crores. No other domestic manufacturing of this product.

- RM Sourcing: Sulphur - by product from oil refineries, Ethanol - locally produced and also imported depending on price.

- Backward integrated upto sulphur; high quality and cost effective production; safe history of producing hazardous chemicals.

- 130 Cr turnover; 55% domestic 45% exports.

- Customer are usually sticky on export side; not many producers. US is biggest market followed by EU and China.

- Plant in Roha, Maharasthra - continue business as usual. New product launches basis RM/logistics/market and other business conditions , either in Roha or Dahej.

- Preference shares outstanding : 2.8 Cr - held by employee welfare trust, dividend at 2.5% needs to be paid.

- Shutdowns once in every 15 to 18 months. Inevitable, but can be better managed by stock build ups etc - likely to be in next quarter.

- New products are taken up basis 3 year payback window.

- No value either from land/plant in Rajasthan. Old SSP manufacturing machinery not of any value. No land in Ambarnath, gone long ago.

Multipurpose plant

- 10 Cr capex last year. Company has done nearly 600 - 700 tons combines which was not there last year.complex process and smaller output is compensated by higher margins.

- approvals are product specific till now. Have 2 multipurpose plants, rest are dedicated.

- Multipurpose is beneficial because of flexibility. Once a particular product reaches sufficient volume - can have dedicated plant of its own.

- For any new products - typical multipurpose plant is about 10 Cr capex.

Borax Morarji

- Set up in 1963; JV between DMCC and US Borax (then BCL); listed somewhere in late 70s majority bough out by DMCC.

- Manufacturing Boron chemicals - borax, boric acid as well as downstream products like - zinc borate (used in fire resistant cables/paints etc), disodium octaborate tetrahydrate(micro nutrient fertilizer, timber preservative), boric acid sq.

- 50 Cr turnover

- Plant in Dahej, Gujarat. Newly built plant over last 2-3 years, common utilities (chilling plant, thermal fluid, effluent water treatment, gas from ONGC) useful when DMCC expand in Dahej. Ballpark benefit 5-6 Cr.

- Focus to grow in specialty boron products. Normal operating range 10-40%

- Losses in past year from supply glut led by decline in Chinese imports; Huge finance cost - looking to reduce; shift from Ambarnath plant proved costly.

- Higher capacity in Dahej plant - ready for next 10 years. May take up some commodity products (technical grade boric acid, additional 2 Cr capex) - improve capacity utilization.

- Potential peak revenues of 60-80 Cr.

- Debt around 17 Cr

- New products in pipeline : Zinc borate, Glycol borates, formulations for specialty micro-nutrient market.

- RM Sourcing: All boron is imported, there is no boron available locally.

- No Tax benefit : Losses from Borax not to be carried forward.

- Preference shares outstanding : 9 Cr - held by promoters, to be converted to equity. dividend will be waived off.

- Ambarnath land is in the process of being sold. Permissions are awaited.

Merger Rationale.

- Reduce fixed overheads. Combine R&D workforce and prioritize new product pipeline in either of Roha/Dahej and either in Sulphur/Boron.

- Boron itself should be able to make money and not a drag on consolidated.

- Reduce finance cost for Borax through pulling DMCC resources

- Appointed date is April 2016 May take about 6 months to complete.

5 Likes

Doc about project expansion: http://environmentclearance.nic.in/writereaddata/FormB/TOR/PFR/16_Feb_2017_10314818072CDWUZXAnnexure-PrefisibilityReport.pdf

3 Likes

A GREAT EMERGING STORY DESTROYED BY A MERGER

-

The key question is that if Borax Morarjee (BM) was not a group company and was available as an acquisition target, would DMCC have acquired it? The answer is a clear NO.

-

BM just about manages to stay afloat on the ebitda level. And this is not new. Check out the last 4-5 years financials of BM. Mostly have been a marginal ebitda loss. So what is so great about BM that makes it attractive for DMCC to acquire it?

-

The recent con call by the management does not point to any great story emerging in boron based specialty products. The key reason given by the management for the merger was more to do with the high cost of debt being availed by BM and spare land available with them. Rest is general talk about wanting to focus on boron based specialty products. What is going to be the return on capital employed of BM in the next 2-3 years?

-

Why should DMCC shareholders bare the burden of financially helping a group company to stand on its feet? BM has total debt of Rs 21 cr (sept 2016 figure) with hardly any free cash flows. If I read correctly from the call notes, the total external liability of the merged entity will be close to Rs 95 cr (debt + current liabilities)

-

The preference shares held by the promoters in BM of about Rs 9 cr are also going to be converted into equity. Though this is not so negative but means further equity dilution.

Net-net, a great emerging story in DMCC has been postponed by another 2-3 years till BM problems are sorted out. The return ratios will fall, no idea of when BM will turn around (forget about giving a 20%-30% ROCE), more liabilities of BM to pay off in the next few years instead of cash flows of DMCC being used to further its own growth (BM any way does not generate any cash to pay off its liabilities).

Another plant shut down of the sulphuric acid plant is coming soon so (though a short term blip) but I feel the stock price of DMCC is not going anywhere till a clearer picture emerges of how DMCC handles the added burden of a ebitda breakeven/loss making BM for the last so many years.

.

6 Likes

95 Crores is not the debt. It is Current liabilities which includes creditors etc. Combined debt should be around 30 Crores max.

I haven’t done a lot of work on Borax Morarji, would spend some time on that in the coming days. I was a bit surprised that they did the deal now given DMCC was just getting its act together.

Another way to look at this merger is that they are getting ~ 100,000 square metres land in Dahej at an EV of 45 Crores with a topline of ~ 80 Crores.

So far, the management has been fair so far in their treatment with minority and also supporting the company through the tough times… One needs to trust them and give them time. What they have been saying in DMCC is coming through as planned. Can they do the same thing in Borax?

Let’s see if the merger is a drag or is perhaps at an inflection point and will help the combined entity. Too early to say I would think. But Let’s do more work

Disc: Invested.

8 Likes

Here is a nice article on understanding boron chemistry -

http://cen.acs.org/articles/94/i30/Boron-chemistry-branches.html

1 Like

Let us try and understand this acquisition transaction from the basics:

If I were to approach you to sell my company with the following financials (other income removed from ebitda), what would you pay for it?:

FY2012 : Sales Rs 77 cr and ebitda of Rs 0.8 cr

FY2013: Sales of Rs 62 cr and ebitda LOSS of Rs 0.4 cr

FY2014 (15 mths): Sales of Rs 66 cr and ebitda LOSS of Rs 7.7 cr

FY2015 (9 mths): Sales of Rs 47 cr and ebitda LOSS of Rs 4.6 cr

FY2016: Sales of Rs 42 cr and ebitda LOSS of Rs 3.2 cr

FY2017 (9 mths): Sales of Rs 40 cr and ebitda LOSS of 0.3 cr

There is an improvement taking place in the business but it is still an ebitda loss company.

Let us look at the liabilities in BM:

-

Total debt of Rs 24 cr

-

Payables are going up despite stagnant sales:

a. Rs 12 cr in FY14, Rs 21 cr in FY15, Rs 21 cr in FY16 and Rs 26 cr as on Sept 2016.

b. Which basically means you are not paying your r/m suppliers on time and any new buyer will have to clean up payables to a reasonable level to do business. I feel there is excess payments to suppliers of about Rs 15 cr which will need to paid immediately by a new buyer.

c. Just to give you a perspective, Indo Borax with sales of Rs 73 cr has payables of Rs 4 cr (compared to Rs 26 cr of payables for BM on sales of Rs 41 cr).

So total liabilities are around Rs 39 cr.

Typically, chemical companies of this type should trade at a valuation of about 6x-7x ebitda. Indo Borax trades at 7x.

You would not pay an enterprise value (EV) of more than Rs 15 cr for this loss making business (giving it the benefit of doubt of a Rs 2 cr ebitda positive business already). There is some spare land and utilities so add another Rs 5 cr. So max EV of Rs 20 cr.

And guess how much has DMCC paid for BM? A total of Rs 62 cr (equity of DMCC shares worth Rs 22.6 cr and taking on liabilities of Rs 39 cr).

Indo Borax, a competitor, had sales in FY2016 of Rs 73 cr and an ebitda of Rs 12 cr. Nil debt. Has net cash during the year which earns Rs 2 cr + interest (is sitting on Rs 17 cr of investments as on Sept –2016 which it moves to inventory and back to cash during the year). Available at a valuation of Rs 88 cr (7x ebitda).

Simply put, this was just a bail out of BM by the promoters. Just does not make economic sense to buy such a business at these valuations. Unfortunately, DMCC investors will have to suffer.

5 Likes

Does any one have an idea of what is the market value of Borax Morarji’s land in Badlapur that the Co. is looking to sell?

1 Like

Great reply. Such counter views are very much necessary for a healthy discussion.

The way I see it and the management emphasizes in the conference call - that Borax business is sustainable on its own - just that they need to be helped at this critical juncture. Given that the business is very close to breaking even at the EBITDA level in the recent quarters

There are some small initiatives, like the technical grade boric acid production, which can be facilitated at additional 2 Cr capex and lead to improved capacity utilization, but Borax in its present form cannot undertake those. Given the brand still commands a name among the consumers, speaks of the quality.

The fact that management is willing to sacrifice the dividend payout on the preference shares and extend interest free loans to meet long term funding, speaks of their commitment. It would be only fair to give them a chance at this juncture.

Also from the point of environmental clearance and everything, setting up a new greenfield plant in Dahej would have set back DMCC by 2-3 years. This set up clearly provides a much faster way out with all utilities being already up and running.

If we go back to an earlier healthy base period FY05-09, this business was earning a healthy EBITDA of 10-12%. Even discounting the commodity bull market of that period, one can assign a 5-7 Cr EBITDA which at 7x yields close to 50 Cr EV. Add the proceeds from land sale and utilities - the 62 Cr purchase price is not that expensive.

Another key point is the renegotiation on the 17 Cr short term debt. Borax is paying very high interest here and can benefit largely from merging with DMCC.

a) Cash Credit facility from Consortium Bankers is secured by first charge over stock in trade, stores and book debts of the company. Further it is secured by way of second charge against mortgage of the land at Dahej, Gujarat. The Cash credit is repayable on demand and carries interest in the range of 15.50% to 16.45%,

b) Corporate loan from HDFC Ltd. is repayable on demand and carries interest @ 14.65% per annum. Repayment is in one installment falling due on 31st July 2016.

A lot will depend on how quickly the merger happens and integration benefits are passed on.

4 Likes

Folks following Borax kindly comment on this:

The Annual Report of Borax Morarji for 2016, has the following observations :

[Page 8/84]

Land at Ambarnath

As approved by the Shareholders and informed earlier, the Company has sold its land at Ambarnath and the necessary provisions/adjustments have been made in the books of accounts arising out of the said sale.

[Page 52/84]

Income

Profit on Sale of Land at Ambarnath 2,161.52 Lacs

Footnote on same page

Profit on sale of land at Ambarnath is pursuant to agreement to sale entered with a Party. The Company is in the process of registering the agreement and has received substantial portion of the sale consideration and also obtained necessary permission/approval in the terms of the said agreement.

What sale proceeds are we then talking about when the management mentions that land sale in Ambarnath is awaited ?

3 Likes

- Saint like charity made by the promoters by waiving off outstanding dividend on preference shares

Most investors seem to be mesmerized by the act of the promoters to waive off the accumulated outstanding dividend on the preference shares held by them. Why don’t we do some number crunching.

a) DMCC Preference shares:

a. 6 lakhs pref shares at 8%: Accumulated overdue dividend outstanding as on March 31, 2016 is Rs 6.24 cr. Add another Rs 0.36 cr till Dec 2016. Total is Rs 6.6 cr (waived by promoters)

b. 2.8 lakh pref shares at 2.5%: Accumulated overdue dividend outstanding of Rs 0.57 cr as on March 31, 2016; dividend cannot be waived as they are owned by employee trust (not waived)

b) BM Preference shares

a. 90 lakh pref shares at 8%: Accumulated overdue dividend outstanding as on March 31, 2016 is Rs 1.27 cr. Add another 0.72 cr till March 31, 2017. Total is Rs 2 cr (waived by promoters)

So the promoters are waiving off around Rs 8.6 cr of accumulated dividend on outstanding preference shares held by them. Wow. Such generosity. Only a true saint can perform such an act.

- How do they react when a seller comes to them to sell his company

The owners of BM come to meet the owners of DMCC and offer their company which has the following fundamentals:

a) Sales of Rs 42 cr

b) Making ebitda loss for last 4 ½ years

c) Commodity business

d) Outstanding debt of Rs 24 cr (bank debt at around 15% interest)

e) Outstanding supplier payments of Rs 26 cr

f) Net worth of Rs 2.55 cr

This is clearly a struggling business which is not generating any cash and with no ability to meet its outstanding liabilities. The business is on the verge of closing down until some help comes their way. No problems. DMCC will value this lousy business at Rs 62 cr. They ignore that another borax business with sales of Rs 73, ebitda of Rs 12 cr, pat of Rs 9 cr, nil debt, outstanding supplier payments of only Rs 4 cr is quoted on the stock market at a valuation of Rs 88.

Sorry, I just forgot to tell you that owners of DMCC are also the owners of BM. Apart from DMCC taking on the huge liabilities, owners of BM are also being given shares of DMCC worth Rs 22 cr (of this, Rs 14 cr will go to the existing owners of DMCC since they own 63.5% of BM).

The picture now becomes clear. The sacrifice of Rs 8.6 cr was worth every crore. The promoter clearly spells out on page 13 (last para) in the recent investor con call, ‘nobody does this for charity’ when he talks of waiver of pref share dividend. Of course, he meant it in terms of the long term outlook of the combined business but I see a hard-nosed businessman who has got more by sacrificing a bit. And mesmerized the investor community who seem to be going ga-ga over his sacrifice.

Oh, and just to complete the story, post-merger, the promoter holding will increase from 50.22% to 53%. It did make sense to value the lousy business at such lofty valuation since promoters own 50% of DMCC and 63.5% of BM.

8 Likes