I too agree with your views , it seems there is lot of panic created due to rumors ( I hope its that only ) being spread through WhatsApp messages etc. and may be trader shorting it in big way.

My thoughts of Dhfl and other NBFC .

Past five years-

Decreasing interest rates which was favorable.

good growth in loan book.

NBFC went into Risky asset class like LAP and so on to grow book.

Till Sep 21–

one of the very few sectors growing above 20%

Psu banks had huge prob and market was bullish on Nbfc and private banks as they will take market share from the PSU banks which had 70% market share in lending.

ON SEP 21- IL&FS needle bust the overvalued market which was bound to happen anyway even without IL&FS.

“NBFC” is in the eye of the storm as IL&FS was under NBFC sector. market painted all NBFC under the same paint.

Then the ALM miss match.

Then increasing interest rate in future is taken into consideration.

Then LAP,RE assets become very very risky.

Then market’s worry of who will lend to the NBFC in future since “all NBFC can default”

Unlike 2011 -2014 interest rate up cycle where stocks (finance) fell slowly, we are seeing a knee breaking reaction. since market is looking into the future as always.

PNB housing has raised 1400cr through ECB .PEL has raised 7000 cr (5000CR for fin) in the recent past and yet market is punishing them too.

Now the thought is RE sector cannot sell homes and everything will become default.

Same thing happened during NOV 2016 demon days. that panic went on till feb 2017.

Future-

Due to interest rate up cycle and some recent problems, NBFC sector will grow slower,this the companies also accepted.

PE -P/BV of companies adjusting to the future lower growth rate.

The market is reacting like the Frog in hot water.If this has happened in a slower manner we wont know the heat.

I might be totally wrong in my thoughts.

Invested in Dewan,Pnb housing,Gruh,Pel and Bajaj fin.

4 Likes

Would appreciate if you can share anything specific substantial on

"they have distributed loans like cakes to borrowers which are not capable to pay "

since as of now there is no evidence that shows sign of this in terms of NPA etc.

3 Likes

Mainstream media scaremongering in bearish times and going gaga in in bullish times is not surprising. Happens in every cycle. Not saying all is fine or not at DHFL, but we definitely need to take media opinions with a bag of salt, to say the least.

DHFL has successfully issued masala bonds in the past.

My reading:At most, DHFL could see short term margin compression. Defaults unlikely, given that nearly 80% of business is to retail (also a reason for the lower margins/return ratios many have mentioned in earlier comments). Also, since most of their lending is in the ‘Affordable housing’ category, i see them as beneficiaries of the securitization trend, as and when that channel gathers steam (for banks to fulfill their Priority sector lending requirements).

Given that mortgage to GDP ratio in India is still at ~10%, it’s important not to forget the longer term picture. As long as the management can deliver on thier NIM commentary over the longer term (check that over last few years), the stock should make a comfortable recovery in my opinion.

Disc: Invested; Added marginally on this dip.

1 Like

2 Likes

The biggest worry is that the IL&FS fiasco may force the RBI to regulate NBFCs as stringently as the banks. Definitely, It has got to do more with the liquidity and not with solvency, as rightly mentioned by a few members that the branches have reduced/slowed the disbursement process. more controls from RBI would mean stricter capital adequacy, NPA provisioning etc. If anything happens in that direction, it would revalue the whole industry.Perhaps thats the fear that is being priced in across.

The cost of capital for NBFCs is usually 2-3 percentage points higher than that for banks, but these firms can leverage up to eight times on their equity. NBFCs typically leverage five-six times.

members, do share your views.

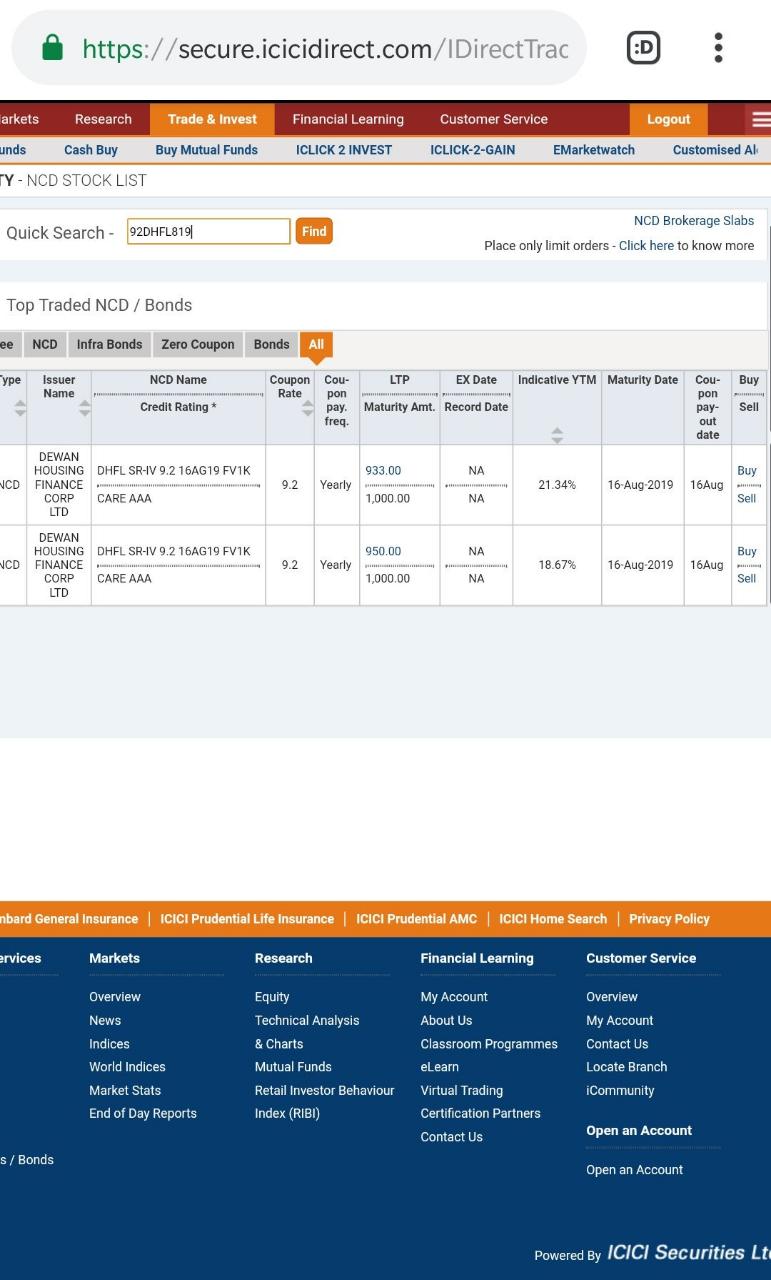

I was forwarded this image today by a bond trader friend, just wanted to know if anyone tracks this, since the YTM on this short term NCD is around 19%! Seems too good to be true! It’s AAA rated too!

To be fair, he did say liquidity is low, but a retail investor can still buy in decent quantities, he said.

Would appreciate if anyone can either confirm or debunk these prices.

If debunked, will delete the post immediately. Thanks in advance!

Disc: not invested currently, but very much interested after the fall (both in equity & debt)

LTP is 933, maturity is 1000. Maturity date is Aug-19. YTM seems to be close to 9%. I guess the ICICI direct platform has bugs and your trader friend doesn’t know.

1 Like

Anyone know what is the current yield on 1/3/6/9 month instruments of DHFL compared to other AAA instruments?

There is coupon (interest) due on maturity and principal due of 1000 which is selling for 933 now. So 159 (67+92 ) due on maturity along principal of 1000 ~15.9% on absolute basis and more on annualized basis. So the numbers are very close to what is shown.

2 Likes

Any other papers quoting at a similar yield? This is an NCD which is of relatively longer duration. Anyone know of any CP yields?

@dineshssairam - this is what I was referring to in your post. For now lets forget about a default. How will they raise capital to grow if this is how the market will price their NCDs/CP’s? Would one assume that until the yields come back to where a AAA yield should be, DHFL will severely limit lending (as a result of which their gearing will keep coming down) and as soon as money market is normalized they have the ability to lever back up and again for a short period possibly grow at even 30/40/50% to make up for this loss until their gearing comes back to current levels?

YTM will be higher since expiry is in 10 months. The volume on these appear quite low so how reliable are these? Can anyone comment

Forget 17-20%, I think I found a winner:

We should liquidate all our assets and invest in Muthoot Finance NCD ![]()

1 Like

Is that a bug or am I missing something in calculation? I calculated yield as (1704-1450)÷17.04 ~ 15%

That’s for ~4 months. Annualized YTM would be around number shown.

1 Like

How can coupon be 0%?

As a non-sarcastic answer, CP trading data is found here: https://www.nseindia.com/products/content/debt/corp_bonds/cbm_sett_data_archives.htm

A CP issued by DHFL was traded at a 8.98% Yield on 28-Sep-2018. There’s one more settled on 19-Oct-2017 at 7.10%, but that’s not helpful for us because it was settled on the Maturity Date itself.

There is a pressure on all NBFCs to manage liquidity. We shall hope that the management sees this through, with a helping hand from the regulators.

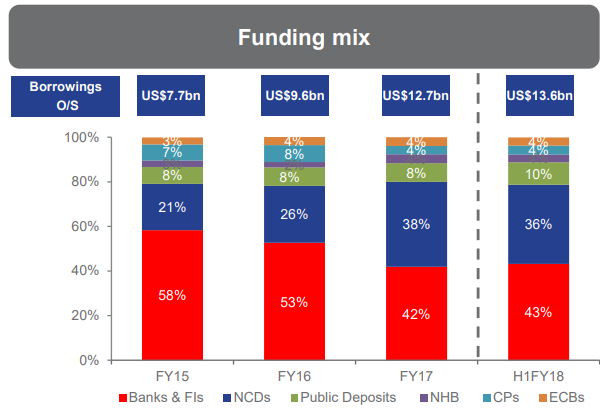

At this juncture, let’s not forget the funding mix of DHFL:

3 Likes

So what I gather from the responses is that in some thinly traded markets, if you are lucky, you can buy really cheap debt in decent quantities (not in crores, but in lakhs, as per my friend, who is actively buying). In all probability, this is only possible for those companies which are (rightly or wrongly) negatively perceived currently. For someone like Muthoot Finance, I am still inclined to believe there is some error, or just a freak transaction, possibly colluded by both buyer & seller.

Just for the record, he is also buying IHFL, SREI Infra, etc debt at obscenely cheap prices. Have some screenshots of those as well, but not posting without his permission.

For us at Valuepickr, those who are interested in buying equity (including me) in some of these names may check out if buying debt could be a better risk adjusted option. Also, I think this might a temporary dislocation in the debt markets, and things should get more rational soon. That’s my opinion, to each their own, of course!