Not expecting a huge upside even if profits reach Rs 200cr. Find the HDFC Sec target of Rs 190-200 realistic. What is the PE that a company like this should get? Current market cap is Rs 1361cr. So about 46% return if share reaches a PE of 10 with profit of 200cr.

Higher reliance on trading activity leading to a deterioration in the financial profile marked by decline in profitability margins

Increased debt levels (being debt focused, the agency has also taken into account debt funded capex pertaining to capacity augmentation of Bentonite Sulphur (BENSULF) and NPK fertilizers)

Continued reliance on natural gas at market rate vis-à-vis administered price mechanism (APM) rates

Likely recovery of differential pricing on account of domestic natural gas at APM vis-à-vis natural gas at spot prices further to the circulars issued by the government

Fertilizer stocks including Deepak have taken a hit today as Government officials say that fertilizer subsidy arrears of Rs 40,000 crore are not likely to be paid this fiscal

I saw the prices of all these fertiliser stocks and I see that they are hardly 1 to 2 % down or flat.

If stocks go down 1 to 2% and people come out with statements that they have taken a hit then it seems the whole market has been taking a hit since a long time.

I think the key remains to maintain a balance and keep away from all these kind of sensational news designed to grab eyeballs rather than providing any useful information.

These days the problem is of excessive information overdose. (and most of this info is irrelevant or useless)

I take your point

Was looking at the reason for fall in RCF and Chambal, and the news flashed on CNBC. They even interviewed Zuari Agro management on this Lets see if the news is posted on their website

In any case, I take that as an opportunity to buy more of Deepak. In my opinion, the company is not so adversely affected even if the arrears are delayed. The risk of losing the upside on gas availability is higher. What I am concerned about though is the fall in commodity prices, which might delay an uptick in mining activity (negative for ammonium nitrate).

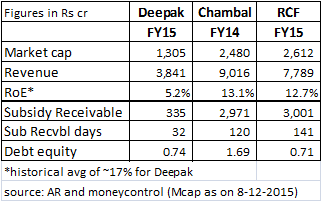

Deepak Fertilizers had Rs 334.98 crore of subsidy receivables due as on March 2015 (Page 127 of 2015 AR). Compared to this, revenue for the year stood at Rs 3841 crore (Page 111). The company therefore seems to be relatively better placed in terms of subsidy dues.

This is the link where moneycontrol says that “news are doing rounds” about delay in payment of arrears from the government this year:

The whole fertiliser sector is buoyed by growth figures flashing on cnbc about the sector showing growth. I just managed to see the anchor lata venkatesh mention something about growth in fertiliser sector.

Another company which would be benefitted with this agreement between rasgas and pet lng would be torrent power. Both companies have entered into a 20 year supply agreement and regular availability of gas would provide good growth visibility to torrent power’s gas based plants.

disc: invested in both deepak fert and torrent power.

Thanks Hiteshji! Purchased some torrent power. Gas prices have almost halved because of this decision. Any idea about the quantum of benefit accruing to Torrent Power?

The CEO of Petronet LNG has also claimed that the lowering of gas prices by RasGas would save Rs 10000 crore in fertilizer subsidy over a period of three years. Though not directly, but would that benefit fertilizer companies heavily dependent on subsidy?

The note says that “chemicals manufactured by integrated fertiliser-chemicals complexes may also witness improvement in profitability as cost of production will decrease while their prices are generally driven by international prices”. Deepak has been explicitly mentioned as a beneficiary in this note apart from GSFC, Guj Narmada and RCF

Major impact as per the note would be on subsidy receivables and lower working capital (and therefore, lower interest burden). However, Deepak is not significantly exposed to this, nor is it a urea player.

Does anybody know why the Government is not providing gas to Deepak despite the HC order? As per a friend of mine who covers the sector, the government is penalising Deepak for using gas to manufacture chemicals instead of urea.

Deepak Fertilisers & Petrochemicals Corporation, India’s leading producers of industrial chemicals and fertilisers, reported standalone net profit of Rs. 23.47 crore registering nearly nineteen folds jump yoy but decline of 11.13% qoq. The company’s revenue stood at Rs. 1,051.32 crore, witnessing growth of 28.45% yoy and marginal increase of 0.27% qoq.

It’s core operating profit of Rs. 86.88 crore increased by 70.45% yoy but declined by 6.94% qoq. Operating margin at 8.26% expanded by 203 bps yoy but contracted 64 bps qoq.

For nine months ended December 31, 2015, the company’s net profit stood at Rs. 95.21 crore increasing by 86.25% yoy. It’s revenue stood at Rs. 3171.97 crore clocking growth of 14.07% yoy.

Standalone EPS for the quarter stood at Rs. 2.66.

Management Comments:

Mr Sailesh C Mehta, Chairman & Managing Director - DFPCL, said: “As compared to previous few quarters, performance in this quarter has shown some positive signals. This quarter witnessed Acids and TAN recording very good volumes and the Company will now take on the next growth phase with expectations of better performance and enhanced market leadership. We continue to remain optimistic about the resumption of supply of natural gas and are hopeful that the matter will soon be resolved.”

@hitesh2710 Hi Hitesh, do you think it is a good time to accumulate Deepak Fertilizers?

There are three things that I believe are in the company’s favour:

Chances of a pro agriculture budget

Dividend yield, which can get better as I feel DPS might inch up to Rs 5.50 again (looking at dividend only from a Graham’s point of view, being around half of AAA yield). While the likes of NMDC and Tata Steel also have high dividend yields, only in the case of Deepak is it sustainable. Refer Graham’s last will and testament to find the attractiveness of Deepak on various parameters including P/BV http://www.stockopedia.com/content/benjamin-grahams-last-will-10-useful-rules-for-stock-selection-64001/

Recent numbers that indicated a turnaround in operations (gas issue resolution being an additional trigger). I am negative about traded goods sales though

The problem of gas plaguing the company is on the verge of being resolved. But the fortunes of the company depend partially on the state of monsoon and how fertiliser sales pan out. For me its very difficult to predict the earnings of these companies and hence allocation cannot be high.

div yield should offer some downside protection. But with market correction affecting even quality stocks there could be better choices.

Very good news for the company . That will bring down their net debt to very low levels . Surprised why the stock is up only 5%

Deepak Fertilisers & Petrochemicals Corporation Ltd has informed BSE that the Department of Fertilizers (DoF), Ministry of Chemicals and Fertilizers, has been withholding subsidy claims due to the Company in accordance with applicable Nutrient Based Subsidy [NBS] Scheme of the Government of India, since June, 2014 amounting to Rs. 795 crores as on March 31, 2016. The Company had since challenged the said withholding before Hon’ble Bombay High Court and the Department has now informed commencing the release of all subsidy arrears except an amount of Rs. 310.52 crores in the interim. This part withholding is already under Hon’ble Court’s purview for final award.

Lets see if the news is posted on their website

Lets see if the news is posted on their website