DE NORA India is a niche zero debt, small cap MNC, with a tiny equity capital of ₹ 5 crore of which 54 % is held by the parent oronzio De Nora of Netherlands

. This firm has 3 divisions 1) electrode technologies 2) water technologies 3) Anti corrosion systems.

This 30 year old company was in corporated in technical & financial collaboration with De Nora group, by erstwhile MD & their families of Alfa Laval India & Hoganas India, mainly to cater to re coating of electrodes & replacement of damaged electrodes in chlor alkali industry in india, which required re coating of electrodes every 2 years, in the then mercury cell process. In the past 10 years, the entire chlor alkali industry in india has migrated to energy efficient membrane cell process, which requires recoating every 6 to 8 years, which implies that Denora India will have work only for 2 years & will have to sit idle for the next 6 years.

. That’s exactly what has happened, & Denora India has mastered the art of hibernation, with annuity model income from AMC as well as interest income from fixed deposits of ₹40 crore. However the major obstacle was the prolonged tussle with the Indian promoter Devika Khanna family for the past 8 years, as a result, the parent refused to supply technology & support. Ultimately with the threat of cutting oxygen supply to the Indian subsidiary ( it was done) the Indian promoter was declassified from promoter quota & they sold their shares on the bourses in late 2017 at ₹250 levels, which was fully absorbed.

Now, this, is is the reason, why returns on all parameters, for Denora India has been poor, for the past 10 years. Now the parent has taken full control & its anticipated that with the support & control of the parent, technology will flow, as also the Indian subsidiary will be able to seamlessly import, knocked down kits, components & spares on credit from Denora subsidiaries worldwide. (This was not possible earlier). Now on the bourses, with cyclical quarterly spurts in profits, it has surged to life time high of ₹560 in 2016 & ₹633 in 2018, & now corrected to ₹230 levels, in the aftermath of small cap carnage.

With nil holding by mutual funds, 54 % is held by the parent, 20 % by HNI & NRI investor groups. No analyst has ever given coverage on Denora India, except for sp Tulsian in 2016. With low floating stock & equity capital, it’s easily manipulated by operators, in trend with volatility in quarterly profits.

Now coming to the 3 divisions, 1) Electrode technologies, worldwide Denora has electrodes repair & electrode manufacturing in the same plant for synergy, but in india major role is for re coating, while manufacturing of electrodes is limited to chlor alkali industry, however presently exports of electrodes pertaining to chlor alkali industry is being undertaken, as cost of manufacturing in USA plant is high. Worldwide, Denora manufacturers electrodes for all applications, including those used in fuel cells for industrial & electrical vehicles in joint venture with AFC energy plc. So in india, we can expect manufacturing of electrodes for all applications, in future, as its only plant in Goa has land bank, for future expansion.

-

water technologies. Denora India manufacturers standard as well as those catering to client specifications, All types of electro chlorinators for water purification for drinking water in railways, townships, residential flats, hotels, industries, swimming pools water theme parks etc. Electro chlorination is the most convenient & cost effective process for commercial water purification. After parent, taking full control, De Nora India bagged tender for industrial electro chlorinators from Bhel in Tamil Nadu for ₹12 crore. Now industrial electro chlorinators are a must in coal, power, steel, nuclear, oil & gas, & all industries that use sea water. Typically Desalination is done, followed by electro chlorination,which kills microscopic algae in sea water, which otherwise grow & occlude equipments & machinery, resulting in sudden shut downs & extensive repairs. Now these projects typically have a gestation of 12 to 18 months, after approval of drawings, for installation & trial runs. The Bhel order is now in the last phase of execution & Denora India typically plans to bag 2 to 3 tenders for industrial electro chlorinators every year & steadily grow in the segment. Now these industrial electro chlorinators are imported in knocked down version from Denora subsidiaries in Singapore or China & assembled & installed in india, along with AMC, spares, maintenance & after sales services. I don’t think these industrial electro chlorinators will ever be manufactured in india, as dedicated plants in China & Singapore do the same thing. However because of imports, forex & dollar rupee comes into play. Further the company caters to entire spectrum of waste water treatment plants for industrial waste, Municipal waste, river purification etc, These kits & components & spares, are again imported from Singapore & China.

-

Anti corrosion systems are used in steel, construction, marine, ships, industrial etc for prolonging life & durability. Further immense potential as, anti corrosion coatings are used in oil & gas pipe lines for prolonging life, as also railway tracks & structures, bridges etc.

Risk factors. The management is trustworthy, with integrity & unalloyed passion to electrochemistry. However the parent & all its subsidiaries in Italy, Europe, Netherlands, Japan, Canada, USA, Singapore, China are privately owned & not listed on the bourses. The only exception is the Indian subsidiary. Therfore its difficult to get info on Denora India from the management, also no quarterly concall, only limited material is revealed in AR & AGM. With parent in full control & immense potential for its products in india & neighborhood nations, Denora India is a potential multi bagger, if all goes well. Even delisting cannot be ruled out at a future date, as the Indian subsidiary is the sole listed subsidiary in the world. Being a small cap, No mutual fund holdings. Share is also volatile, with volumes from less than a thousand to 3.5 lakh per day on strong cyclical quarter results. With focus on all 3 divisions, volatility in profits should iron out. However all depends on the intentions & will of the parent to focus on the growth of its only listed subsidiary.

I would request one & all especially, Rohit Balakrishnan & sri Krishna bhutra to provide perspectives.

As of last year, electrode technologies contributed 78 %, water technologies 1% & anti corrosion systems 20 % to the turnover. With parent, in full control, all 3 divisions are expected to grow, substantially, & volatility in profits or cyclical nature of business & profits are expected to be ironed out.

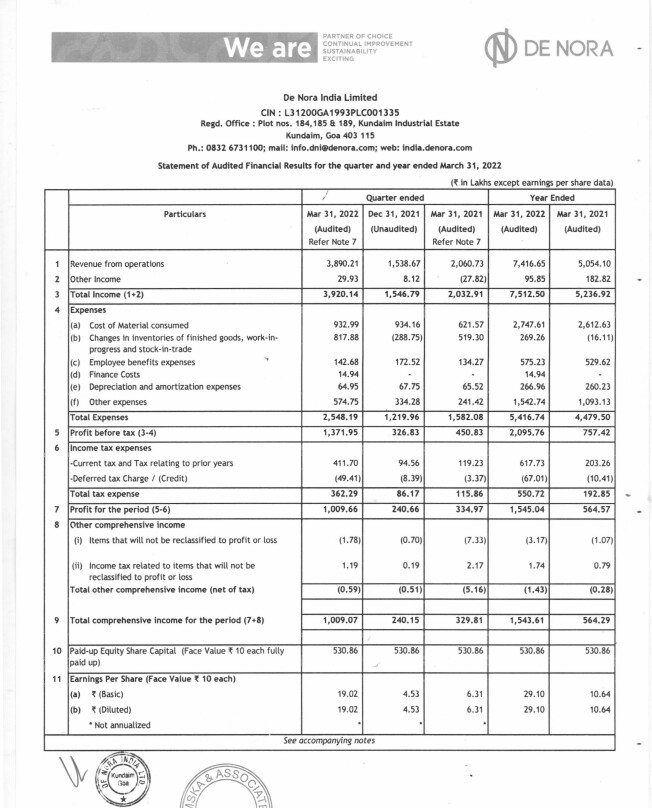

On the financials, December quarter, 2017 was the best, with net sales of ₹13.42 cr & EPS of ₹ 8.54, due to surge in re coating orders for electrodes. In March 18, Q, Net sales dipped to ₹ 5.02 cr, with loss, in the Q with negative EPS of ₹3.30. This is due to dip in recoating orders, showing cyclical nature & also, since re coating of electrodes is the major, contributor to revenues with 79 %, This share corrected from ₹633 levels to ₹220 levels. Now with the parent, focusing on ramping the other 2 divisions, volatility should iron out in future.

For June 18 Q, on a net sales of ₹9.13 cr, EPS was ₹3.58, while for Sept 18 Q, Net sales were ₹ 7.86 cr, with EPS of ₹ 0.95. Company has been regularly paying dividends for past several years , with 10 % for the last fiscal.

Discl Holding for the long haul.