here is the detail on menstural cups. the raw materials and customer base is likely to be the same as male/female condoms. It will complement the sale of female condoms while increasing ROCE and sales.

Cupid just declared results. Both topline and bottomline are down by 50pct. Also, 9mth results for current year are trailing previous years 9mth results.

Cupid seems to be facing serious issues with capturing govt, institutional and retail orders.

Considering govt tender based business, it is expected to have lumpy sales on Q on Q basis. However, we need to evaluate full year performance.

The “poor” results are clearly due to the “drop” in Sales. Margins have held up (Which we should expect anyway). The reason provided is that two large orders had some sort of shipping delay, and hence moved to Q4.

If I’m reading this right, it’s an accounting adjustment. As pointed out by @hnk_so, we should wait for Q4 before judging the overall business (I expect at least a 10% increase in Top line). Meanwhile, we can always look forward to the Concall for more details.

The notes mentions that the impact of the accounting adjustments is not material. The numbers are clearly due to postponement of customer deliveries and that reflects in the inventory adjustment…

Given that almost no institution holds shares, the downside is limited…even the promoter won’t logically sell stake at this stage

Good to know you are still holding… seems like a tough phase after dream run in financial performance (both top and bottomline) until FY18

@dineshssairam Admire your ability to deal with and fairly value/quantify uncertainty. As per screener, the Graham Price of Cupid apparently should be 121.19 (not sure if its updated based on Q3). For a company like Cupid known for a lumpy growth pattern, is this a good reference point to use to enter/exit from an investors standpoint? Also, can we assume Graham Price as a good entry point to add more should someone be interested?

Dis: Invested

A 50 pct hit due to delayed deliveries is a big deal especially when we are waiting for growth.

They also lost a case against a govt medical agency. A new CEO is still not found. Problems are increasing for Cupid. However, all is not lost and it remains to be seen how Mr. Garg steers the boat.

Any company in this world faces challenges and the first rule in life and business is that things are never linear.

Your points are valid. The comfort is the order book.

The greatest challenge in microcaps is the mortality rate. A good management deserves a higher valuation regardless of growth in my opinion. LEEL and Prabhat are examples before us.

Incase the numbers they publish are true and the balance sheet and ROE are healthy, the price fall is not a concern.

2 Likes

It’s not a “hit”. It’s a delayed order and has been added to the inventory. The note says it will be added back to Q4 Sales, which remains to be seen. In an order based business, it makes no sense to compare QoQ numbers. Only YoY performance and management guidance helps.

The problem about succession is most certainly there. If Mr. Garg manages to appoint someone with a good Sales/Marketing background as the new CEO (As he’s been wanting to for so long now), it will be a big boost. Mr. Garg is too conservative and even recently made a comment about how he’s unwilling to spend on B2C advertisement in India. For Cupid to scale, this needs to change. Cupid needs someone who can steer the marketing activities, as well as a decent capital allocator.

Graham Price is usually a very pessimistic estimate of value. So, yes, I’d say that’s a good starting point if you want a massive Margin of Safety in the stock.

As per this, balance revenue to be booked in Q4 should be atleast Rs.40 Cr. Add to this, Tanzanian order of Rs.16 crs which was received just after the concall.

If delay in shipment is the only reason then Q4 topline should be Rs.56-57 Cr. atleast. We need to confirm this on concall that there is no material change in other pending orders that company had as on last concall.

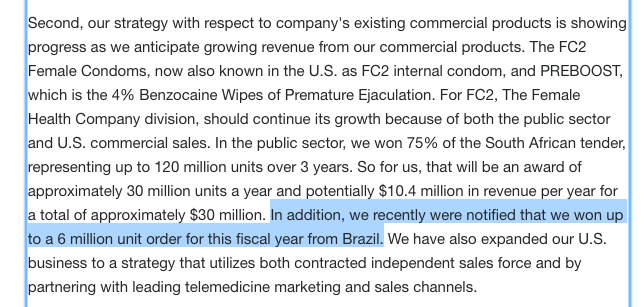

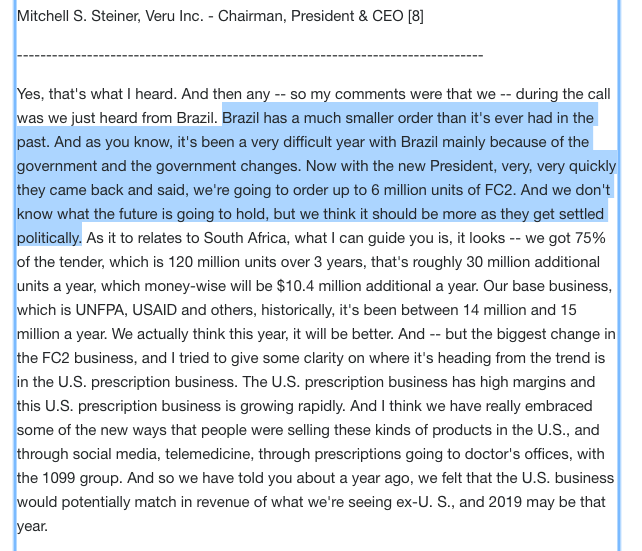

Veru has won order for 6 million pcs from Brazil tender. From the comment it looks like govt just came up with 6 mn pcs right now instead of 30 million. If that is true then Cupid unfortunately couldn’t win this one.

Here is an update from Veru’s latest concall. (https://finance.yahoo.com/news/edited-transcript-fhco-earnings-conference-184940456.html)

2 Likes

My concern is relating to the reasons which led to such a huge qty being pushed to q4? Inventory and planning be put aside, any variation over 20-25%will make me uncomfortable as an investors, qoq and yoy performance not withstanding.

Looks like Cupid didn’t win the Brazil order I guess. Tough times I guess, lets see what Mr Garg has to say.

List of questions for upcoming concall:

-

Progress on expansion. First line was to be commissioned by Dec. and another by March. Are we on track? How much have we added by Dec.?

-

Are we on track to achieve 56-57 Cr. turnover for Q4FY19?

-

Below 3 are inter-related

- Product mix

- Capacity Utilisaition

- Finished Goods Inventory as on 31st Dec. 2018

Based on the inputs provided by the management, we will be able to know the real issue in Q3. If the shipment is delayed and goods are produced then it will be reflected in inventory. Inventory as on Sep. 2018 was 7.59 Cr. (Last 3 years FY18, FY17 and FY16 - FG proportion to total inventory is 56%, 44% and 57%)

If inventory level is low or same as Sep. 2018 then capacity utilisation should be under 50%. Last quarter it was 90%.

If both these are approx. same as last quarter then product mix and realisations would have dropped drastically which is unlikely.

-

Whether final notification received from USFDA and progress on discussions with marketing company in California. Are we still hopeful of generating revenue from Q1FY20?

-

Progress on new products - 1. Wipes and 2. Second generation FC.

-

Updates on Brazil order. FHC has won 6 mn pcs. What about balance qty? It was mentioned that single company will likely win the order so is Cupid out of race now?

Other members, please add your relevant questions so that we don’t miss out on anything.

3 Likes

You forgot the mandatory question about the new CEO. But I guess someone is bound to ask that anyway.

2 Likes

i have a more fundamental question -

- Management keep talking about revenues of 200 cr in a couple of years time but the recent news has been exactly the opposite i.e. lower volumes in SA, JV project in SA shelved and now a much smaller project, nothing on the Brazil front, domestic brand building shelved as too expensive and take up quite slow.

Only positive has been on the male condom side which is such a low margin commoditised segment.

Where does the promoter go from here - is this a reflection of Cupid’s inability to compete with FHC? Is this going to be mainly a male condom company with minor amounts of female condom here and there.

Regarding US entry, how does Cupid compete with FHC in their local market. FHC have more muscle power and greater size and we have already lost the Brazil and SA tender to them this year. So why should we be positive about the US entry.

I think Garg is a nice guy but we need to shake things up and start asking some hard questions as news flow of late hasn’t been good.

1 Like

Surprised that people are looking for 50 crores as Q4 turnover assuming that unshipped Q3 sales will catch up. I don’t think it’s fair either to judge the company based on orders that the company didn’t get; the addressable opportunity is huge. Yes however tough questions need to be asked.

I feel that the promoter should put up the company for acquisition so that the potential can be monetized effectively.

It is understandable that company is expanding sexual health and wellness range, but looking to the competition, I would say they should add products using same raw materials of silicone and latex.

- Baby bottle nipples and

2 Menstural cups,

Baby products are high margin and Menstural cups are a volume product.

The target markets will still be SA, Brazil and rural India and bring complementary sales volume and economies of scale. This will also make the company a sort of FMCG brand with a vision of social awareness.

I wonder why other boarders are not enthused about asking the management such questions during the investor Concall rather than stick to Brazil order or SA order inquiries which only pertain to a quarter or two…

1 Like