I remember they discuss this point during last call…

getting us FDA approval cost them 15 Cr to 20 Cr but iam not sure about the timing…

1 Like

Approx 18 months, 15-20 cr cost. Details r available in various concall transcripts

Any one please share the market size of female condom in USA?

Once cupid got the FDA approval then how much revenue it will get approximately?

Excellent Question.

I suggest that you read the books One Up On Wall Street (from Peter Lynch) and The Five Rules for Successful Stock Investing (from Pat Dorsey) keeping Cupid as an example in order to get an answer.

It would be laborious and too slow but worth doing as you would be awarded the scroll that can be applied to get answers for any company.

On a lighter note, experts say that never buy a share in month of October. Other months to be avoided are the rest eleven.

Intention of this note is to set you on the right course…Cheers.

8 Likes

Female Condom Update: IXu Asks Why FDA Dragging Feet, Senator Stabenow Inquires; Cupid Ltd. Offers for Patents

Check the above out -apparently they have been waiting for three years for approval.

IXu also announces it will conclude transactions for its female condom patents by November. Cupid Ltd. of India, which produces a knock-off of the VA w.o.w, submitted an offer for the IXu next-gen electronic female condom patents (VA Vibe) and indicated Cupid can contract-manufacture condoms for IXu.

2 Likes

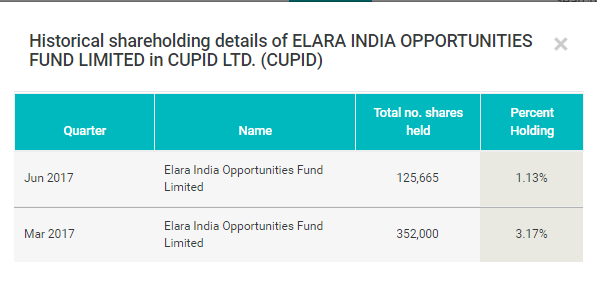

It seems Elara India oppourtunity fund is reducing its holding in Cupid…

DIsc - Invested

@MONK88888 content is here in detail:

http://www.prweb.com/releases/2017/10/prweb14760495.htm

I could not understand it well. Please write it in simple language.

Promoter’s holding reduced by ~ 3.94% in Dec, 2016 to March, 2017 could have played a role in price pressure. Few big investors has left it too. But now, three big investors are here. Two are 1-3 quarters old. I think, if promoters don’t sell, then big investors going out is over.

Am I to understand that you are enquiring about IXu -I have no connection to the promoter holding reduced story

The way I read IXu release: It is a message being sent to USFDA saying that their product , if not superior to current approved Female Health product is as good as their product. If they get approval , it is positive for Cupid -either Cupid could step in from contract manufacturing of view or Cupid could possibly get a quicker approval as their products are similar(when IXu product gets approved).

Like I indicated earlier , I did not scribe the promoter’s holding reduced…

Discl: No holdings in Cupid

1 Like

If promoters holding is not going to go down then I think, downside is almost nothing but upside potential is very good. Only three big investors are left. Two of them are new so no one should sell now. Time is ripe to grab it.

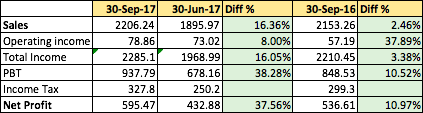

Cupid has posted decent numbers. Profit of Rs.5.9547Cr for the Q2 quarter, (QoQ 37.56% rise , YoY 10.96% rise). Sales has increased 16.36% QoQ, 2.46% YoY. Here’s the brief numbers in Lacs. Please refer below pdf link for more details.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/0982f3e7-1070-4966-b460-8eef0750990d.pdf

1 Like

I feel the problem with Cupid is there is no near term visibilty of earnings growth in terms of expansion or a way of strong earning rise ; for the last few quarters the quarterly earnings are in the range of 15 to 25 crores. It does n’t have any thing to feel confident that it will go to around 40 cr quarterly in the near future. Till that visibility comes, the market price will hover in the same range of 270 to 330. However, one of the straight forward and transparent promoter is a positive …

Disc: exited 2 quarters back

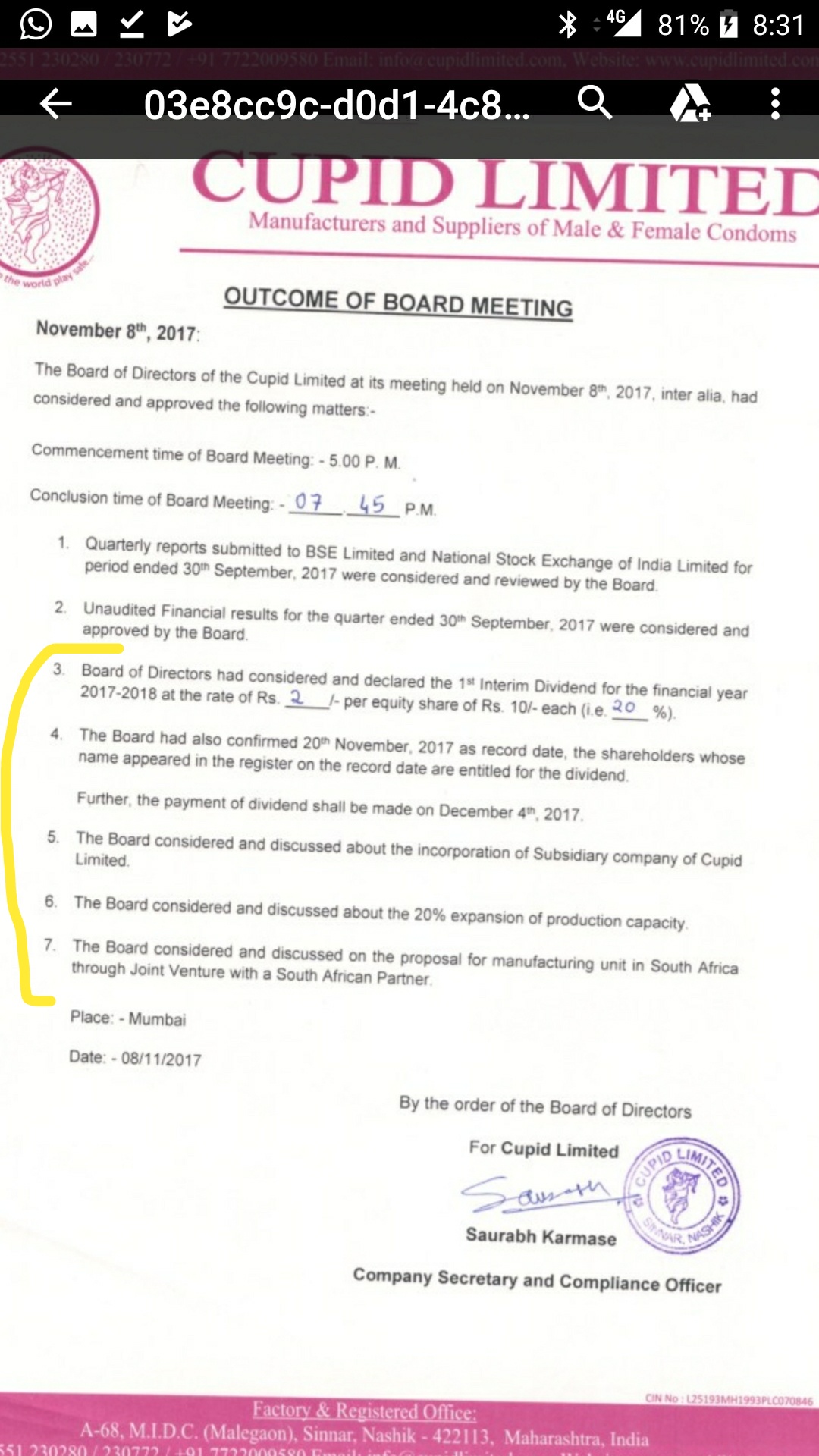

Decent numbers and some icing on the cake

• dividend of 2 per share ( 1st interim dividend)

• increasing capacity by 20%

• setting up subsidiary in south africa

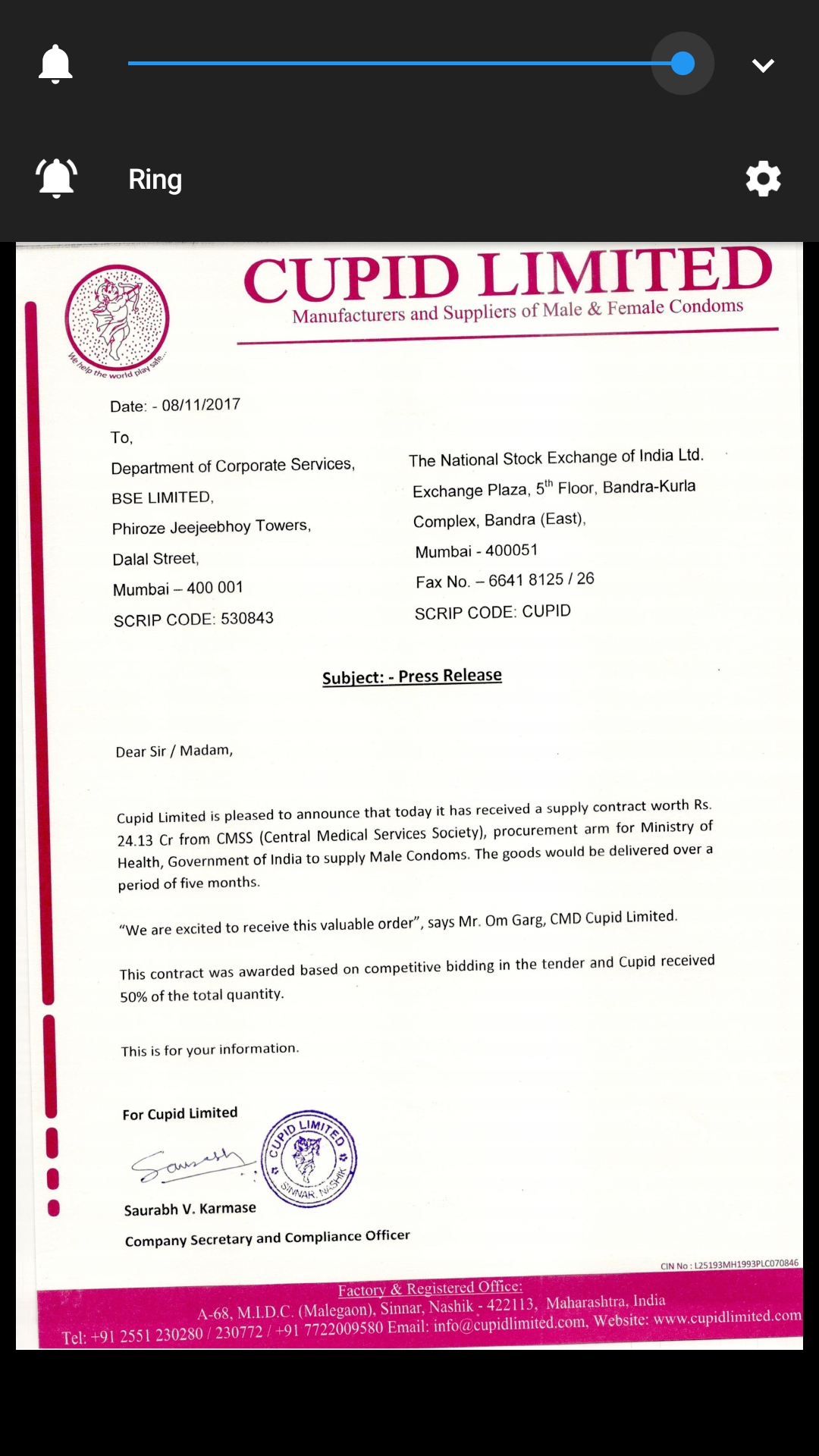

• another order from GOI to be delivered over 5 months worth 24.1 cr

3 Likes

Good results indeed.

So total order stands at 73 cr.

For the entire year, it comes to 73+ 19 ( last quarter) = 92 cr ( A mere 12 % increase YoY, FY 17 was 82 crs).

My guess is , Mr Garg is being conservative in the order book outlook.

The encouraging thing I noticed is the B2C online sales launch in december 2017.

The March quarter show start to show the results. This might be a big trigger for a rerating then perhaps.

As of now cupid is still very much a B2B company, so I think a re-rating to higher PE levels might still not be on the cards .

4 Likes

Cupid bagged an order worth of 24.13 crores from govt of India and they will be supplying over 5 months.if they are supplying within this year,then 4th quarter would be definitely excellent quarter.c1a0618b-de21-4e4c-900b-f4462ac7e7e1.pdf (672.3 KB)

2 Likes

Another Positive trigger would the Status of the prequalification of the WHO 3-year long term contract.

Would be safe to assume Cupid will get it…

More clarity will be known in today’s conf call.

1 Like

I may miss today’s concall. If anyone attending ,please as:

- Status of B2C leadership hiring and channel ramp up

- Status of African oppo discussed in last concall

- Growth rate of female condoms in India b2c qoq . When adoption is issues what makes them bullish

- Status of other products like wipes in pipeline

huh! why would someone buy it from Cupid if it is coming free ?

1 Like

A second-order effect of this could be positive for the over-all condom market. It could expand awareness and usage of condom at faster pace.

1 Like