They had another 1 on 1 meeting with institutional investor. Having not done/postponed earnings call, they seem to be communicating very little with retail investor. Though the results have been terrific.

Any idea what could be the reason ? Mostly when companies do well they talk more. Also, i have owned this stock for 6 months, were they historically poor communicator?

Hope someone finds an answer to the usability issues to the product in the concall. After my initial excitement i realised that the product was not very usable based on asking many doctors and fellow colleagues. Hence i have exited the position until clarity emerges.

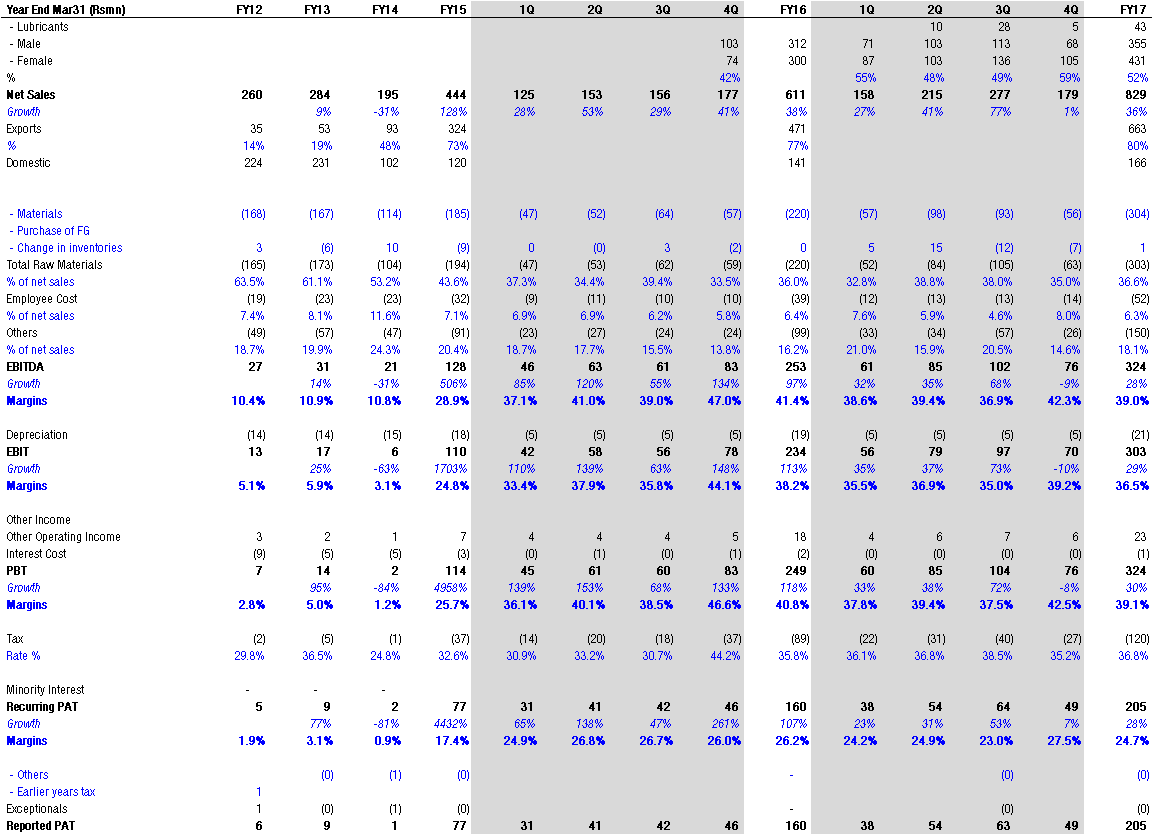

Optically, YoY, the results look good, but this quarter results were a bit below expectations (Mr Garg had indirectly guided for around 20 cr sales, but only 17.8 cr was achieved).

No evidence of the lubricant jelly orders ramping up yet .

No new visibility of the order book ( it seems to have remained the same , which is bad)

In short, we might have to wait a while for Cupid to get re-rated .

However, the silver lining is that management commentary looks optimistic .

The next two quarters might provide an insight whether the next growth trajectory is commenced or not

Although YoY results look good, the Q4 results are muted with very flat numbers. Operating income has 1% increase compared to Q4 FY-16.

Water base lubricant seems to be going steadily athough still very small part of overall product portfolio.

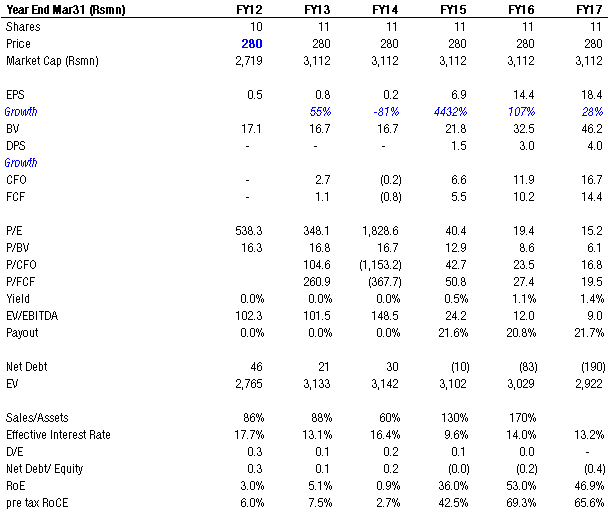

Market has reacted negatively, My thinking is compnay need to deliver 20%+ topline growth to sustain the valuation.

Disc- Invested.

Poor results. The pipeline for next year look similar to this year revenue, so growth could be flat. Not sure if diversification is yielding results but core growth commentary is to be watched carefully. the stock was not doing anything in last quarter with little management communication, cancellation of last quarter concall, one to one calls with institutional buyers and selling/moving of promoter stake.

Disc: exited major position still with small exposure.

Key Takeaways from Q4 Concall as per mgmt. guidance:

Revenue break-up: FC 52%, MC 43%, Water-based luricants 5% for FY 17. Change in Revenue-mix as per mgmt. guidance FC: 52-55%; MC: 35%; Lubes: 10%. Basic idea is to reduce low margin MC biz. And diversify into other products. Geographical Mix: Domestic (20%), Exports (80%).

Product developments: Patent acquired for sexual pleasure in MC ; 2nd Gen FC; Hand Sanitizer launched with retail strategy (domestic) + Sub-Saharan African countries for exports (as major players already in this space); Vaginal cream; Co. might distribute or manufacture Wet wipes for pre-mature ejaculation[400 mn USD market size in US] in India for US (Florida) based Co. in FY 19.

B2C expansion(retail sales) from 220 cities to 1000 town + cities in next 3 years. Online Sales: 2 lacs - FY 17; Overall B2C biz target of Rs. 10 cr with WC requirement of 4 cr; Readiness for B2C expected within 3 months; Sales Channel – Super distributors to Dist to Retail Stores (No agreements finalized yet with big names like Apollo Pharmacy, Religare); Advertising using Print Ads specifically stressed will not us TV medium due to costs.

Expected Order Book– 58 cr + 31 cr(repeat orders) = 89 cr. (Sales estimated at Rs. 97 cr for FY18).

Fundraising of about Rs. 25 crores in 1st Tranche. Purpose: 7cr Capex[imported machinery] by + 11 cr Branding & Promotion + 3 cr USFDA (initial testing) + Automation of plant.

Also, investors were curious to know about fundraising plans/progress of Co. whether through QIP/Rights Issue/Debt. Many raised concerns on equity dilution thru QIP route & investors requested Mr. Garg to consider Rights Issue.

Idle Cash of 19 cr on B/S to be utilized for Acquisition. (Prospective Target size : 20-40 cr; Domain: for new products(not condoms), mgmt. looking at Indian, South African cos.)

Seasonality in biz explained with Q1 & Q4 being weaker vis-à-vis Q2, Q3 due to budgeted amount of Funds/MoH being exhausted by Q4 & Q1.

Currency Risk: Rand/USD fluctuations not expected to be a problem. As Cupid has all contracts in USD, although risk through strengthening of Rs is mitigated by forward contracts.

Management Strength: Appointment of CEO - interviewed 4 candidates but still looking for a FMCG marketing expert. Investors suggested hiring consultants. Professionally + Experienced core team of 15-18 people in top management positions with Co.

SHP reduced 48% to 44% for buying family estate in NY.

No GST impact as condoms exempted.

Tenders: L1 in MC tender(GoI tender for MC took place after 3 years, FC tender to take place after 5 yrs.)

USFDA Approval allows company to sell FC for 2$/pc compared to current 0.4$/pc.

Weak Online presence (educational + advertisement purposes) compared to major competitor FHC (Chicago). Mr. Garg requested investors to help in contacting Digital Marketing experts to improve their online image.

Ease of Use + User acceptability: Mr. Garg responded by saying FC product preferred by Females as enhances pleasure with Inner ring & Sponge being much better in 2nd Gen FC assuring superior quality & performance.

Personally, I feel this year Change in Mgmt + Acquisition plan + USFDA approval for FC (in Oct 2016 concall said 12-18 months for approval i.e. expected by Q4 FY 18 or Q1 FY 19) + Sales & Marketing skills on execution seen on ground & online are triggers to be seen.

Acceptability & ease of use in FC can be validated only by success of mass retail strategy which is a tough ask and demands a dynamic team( as behavioral / buying process requires change in FC). For opportunity size to grow for this company, product & geographical diversification seems to be a better bet, considering FHC is already in biz since 1993. I feel existing business in FC can only propel biz soo far as it will attract competitors in this high margin B2B biz in future. Hence, introducing new high margin value added products can ensure sustainability of profits.

I think this would mean short term pain for financials and wait/hope for investors that management would be able to execute all these strategies. I think management is spreading itself too thin too fast. More so considering limited bench strength and management bandwidth as of now. So biggest risk is focused business delivering great return can easily become de-focused low return business.

Disclosure - Sold all shares before QIP. Watching with interest