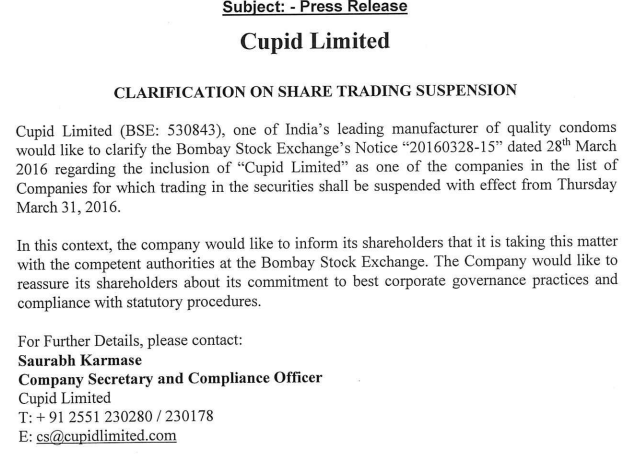

BSE has decided to suspend trading in the shares of Cupid Ltd. w.e.f March 31, 2016 as a surveillance measure to curb unusual price movement vis-à-vis the preferential issue price.

What is disturbing is that this action has been taken suo moto by BSE, with no notice being served on the Company. The decision to suspend trading & thereby harm the interests of the entire investing community has been taken by the exchange without even giving the Co. an opportunity to present its case.

It may be noted that even in cases of non-compliance, as per SEBI guidelines, a fair opportunity has to be given to the promoter/Company to rectify/represent its case before securities can be suspended from trading. Following the same spirit of law, should similar opportunity not have been accorded to the Co.?

If the fears of the BSE were that the promoters would benefit themselves by dumping its preferential allotment on unsuspecting public, then why not prevent the promoter from selling his shares? Why penalize the entire investing community?

Whose interests is BSE safe guarding here? Certainly not those of the investing public, which is now stuck with shares with no option of exit. Where BSE has really managed to succeed is in creating panic amongst the investors. Today there were hundreds of investors trying to sell today with no buyers.

The Mgt. I gather is working with the BSE officials, to revoke the suspension, so all is not lost yet. Perhaps, we Cupid investors can help our cause by highlighting the arbitrary actions of the BSE on social media.

Indeed this is a disappointing step by BSE. They have not given proper notice to the company neither have they published any warning letter in any newspaper and other media. Just putting a notice on the website one fine day will only hurt the investor community. Hope SEBI and finance ministry puts pressure on BSE to rectify the mistake and allow fair hearing on both sides.

Cupid should go to court and ask for a stay order on suspension. If bse is satisfied with requested documents, then there wouldn’t be any need for suspension. Once suspension is imposed, revocation may take its own sweet time.

ishank please share the names of the companies who had taken stay on the suspension

It would be very helpful as we can pass on the message to management of cupid.

Request all members to file a complaint with sebi on the link provided by @RajeevJ

once they receive multiple complaints they may look into the matter as investor protection case.

All members are requested to restrain while posting in favour or against. We have seen similar kind of chaos in other company threads and ultimately admin has to lock the thread. Keep a cool and balanced mind while posting. This is not a battlefield and you all are learned civilians.

It is interesting (& instructive) to note how regulatory actions are perceived in different light by the same people when they have skin in the game versus when they don’t.

It is rather unfortunate that BSE has tarred a number of companies with the same brush and Cupid investors in this case have been caught in the crossfire.

Let us step back and examine the situation. There is no denying the fact that there is rampant manipulation of stock prices in a number of companies listed on the BSE. There is various modus operandi to this manipulation and issuance of preference shares in one such route. BSE is rightly cracking down on this and we as investors will benefit from a cleaner system in the long run.

The investors of Cupid trust Mr Garg and feel that the company has been wronged by clubbing it with other unscrupulous elements. This is undesirable and could have been avoided. What BSE has done is against the principles of natural justice and will not stand in a court of law. This is presuming what the management is telling us about no notice being given to it and not being given a chance to explain its side of the story is true.

The first logical step for the company is to go to BSE and explain its position. If that doesn’t work out for any reason, then go to the courts to prove its innocence and get its status reinstated on BSE. It is extremely unlikely that the courts would not admit Cupids plea to seek recourse.

At this point we cannot be sure how long this process would take. Someone on this thread has mentioned that some other companies have managed to get this ban stayed/revoked. These cases can help us guesstimate the time lines.

Meanwhile i am presuming that the company would continue to manufacture and market its products. All this ban means is that we as investors will not receive the quotes that we receive on trading days which values the company either higher or lower in every trading session. However, this doesn’t take anything away from the intrinsic value of the company. If you don’t have liquidity issues and don’t need to sell, then nothing changes for you. We can argue that this could lead to a loss of reputation which can impact market value. This is true but at this stage it is very nebulous and hard to quantify.

Buffet had famously said that buy companies where you don’t have to worry even if the stock exchange shuts down for the next 5 years. I guess a number of investors would get tested now.

Your post made me thinking and went thru all the news information as given to BSE since 17-6-2010. I have some questions.

1.Preferential allotment on 17-6-2010 11.50 lacs shares @ Rs10.50. Market price Rs 9.88. What is the need for preferential allotment when the market price is Rs 9.88. Promoters could have purchased from the market. Share holding Pattern June Promoters 36.92 Public 63.08

2.Preferential Allotment Rs 15 lacs on 3-5-2011. Market Price Rs 7.93 Shareholding pattern June 2011 Promoters 44.46 Public 55.54

3. You find lot of intimation to BSE on receipt of orders ( even small orders), signing of agreements,etc. These are done regularly. What is the need to intimate each and every order received, even small ones.

4. There is no repeat of orders convincing ones. There was orders from India Govt for Nirodh but we all know how these orders are managed. There was an order from Brazil Govt on 30-7-2011 but no repeat. WHO orders can change any moment as international bidding/lobbying involved.

5. There is an intimation to BSE on DKT India , a charitable organisation. But in DKT website no mention of this. If it is such an important thing, DKT India should have mentioned it.

6. Safeware Company - If you see their site, there is no mention of any condom business as they are into Polyproplene business and no mention of any tie-up with Cupid.

7. After safeware news, promoters sold and till date there is no trace of Safeware Co, looks like a company with no history.

8. Please analyse the changes in shareholding for people holding more than 1%. I did from June 2010. You will find frequent changes in the list.

I may be wrong but my experience says when in doubt stay away. Only time can tell whether all these doubts will lead to something or just become useless analysis. There is so much data I analysed and I dont want put all the data here as it will clutter the post. Hence, I have listed my observations here but not conclusions. As a retail investor, it is very difficult to draw any conclusions or say anything with firmness.

Now from my 3 decades experience, I will explain about this warrants business.Please note lot of credence is given if it is direct purchase from market as it is a clean transaction.

First warrants are allotted to promoters. Funding comes from India or abroad . The fund from abroad can be a source of black money routed back to India. Local sourcing has reduced as there is lot of vigilance now. The money diverted to local operators to ramp up the prices. Since the companies dont declare where these funds are put to use. Now the promoters keep on selling the stake to unknown entities ( there are 1000 companies in India ) who in turn sell the shares in market and pocket the fees or profits. Let me not go into detail. Over the time promoters stake is reduced or stay their for namesake and these unknown entities are wound up or just disappear.

Since no debt involved , nobody bothers and equity risk cannot be questioned by a third party.

There is nothing which investors could do now as the onus is on the Company to come out clean. Only time will tell whether it is an error committed by BSE or a slow death for the Company.

My guesses or analysis may be wrong and Cupid in fact can turn out to be a good Company. But,as of now,there are doubts and there is no clarity.

@sethufan on your point one, preferential issue is made when company requires funds. When promtoters buy from market, company does not receive any funds.

Agreed. But preferential warrants are not issued for working capital needs and that too for a small amount of Rs 1.50 crore. The market cap was also around 12 cr ( Mar 14) around that time. Now it is Rs 322 cr.

Equity was diluted in FY07, 09, 10,11 and 12.

Cupid had borrowings of 4.9cr on the year preferential shares were issued last time i.e. FY12.

Here the problem is with price movement which happened due to the turnaround in the company performance. Net profit was 0.59Cr in FY12, improved to 12.59Cr. TTM, which is 21 times. Mcap increased to 350CR from 10Cr which is 35 times, which is due to premium given by market for its asset-lite business model and competitive advantage because of patent and approval with WHO etc. Mcap reached the maximum of above 550Cr. during Dec 2015. Important thing to note is promoters didn’t sell any shares during upmove and they also started paying the huge dividend in last 2 years. In fact, the total amount paid in dividends is around 5Cr. (including dividend tax), which is 50% of the then market cap.

It is not a secular growth from 0.59 cr to Rs 12.59 cr. It was only 5 lacs in Mar 14. Further, a stable EBITDA margin of around 11% till Mar 14 jumped to 30% in Mar 15 . How can one explain such a big jump which is not normally seen . Even in TTK, the turaround was gradual. If it is such a fantastic business, all Fund Managers should be camping in Garg’s office. There is no need for any more warrants.

Mind you, investment is made on future though one made Rs 5 lacs profit in the past.

why should shareholders poor or rich who sell on LC be compensated?Who do shareholders compensate when they make profits? Stock markets are about capitalism and not socialism.