Higher percentage of unrated indicates business opportunities for rating agencis ? Good observation? Can v quantify?

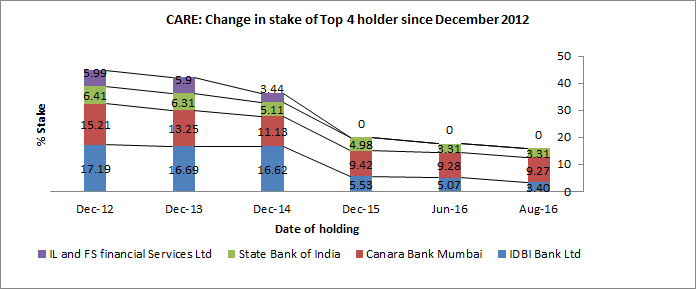

As some members have mentioned about constant sell from PSU stake holder of CARE, find enclosed change in stake of Top 4 Stakeholder since December 2012. Ther has been increase in stake by MF and LIC primarily and top 4 shareholder of December 2012, are no longer among top 4 holder (except Canara Bank) of CARE.

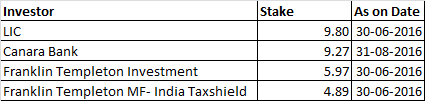

Find enclosed details of Top 4 holder (adjusted with latest disclosure til August 30 2016 on stock exchange)

Movement in Stake of Top 4 shareholder in Deccember 31, 2012

Disclosure: I have added my holding in the company during last 30 days and hence my view may be biased.

I have attended AGM of Care Rating in Mumbai on September 27 2016. Find enclosed my note on the meeting.

Disclaimer:

Please note that I hold share in the company and added my position in last one month. Also, note that there might some misunderstanding while taking down notes in AGM and hence reader shall aware about same. Also, all investor are advised to do their own independent due diligence as my views might be biased due to my interest in the company.

1) Rating industry overview

CARE is the second largest rating company in India. The demand for rating is depend on mainly on industrial growth. The credit growth in services and agriculture sector has limited direct impact on rating growth. Even bank credit growth, which in FY16 was more in retail/MSME and agri areas, resulted in lower rating revenue growth for the industry. In such difficult environment, the company manage to maintain its revenue.

Rating for small scale industry is driven by Government support on rating subsidy. During FY15 budget, the government grant for SME rating adversely affecting rating demand from the segment. Accordingly, the company reduce the manpower which was expected to work on small scale rating and manage to reduce the cost.

CARE has also entered into technical tie-up with Japan Rating Company. The main purpose of JV to develop mutually beneficial relationship. CARE has now an alternative to the client which wants international rating and do not want to go two established players. Similarly, JRC would assist CARE in getting business from the investment happening through Japanese investors.

CARE has also set up African and Nepal Rating venture. The African venture is currently loss making. However, the company is optimistic about prospect of same.

CARE has also acquired a small company which is in business of Risk advisory/ Early Warning Signals to Banks, which are related to rating business. CARE Kalypto has turnaround during year and provide for around 7% of consolidated revenue which come from non-rating business.

The company is also exploring certain opportunity of inorganic growth if it suit to core business and strategy of CARE. Having said that, the acquisition shall add to overall value of the shareholder in long term and the company would move at own pace and price when looking at acquisition.

CARE is intending to provide related products to existing client of around 13,000 and get more from of wallet share. For instance, CARE is considering providing TEV study for clients who would mean no marketing expenditure while adding to better utilisation of resources and very high margin addition.

Further, increasing focus on bond market development (even though partial cannibalisation from Bank loan rating business) is good for credit rating business as typical charge for Bond market issuer is around 8-10 bps (with cap on fee) as against Maximum fees of around 4 bps in bank loan rating business for the company. Please note that fees are bilaterally negotiated between client and company and hence may vary from client to client. The above figures are broad range of fees.

2) IRB Implementation

As per the management, In December 2015, BIS came out with paper which indicate that country which are under standardised regime, may continue to remain under same regime (India is currently under standardised regime). BIS experience with developed country has not been very good for IRB. There is inherent conflict for Bank’s system to be lenient to give rating to the customer which may result in higher risk and subsequent consequences. Hence, there is probability that IRB implementation may get changed or delayed or may have scope for external rating agency in some way.

3) BRICS Rating agency /Investor paid rating model:

Over last century, various model including investor paid and regulator controlled is tried. Even in developed market, after all experiments, issuer paid model is only found viable and hence the company does not see same being changing in medium term.

On BRIC rating agency, one needs to wait and watch for further actions.

4) New Area and Business outlook

The company is considering India REIT rating, NGO rating, Green rating as new area to augment revenue from same clients. CART, 40,000 issuer rating database compiled from all 6 rating agency is getting good traction in market and contributed to around Rs 3 Cr revenue to the company. Further, with expected decline in interest rate, revival of infrastructure and economy recovery, and NPA problem reached to peak, CARE expect willingness of borrower and ability of lenders are at take off stage for FY17 and hence optimistic.

5) Usage of ~ Rs 400 Cr Marketable investment and Cash

There were nearly 4-5 investor (including institutional investors) asked for management view on utilisation of funds. The management said that there has been new MD who just took charge of the business. Couple of directors are also new to the company. Hence, they would take some time to see company growth strategy and opportunity for inorganic growth in related areas to take considered view.

There were suggestions by many shareholders that CARE may consider buyback of share instead of increased dividend payment (in context of higher tax leakage due to DDT/Dividend tax in more than 10 Lakh per annum). Further, certain shareholders are constantly exiting from the company in open market which may also get opportunity to exit from the company at the same time, remaining shareholder gain for lower equity base resulting in higher EPS and RONW. The management promised to look into same and take appropriate action.

11 Likes

A very interesting development for Credit Rating industry from Muncipal Bond market. The artcile indicate, as against total bond outstanding of Rs 1,500 cr over 25 years, during CY2017 only around 6000 Cr of new bonds are expected to be issued which supports credit rating industry. CARE is expected to gain from this growth in Muncipal bond market.

1 Like

@dd1474 why specifically CARE? In general, yes credit rating agencies will gain but the article doesn’t mention CARE

Disc: long since a long time, no intention of selling

Care is second largest market share holder in Indian credit rating business. Assuming other thing being same, CARE would be major beneficiary along with other rating agency. Also, while Crisil and ICRA other two rating agencies also have other advisory and information business, CARE is pure India credit rating link listed play. So crisil being major gainer due to highest market share, the impact of same not be as high as in case of Care as research account now more than credit rating revenue.

Disclosure: I am holding care and my view may be biased.

Q3 FY17 Results

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/E5421133_0334_4106_8BDC_87A5F6F7A0CD_184344.pdf

Top Line 65.94cr (Dec '16) vs 63.92cr (Dec '15)

Net Profit 45.15cr (Dec '16) vs 26.80cr (Dec '15)

2 Likes

Crisil has bought 9%+ from Can Bank in Care today in a block deal

1 Like

I am not able to understand why spot is up 13%. Canara sold and Crisil bought the same number of shares. How does this affect the fundamental value?

crisil buying care shares might signal a consolidation in ratings market

2 Likes

-

The deal happened at the price of ~1660 Rs / Share.

-

It is like Dolly Khanna buying share of an obscure investor :).

-

Competitor buying has its own interpretation.

1 Like

- Hard to find a reason more than just being a financial investment for Crisil. Why would a #1 player acquire a non-strategic + non-board seat in #2 player

- I don’t see consolidation as a reason as competition tribunal may not approve deal

- One major sword on the price is off. SBI + IDBI stake of 6+% could be sold in the next few months as well. Then the valuation could catch up to that of bigger n smaller peer(s).

- Triggers like Munis bonds (absolute wild guess) could apart from expanding Sme market. Then Crisil may sell stake.

Interesting story to unfold

I think this is buy out by Crisil is pure hubris on their ( CRISIL Management) part, they could have accumulated the same some time ago when the stock was trading at 52 week low, but no they went and bought the stock at premium (400 Cr for 26.50 lakh shares). On top of it CRISIL claims that its an investment, now i expect a rating agency to at least arrive at a fair price, but here CRISIL has all but given to that mania of Mr. Market. Lets keep a watch on share price of CARE and see what is the return CRISIL going to get in next 3-4 years.

3 Likes

The irony is that the experts of fair value whose job is to figure out fair value day in and day out paid a premium to a desperate seller… for no real value than a sheet of paper showing the quantity… who could have well accepted a discount… pure hubris…

2 Likes

This hubris is good for us because as a value investor I can profit from the greed and fear of institutional or so called efficient investor.

1 Like

Another view is CRISIL is trying to take over CARE. .

1 Like

I doubt they can take over CARE because of Regulatory issues, and even if they do, its good for CARE shareholders as we stand to gain from the takeover.

lo and behold: http://economictimes.indiatimes.com/markets/stocks/news/now-fitch-makes-a-move-for-care/articleshow/59521321.cms

1 Like

I have attended AGM of Care Rating in Mumbai on August 1 2017. Find enclosed my note on the meeting.

Disclaimer:

Please note that I hold share in the company. Also, note that there might some misunderstanding while taking down notes in AGM and hence reader shall aware about same. All investors are advised to do their own independent due diligence as my views might be biased due to my interest in the company.

1) Rating industry overview

CARE is the second largest rating company in India. The demand for rating is depend on mainly on industrial growth. During FY17, growth in bank credit was in single digit at around 8.7% as compared with 10.9% in FY16. Bank credit growth was driven by the services (19.5% growth YOY) and retail segment (16.7% growth YOY) in FY17 which generally have lower impact on credit rating growth. Further, industrial growth continue to remain during FY17 at 5% as against 3.4% during FY16. Growth in Corporate bond, however, assisted the company during FY17.

CARE has also set up African and Nepal Rating venture. CARE also promoted research and training subsidiary named CARE Advisory and Training Ltd (CART) to enhace revenue from non-rating business. During FY17, CARE took lead in developing new credit rating system as suggested by Ministry of Finance for Infrastrcuture sector which would comment on the expected loss (EL) of debt instrument after factoring probability of default (PD) and recovery propsect. This is expected to assit Infrastructure sector to get credit on better terms as recovery on default for long tenure revenue generating assets is much lower than typical industrial unit.

Increasing focus on bond market development (even though partial cannibalisation from Bank loan rating business) is good for credit rating business as typical charge for Bond market issuer is around 8-10 bps (with cap on fee) as against Maximum fees of around 4 bps in bank loan rating business for the company. Rating fees are bilaterally negotiated between client and company and hence may vary from client to client. The above figures are broad range of fees.

There is no linear relationship between number assignment and rating fees. The reverse bidding and tender based bidding also at time result in lower rating fees. So the company take call on rating fees after considering all factors like relevance of customer, size of mandate, potential to grow business, competition intensity and efforts involved while quoting its fees. Over a period, industry size is growing and with increased efforts from regulator to shift large borrower from bank to bonds market would augur well for future of the company as in the listed bond issuance there are no substitute to external credit rating. (Bank may do rating internally and avoid external ratings).

In developing new grading/ ratings products in area such Real estate, Education, Environment, Infrastructure and Training instituion would also provide growth for the company.

2) Internal ratings-based approach (credit risk) - BASEL Implementation

In 2016 AGM, Mr Mokashi indicated that BIS experience with developed country has not been very good for IRB. There is inherent conflict for Bank’s system to be lenient to give rating to the customer which may result in higher risk and subsequent consequences. Hence, there is probability that IRB implementation may get changed or delayed or may have scope for external rating agency in some way. During FY17, while there was no official communication, informal belief in regulator is stregnthen to continue to have external rating instead of internal ratings of Banks.

3) Brand building and name change

During FY17, the company changed its name from Credit Analysis and Research Limited to CARE Rating which is popular name by which it was known among the clients. The company further increase brand building advertisement by increasing spending on ET Now and CNBC to market its own identity to relevant audience.

4) Usage of ~ Rs 450 Cr Marketable investment and Cash

The board would take some time to see company growth strategy and opportunity for inorganic growth in related areas to take considered view.The company would consider inorganic growth opportunity if it suit to core business and strategy of CARE. Having said that, the acquisition shall add to overall value of the shareholder in long term and the company would move at own pace and price when looking at acquisition.

5) Crisil Acquistion of share:

Crisil express that the investment is purely financial investment. Crisil does not have any special rights. Management were asked that by not utililsing available cash through buyback, they allowed Crisil to take oppotunity to acquire the stake in the company. Management said that there is nothing more to share with shareholder on Crisil acquisition of share. Business continue to remain as usual as it was before Crisil being shareholder. The comapny would run as independent company run by competent professional management as in past.

Other points

There were suggestions by many shareholders that CARE may consider buyback of share instead of increased dividend payment (in context of higher tax leakage due to DDT/Dividend tax in more than 10 Lakh per annum). The company confirmed that busiess has not impact of GST/deomitisation in short term. All these would result in higher share of orgnaised sector which shall be positive for Rating industry as it would have more rating clients which increased market share of organised sector. The comapny has taken temperorary employees which resulted in higher other expenditure. In Nepal, the company has started rating business. The new NPA resolution under IBC also have specific role for rating agency and CARE expect to gain more business from this area.

20 Likes

Thanks.

very useful info.

Prashant