CP touches 350.Seems post AGM it has caught the attention of investors and analysts.Also the warrant issuance overhang gone.Stock is getting rerated.

How big is the opp size?only 600 crore as mentioned in BT or could it grow to more?

CP touches 350.Seems post AGM it has caught the attention of investors and analysts.Also the warrant issuance overhang gone.Stock is getting rerated.

How big is the opp size?only 600 crore as mentioned in BT or could it grow to more?

Vardha,

Your question ask me do some more work with numbers. I did same. Find enclosed data point for three companies

We have three companies named as A, B and C with PBIDT (approxiamation for EBITDA) and CFO. The figures are actual. Which one would be good companies based on the above table?

Hi Dhiraj,

If you want to become cash flow buff, read Creative Cash Flow book, pdf available on net and Quality of Earnings book this too you can get it from net.

Both above books are amazing

Also Do Remember that even Cash Flow can be manipulated (read Financial Shenanigans to know more).

@mmpcse; @varadharajanr

The table are in context of Vardha concern about lower Operating Cashflow/EBITDA for Control Print. Vardh did raise valid concern about lower Operating cashflow/EBITDA which led me to do some more number crunching. I enclosed the table to get reply from Valuepickr as which company you would like to invest based on the numbers in table?

Thanks for sharing details about Cashflow management and manipulation.

Company A is Page Industry, Company B is Suzlon and Company C is Opto Cicuit. So CFO/PBDIT Ratio for Page industry also appear very mediocare at around 40% if we take FY11-FY14 period. Not that free cash are not important, but isolated ratio would give incomplete picture. That is the limited point.

Thanks Vardha for raising valid concern which resulted some more number crunching and conviction in process.

Also keep close watch on Cash Conversion Cycle (CC Cycle), here in this case link here CC Cycle latest 2015 has CC Cycle is 205, coupled with this we need to have judgement on working capital requirement to support up to 205 days, if they have sufficient cash then it can be managed or else it may lead to fund rising.

I think CFO needs to be adjusted by removing interest portion before calculating CFO ratios.

It will give a much better picture. Also 4 years is a too small data point to see the true picture

I am still not sure why Indian accounting allows interest portion of debt being added first in CFO and then subtracted in CFF. Because of this rule, CFO for most debt ridden companies appears much higher than it actually is. I find US GAAP much better in this respect.

@dd1474

I am happy we are engaging in a good constructive discussion here. Do not look at CFO in isolation but look at it before and after WC changes and find out what constitutes it - for eg., in company A’s case if there was a build up of FG and it translated into sales (next year there was a decrease or very small increase), then the company was on the right path in stuffing the channel sensing a growth opportunity.

However, a relentless increase in FG over 2-3 years is a flag and similarly so with RM inventroy and WIP inventory. I spend time trying to visualize what the promoter would be saying by drawing a mental tree in my mind and see if the numbers fit in. for eg., increase in FG for a year means bullish times ahead. Increase in FG for two years ahead of sales growth means an amber flag - for three years is a red flag.

and aman’s point is valid about interest expense getting added to CFO to give an artificially high figure. The CFO I use is “owner’s earnings” - EBITDA adjusted for WC plus maintenance capex. The issue with CP is the adjustment for WC, which is relentless across years.

@varadharajanr Sir as we are discussing about the CFO and building up of inventory topic, I want to talk about Lloyd Electric. Their management said that they are using push through method to promote their product and that method deteriorated their Balance sheet and increased their Working Capital They said they initiated that strategy 3 years back and now they are reaping the benefits of it. The point I am trying to understand is that what amount of WC increase is right? They said it took them 3 years but you said (I trust your analysis because you have seen so many companies) that 3 year increment is a red flag. Can you give your comments on that? because I feel (but I have not done industry analysis) for companies which trying to become Business to COnsumer companies, 3-4 years of WC can be quite natural.

Great Set of Numbers from Control Print:

Net profit of Control Print rose 40.46% to Rs 7.29 crore in current quarter as against Rs 5.19 crore during the previous quarter. Sales up 28.30% to Rs 36.63 crore in this quarter as against Rs 28.55 crore during previous quarter.

Though Finance cost is double compared to last year (still 72 lacs). Have they increased debt?

Great Set of Numbers from Control Print:

Net profit of Control Print rose 40.46% to Rs 7.29 crore in current quarter as against Rs 5.19 crore during the previous quarter. Sales up 28.30% to Rs 36.63 crore in this quarter as against Rs 28.55 crore during previous quarter.

Though Finance cost is double compared to last year (still 72 lacs). Have they increased debt?

Disc: Invested from lower levels.

I think no one’s looking at the ballooning receivables - the company now has Rs. 35 Cr. of receivables outstanding - up from Rs. 25 Cr. last yoy.No wonder the company authorized an increase in authorized share capital

Look at operating cash flows - all of the profits go back into inventory of FG that they maintain at customer’s end. I am not sure if this is healthy in the long run. This is reflecting in the increasing WC debt too whch is up 25 % or so.

vardha ji

increase in authorized share capital is the first sign of raising funds to fund working capital ? (eg : through debt) or any other plan they have for rise in auth capital.

even eros has ballooning receivables, as we knew recently news on eros.

My only concern remains about large inventory holding and probable obsolescence of the same

in future.

I raised this issue on MMB too, got attacked by other boarders. Looks a bit like Indian Terrain, but different industries.

Invested in Control Print since Rs 200 level, will probably get out around 500-550.

Control Print call board meeting for Bonus:

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=a43792b6-4cf6-4077-b11b-f0baca5d34df

While is no way its change fundamental of business, for strange reasons, market participant become optimistic for company which declared bonus. I would rather happy with stock price going in 4 digit over period of time, as it reduce volatility in stock price movement which is what I like. But then, market has its own way of evaluation.

Happy Diwali !!!

Inventory turnover ratio and account receivable ratio over last 5 years are consistently stable which I believe is not bad. Contingent liabilities also looks pretty much under control (it shot up a bit in 2014 but came down in 2015).

'15 '14 '13 '12 '11

Inventory Turnover Ratio 2.06 1.97 2.48 2.55 2.13

Debtors Turnover Ratio 4.48 4.14 4.23 4.20 4.33

As far as accounts receivables are not becoming bad debts, it shouldn’t be an issue and because they have a stable patterns of inventory since this long I believe it makes their business model credible.

Please correct me if my interpretation is wrong.

I understand equity master in one of the service has recommend Control Print as an investment idea with report released yesterday. That might be reason for today’s surge in price ?

This business model with its extremely high WC cycle is surely not scalable, I suspect the company is winning over business by promising its clients quick service ( and loose credit terms as Vardha highlighted) through storing inventories at their premises, this is however at the cost of high inventory risk and not a viable long term business model as its competitors probably know well.

The business has no FCF to speak of , in the good years of fy 14 and fy 15 when it did manage to generate OCF post WC , its purchase of fixed assets exceeded the OCF number, the difference in some cases was made up through “sale of investments”- another poor quality source of cash.

The other positive of no/low debt doesn’t quite hold up either as the company has been injecting cash through issuance of warrants, they likely got rejected by the banks otherwise they would have simply raised more debt.

In my view, only if the business is able to drive revenues and profits AND lower its WC cycle at the same time, does it become a viable investment candidate.

Accounting is not just bean counting, it explains the business dispassionately and far better than words ( often hyped) ever can.

Bobby

Appreciate your your message.

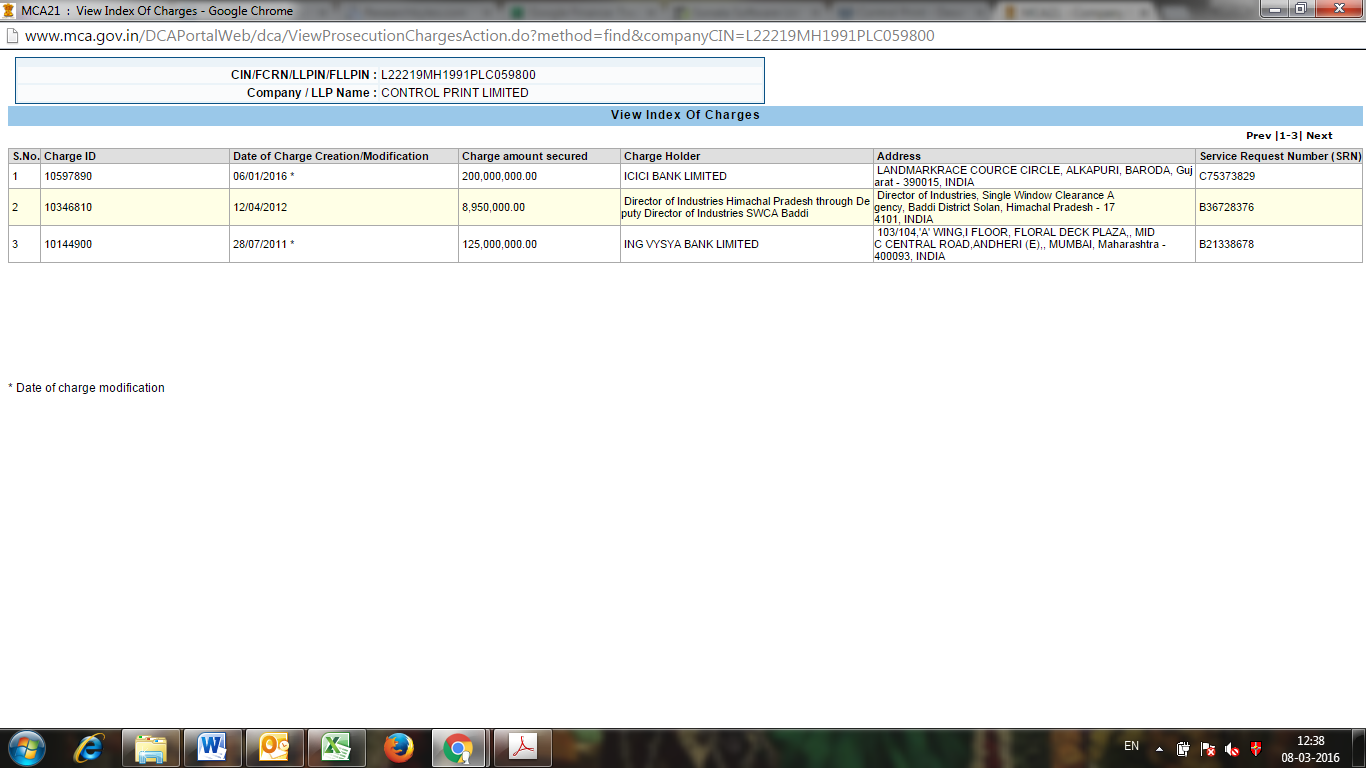

However, please go through past message on the this board. Just looking at number in isolation would not make any sense. Also, I doubt that the company has any issue with getting bank limits. As on date, the company has filed charges with ROC which indicate that it has fund based limit from ICICI Bank And Kotak (earstwhile ING Bank) which are reasonable lenders in my opinion:

The specific point I bring to your notice is about Page Industries free cash flow. We would have missed Page industries also going by this parameter as I explained in previous message on the thread.

The business is not HLL/Nestle kind as I told in past. However, it is good 15-20% compounding over next 3-5 years. Please also look at dividend payment of the company in in FY16. It has gone up significantly during FY16 which give support to argument of genuine cash flow from the business. The interim financial continues to very low debt equity ratio. So only possibility for the numbers to fraudulent is promoter infusing his own money and paying dividend.

In my test, consistent dividend with limited debt over 3-5 years is a very good business model.

Once again thanks for your view and do look forward to get more points on discussion.

Disc: My view may be biased as holding share of the company for last 10 months.