Steel sector :Crisil report

https://drive.google.com/file/d/1se5yJOdoYQTfcW7y9gdLslURq1gNtM_Z/view

@jitenp thanks for sharing the wonderful presentation. can sanghvi movers be a good cyclical pick right now , given the fact wind sector is going through bad times. Lots of scope for operating leverage in the stock. its capacity utlilization and yield are on the very low side currently. Once the cylce turns it may be the first to benefit, given the fact it has 70 % market share in the crane leasing industry.

Is anyone tracking companies producing H-Acid and Vinyl Sulhpone ? China is closing down factories and domestic companies in this sector are carrying out expansion as well as pricing has surged recently resulting in cycle being up for next 6-12 months. Plus major part of sales of such companies come from export so rupee depreciation will also add to the revenues and profitability. Last time the cycle went up in 2016 when stocks in the sector gave multi-fold return. Can the same repeat this time ??

Companies in the sector likely to benefit from the above cycle includes Bhageria Industries, Kiri Industries and Bodal Chemical.

3 Likes

Kiri and bodal are well placed in dyes intermediatries, bodal has just completed expansion, kiri is doing expansion in disperse dyes,

Disclosure: invested in kiri industries

2 Likes

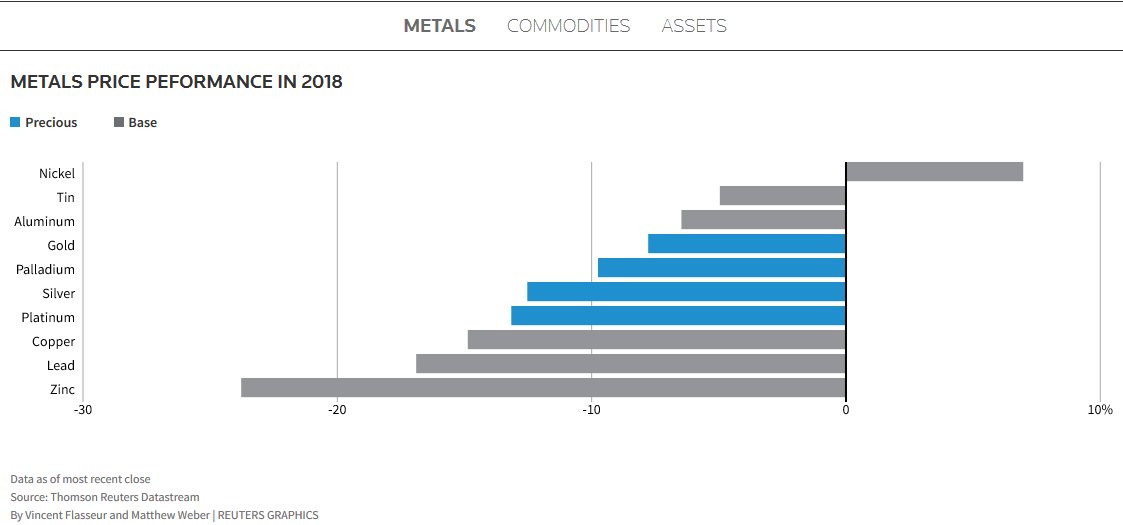

The lacklustre performance of the metals sector so far in 2018 as a result of recent declines due to Trump’s trade war, with only nickel posting gains.

What is everyone’s view on Indigo? It seems to be the perfect case of a good company facing tough times in a industry that’s facing even tougher times. Falling rupee, escalation in fuel costs have dented the profitability a lot. This clubbed with fall in ticket prices for 0-15 days across the industry has led to pricing pressures.

Now Indigo has the most optimised pricing structure among the domestic carriers. In addition, it has A320NEO’s which are 15% more fuel efficient than A320CEO. I won’t go into more details of the company as they are covered in depth on the relevant thread. Why I posted this here is because I feel that due to the commodity nature of the industry (to an extent), these might be good times to buy. All the indicators are there- fall in OPM, profits, industry distress (look at Jet). At the same time, number of people flying will only increase with time.

Jiten Bhai ,

Your current outlook on ferro alloys sector , since you were bullish and exposure some cpl of months ago .

Disclaimer: having significant exposure in IMFA

Unfortunate PSU giant is not taking this opportunity to increase the market share thereby reducing the import. This time it will be different for Hind copper is belied. Our investment in Hind copper appears to be down the drain.

Is any one tracking cotton prices, have been checking Indexmundi site and the prices are at the peak.

I believe this should be -ve for Trident, Ambika Cotton,Nitin spinners etc but when I had seen the Q1 results they werent that bad, am I missing anything?

2 Likes

For Trident, it may be slightly negative as realizations would be higher given recent rupee depreciation.

For Ambika, Nitin Spinners the spread between yarn and cotton is determinant of margins. Generally, the spread is around Rs90/kg. Unsure what it is currently

1 Like

Thanks @bhavveshh for the details, for Ambika and Nitin does it mean that an increase in cotton price will be factored in the yarn price that they sell to the customer?

It depends on demand supply of yarn. So as of now what I understand is China is buying yarn from India after it applied duty on mports of cotton from the US. So yarn and cotton demand is high.

Now key would be to watch out cotton arrivals in September in India

If the availability of cotton is good and priced fall, it’s good for yarn makers.

The situation is very dynamic and can change quickly. I don’t track Nitin and Ambika so can’t comment on them specifically

It was very nice to talk my heart out on the Unlimited Abundance Series.

Here I talk about my investment philosophy, value investing, cyclical investing, investor traits and so on. Duration is 50 minutes, so be forewarned. Views welcome.

26 Likes

Hello jiten sir very knowledgable session.sir you mentioned about sugar cycle downtrend in 2013 which are industris in 2018 which are in down trend present

Excellently explained bade bhai. Enjoyed the way you explain investing

1 Like

Local Cos Fear Dumping by Foreign Steel Players

Firms expect China, Japan and Korea to divert shipments originally meant for US, EU to India; ICRA says rupee’s fall may boost steel exports

Vatsala.Gaur@timesgroup.com

Mumbai:

India is facing the threat of dumping of foreign steel, led by the diversion of exports originally meant for the US and European Union, which could lead to an encore of 2016 when local mills making the alloy were crippled by shipments from overseas, fear domestic steelmakers.

Ratings firm ICRA, in a note on Wednesday, said in the first quarter of fiscal 2019, the country’s steel exports dropped by over 33% whereas imports grew more than 11%. Consequently, India turned a net importer in the quarter, after having been a net exporter for the last two years.

However, with a sharp rupee depreciation in recent months, the ratings firm expects a slide in steel imports and boost to exports, which is likely to improve India’s overall steel trade balance.

The industry has started “sensitising” the government to take action to check unfair imports that could accelerate in the future. It wants the reference price of the antidumping duty to be pushed up or a replication of what Europe has recently done to protect local steelmakers by providing safeguard measures.

“In the last quarter (first quarter of FY19), China, Japan and Korea diverted twice their export to the US into India,” Seshagiri Rao, joint managing director at JSW Steel, had told reporters in July at a conference held to announce the company’s first-quarter results. He said the imposition of safeguard measures by the EU would hit the industry more in the coming quarters.

He had bolstered his statement with data from the last quarter. Imports into the US from China, Japan and Korea reduced by 240,000 tonnes after the imposition of tariffs. But their collective shipments into India increased by 450,000 tonnes.

“Countries are putting safeguard measures to protect their domestic steel industry against unfair dumping. The Indian government had taken safeguard measure by way of reference price at $480 per tonne to curb dumping. This has now become redundant in view of the higher international prices. Consequently, imports into India have risen by 31% in Q1 of FY19 compared to Q4 FY18. Hence there is a definitive case for revision in reference price,” said an Essar Steel spokesperson.

While the US had, in March, imposed a 25% import tariff on steel entering that country, more recently, on July 18, the European Commission announced safeguard provisional measure to curb diversion of exports to Europe. According to the measure, a 25% tariff will be imposed once imports exceed the average import of the last three years. This will be applicable to all countries save some developing ones.

“Unlike the USA, the EU tariffs would be more worrying for Indian steelmakers, given that export volumes by Indian mills to the EU are over five times of volumes exported to the USA," said Jayanta Roy, group head of corporate sector ratings at ICRA. “Moreover, as per India’s Q1 FY2019 steel import data, redirection of impacted steel volumes from countries like Japan and South Korea, with whom India has free trade agreements, is clearly visible.”

Hello all.is any one following close to adhesive and granite industries?