How does this may have impact on Indian Copper industry and demand?

Hi, there have been imports of these products into India and it is stated in National Peroxide last five - six annual reports. Also, in July 2017, anti dumping duty was imposed by India. So, if imports are coming then I believe exports are also possible here. However, traders do validate your point that it needs specialized bags to transport the material.

Gujarat alkali and chemicals also manufactures peroxide

Hi Jiten - so what is your estimate of 1) Graphite India peak earning and 2) HEG peak earning?

Are you still looking to accumulate these or have you have sold off?

Thanks

Con call of meghmani indicates that H2O2 project (100Cr capex) is well on track and expected to add value from FY 20. Chloromethane plant (40000 MTPA) is expected to be commissioned by Dec 2018.

I am unable to correlate the Dec 18 with H2O2. can u provide the source of your info. Thanks.

No positions currently in any GE players.

Graphite electrode prices currently around Rs. 950/kg.

1 Like

That translates into USD 14,600 per ton approximately for GE. I am not very sure about the current needle coke prices, as latest info on the same is not available to me. As per my calculations, for Graphite india, realization for GE during Q3 was around USD 6,600 per MT and needle coke around USD 1,270 per MT. That means, it was approximately 20% of the GE cost for needle coke. Hence, for USD 14,600 of GE cost, needle coke cost works out to be USD 2,920 per ton. Assuming that, other costs involved in the production of GE would be more or less fixed (on par with Q3) and the GE and the needle coke prices stay as mentioned above during FY19, I calculate an EPS of Rs. 197 for FY19 which is 7.4 times the current TTM EPS.

2 Likes

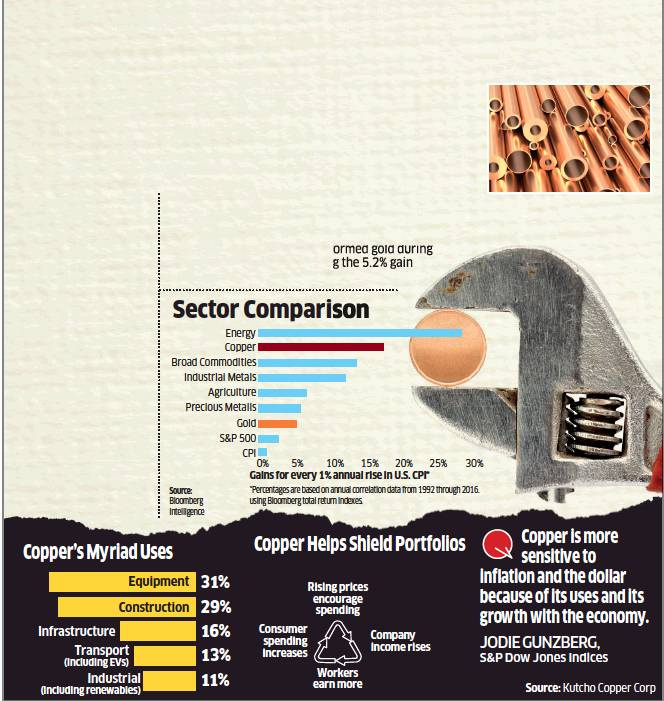

Copper as an Inflation Hedge

Every year, a vast amount of copper is used by the global economy to manufacture a wide variety of goods.

Copper outperformed every major asset class aside from energy - a type of asset that tends to increase rapidly during inflationary periods as well, though usually with high volatility. Copper also outperformed gold during rising consumer prices, tripling the 5.2% gain logged by gold.

1 Like

2 Likes

hi Jiten,

Do you mean 6-8 times of previous cycle peak earnings?

If i am wrong can you elaborate a little more?

thanks and regards

vinay

I try to do for current cycle. And that does require deep understanding of industry. Tailwinds, headwinds, supply, demand scenario. And some personal judgement too.

But, doing it for past cycle also may not be a bad idea, if one is not able to come up with the nos for current cycle.

The most important thing in cyclical/commodity investing is getting in early. Chances of big erosion of capital is always there if one enters late. As upcycles and downcycles are never linear. And one get’s intermittent corrections on both sides. The problem is understanding whether it’s an intermittent correction or a change of cycle.

So, basically, never try to milk the full cycle, and leave some potential gains on the table. Basically, getting out a bit early. As capital preservation should always be foremost in mind.

13 Likes

Hi @madhavikkutti - Have a couple of questions

- Can you please let me know for Graphite how did you arrive at USD 6600 per MT as the realization. I did some calculation and doesnt match with the figure.

- From the Q3FY18 presentation the current utilization of Graphite India is 95%, which leaves very little room for volume growth, the play in my opinion would be the new contracts that gets negotiated with the market price which might boost the top line and bottom line, what is your thought on this

Your thoughts on hospitality sector? Occupancy rising (up over 65% for the first time since 2008). Will gradually move over 70% in next few years. ARRs are expected to rise then. Have you followed the past cycle?

Hi @pandi.rao, Please see if I have made any mistakes in the following rough calculation:

Total Sales for Q3: Rs. 9,33,06,00,000, which is approximately USD 14,57,90,625, assuming 1 USD = INR 64, as it was the case when I originally calculated it.

Assuming a capacity utilization of 90%, for the Q3, we can approximate it to 88200/4 = 22,050 MT

Now, if we divide 14,57,90,625 by 22,050 we get USD 6612 per MT.

In fact, volume growth during FY19 is hardly of any concern. As per reports, even achieving utilization of the 90% of the existing capacity may become a challenge due to the needle coke shortage going forward.

I feel that, going forward, about 60% of the capacity will go into short-term quarterly contracts (for say, USD 10,000 -15,000) and the remaining 40% may be sold on the spot market at higher prices (which can be even for more than USD 20,000 per MT).

Please note that, all these are based on my best judgement, after going through various news articles and I may prove to be wrong.

Why do you think there will be shortage of Needle coke going forward?

As per what I read, needle coke industry is oligopolistic with top 5 players accounting for more than 80% of world’s capacity. Going forward, any increase in the production of needle coke is expected to be offset by its increased use in lithium-ion batteries (due to the increased usage of electric vehicles and phones), creating more shortage for the GE industry

1 Like

Hi @madhavikkutti thanks for getting back.

Have a query on the calculation.

The Q3 FY18 is the standalone figure, since being a standalone number I assume the sales from the German plant which contributes around 18,000MT is not reported on a quarterly basis (correct me if I am wrong).

So the 90% should be on the 98000-18000 = 80000MT. which is 72000MT

Now assuming the Q3 result reported is for their entire capacity (98000MT) and 90% is 88200, I did not understand the 88200/4 = 22050MT figure.

Can you please highlight that.

Also as mentioned above the current utilization is 95% as reported in the Q3 FY18 investor presentation.

So based on that we may have to re-calculate the realization accordingly.

2 Likes

Are there any needle coke companies listed in India? There are some Calcinated Petroleum Coke (CPC) companies like Rain Industries, Goa carbon etc… but are there any needle coke manufacturers?

1 Like

Thanks for these points @pandi.rao. I have divided the overall capacity by 4, as we have to consider the quarterly capacity of Q3 for our calculations. Following link clearly mention that the total capacity of 98000 is yearly and not quarterly: http://www.graphiteindia.com. Anyone, please correct if my above interpretation is still wrong.

Regarding the standalone results, I think you are right. However, when will the Dec quarter numbers for the subsidiary be published and where to get the same?

I feel, if we consider the subsidiary numbers into account, price realization for GE will be even further high as the numerator in our earlier calculation will increase further keeping the denominator the same.

1 Like