@jitenp bhai,

Are you tracking financial sector as a cyclical play ? do you have any observations on the same…could you please share…

Thanks

Vishal.

@jitenp bhai,

Are you tracking financial sector as a cyclical play ? do you have any observations on the same…could you please share…

Thanks

Vishal.

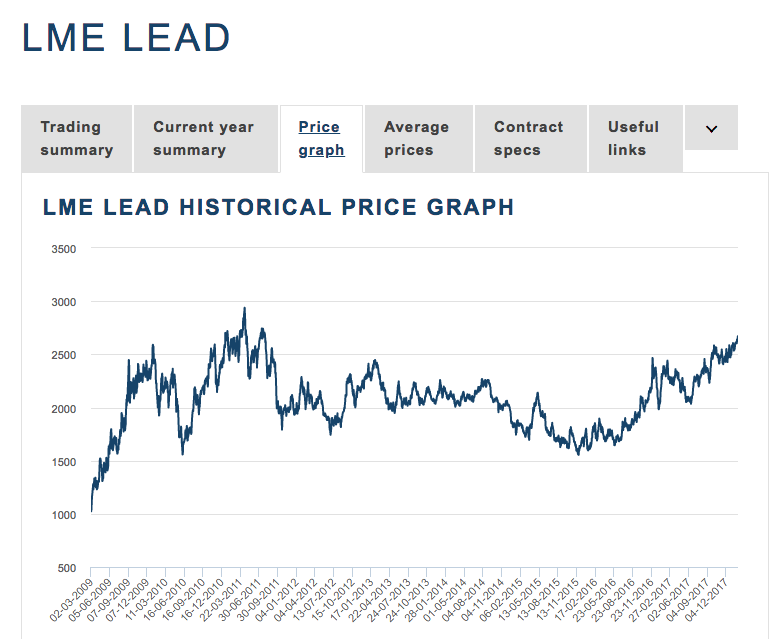

@DEEPAKSINGH - Lead at fresh 7 year high and seems to have broken out of that 2600 level which was a bit of a resistance. 2670 today and can possibly make an all-time high in 2018. I think Gravita is a better stock than Nile/Pondy Oxides purely based on capacities. I remember doing the research sometime early last year when I invested in Gravita. I don’t know if that situation has changed now.

Thanks phreak…thats y i raise question lead looking extremely bullish and now stocks are gettig at attractive levels after hammering.

On Copper / Hind Copper:

Hindalco posted decent numbers propelled by performance of copper. “Copper segment revenue shot up 40 percent to Rs 5,701 crore compared to year-ago quarter, with EBIT rising 27.6 percent to Rs 420.6 crore YoY.” I couldn’t check how much of this is volume versus realization growth. But could signal that Hind Copper will post strong numbers for Q3.

Goldman’s new forcast for crude oil is $82.5; Which company in India is likely to be a key beneficiary of this. ONGC for sure is one however given the election heavy period for next 12-15 months, it might have to share the subsidy burdon. Is there a player in oil exploration space which have either already increased or plan to increase the crude oil output and does not have subsidy strings attached? Would appreciate suggestion/ideas!

Its results are already out. Underperformed considerably.

Selan Exploration is one. Though a small cap.

Are you still holding investments in Godavari Power and Prakash? Results r good but not sure if to add more at present fall.

First of all i would like to thank Jiten for providing a alternate way of value investing and laying out a decent approach for the same. Cyclical businesses if followed proactively and nibbling into them when things are gloomy and pessimistic can handsomely reward the contrarian investor. He has already highlighted couple of such business like cement, steel, paper, and most of the commodity linked stocks. But lot of people in the forum are making this thread a stock and subsequently price discussion forum. it would be better if we all come up with our observations on the topic and learn long term out of this thread.

regards

divyansh

What do you think about sugar stocks now? PE is at around 5 for some and the stocks are available at 50% of their 52 week high. They have a high dividend yield as well. Based on the cycle are they a good buy now?

I have said earlier too. I have long back exited all sugar stocks.

I will buy them at high PE or losses. Do read my presentation, why I say so,

Yes. I think we should discuss processes, cycles, and not individual stocks.

Thanks Jiten. I have read your presentation and do follow all your messages like a hawk. I asked this because the sugar stocks have fallen 50% from their top and also it is not that easy to follow this contrarian approach in commodity cycle (else everyone would do it). That’s what makes your suggestions exceptional!

Is there any commodity near the bottom of their cycle worth entering at this moment?

Investing books tell us that the biggest cycle in I investing is the I interest rate cycle. Does anybody have a view on the turnaround in this cycle…With interest rates poised to go up in India and US too.

The second most important cycle for Indian economy is the oil cycle. Many analysts are of the view that crude may rise to 80 usd

interesting read: https://www.bloomberg.com/news/articles/2018-02-04/how-spiking-bond-yields-really-could-topple-a-stock-market-rally

China had extended it’s shutdowns till May. I think steel cycle had got additional tailwinds. Your process and selection had benefitted all vp members. Thank you for creating the thread and guiding in each cycle.

Detailed investor presentation by Hindustan Copper providing more clarity on their expansion plan for - 3-4x capacity.

Disc - Invested

Looks good on paper. Typical PSU presentation.with poor quality photo copy. Can they not arrange a good PP presentation.