India’s steel demand potential…

Since there isn’t a board for Hind Copper, am posting this here. Kendadih mine is re-opened and this would add 2.25 lakh MT capacity. This mine has been closed since 2000 apparently and the favourable economic conditions have made the company re-open this mine.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/e03ac425-c7fe-4a4b-b23a-c141b7e0b3fe.pdf

3 Likes

I am reading “Value Investing and Behaviour Finance” by Parag Parikh and found chapter on Commodity Investing very interesting and relevant. Points which I like to highlight:

- The Paradox: Conventional thinking does not hold true

When one is looking at returns to be made from investing in a commodity stock, the conventional wisdom of investing on sound financial parameters does not hold true. - Efficient and low cost producers are least benefited during upcycle and high-cost producers and heavy debt companies will be able to give higher returns to investors. Reasons for this are:

• Low-Base Effect

• Debt reduction and decline in interest burden

• Re-rating

• Lower taxes because of the loss in down cycles.

Author has tested above principle with share price comparison of Steel and Cement companies during 2003 to 2006 cycles

I would suggest to read this book especially chapter on Commodity Investing

18 Likes

Very relevant points. Haven’t read the book, but that is also my exact

inference.

1 Like

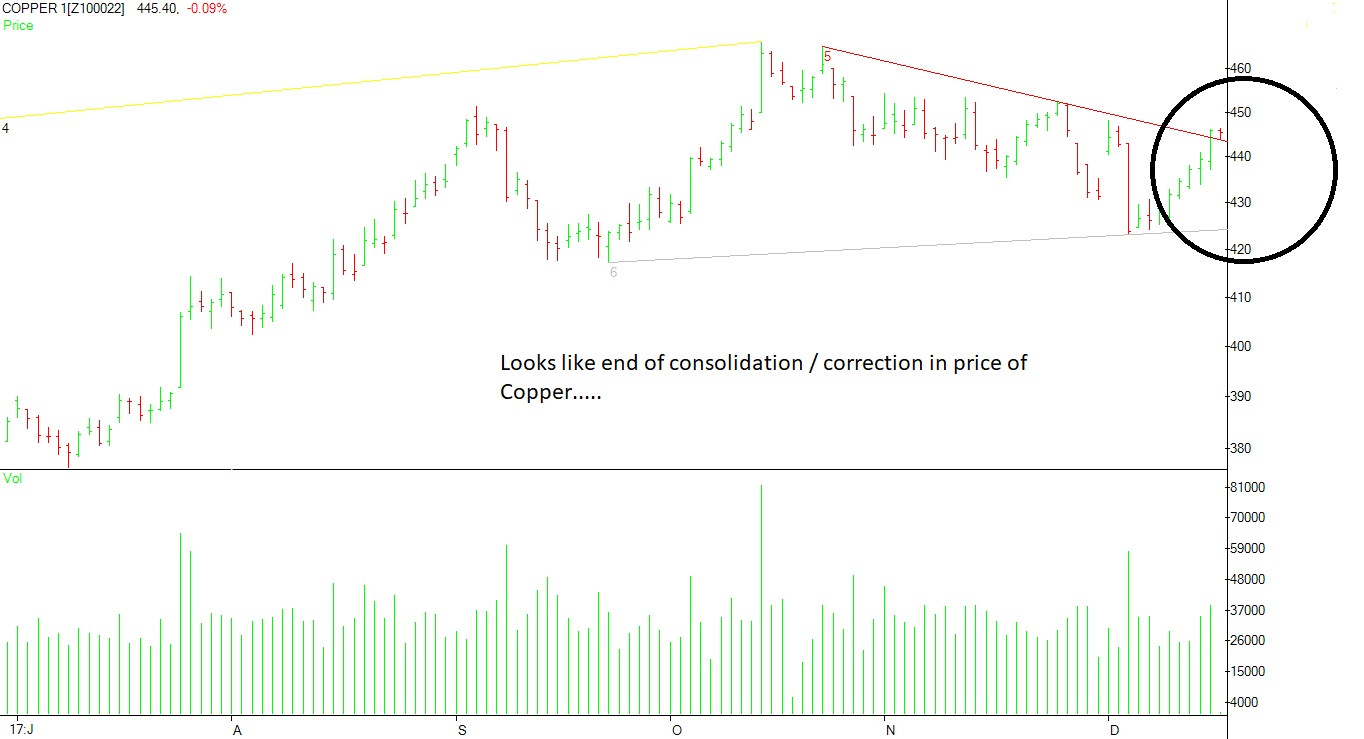

Goldman Sachs is Extremely Bullish on certain Commodities including Copper in times to come…

What is so great about GPIL Jiten. If you can elaborate please as u must know about it thoroughly since it is the largest exposure for u in the metal space.

@jitenp are you tracking Beekay Steel? Just reported a 200% jump in profits on 25% jump in sales. Trying to figure out how long will this cycle last. Company is a manufacturer of Sections, Bright Bars, Structurals, TMT Bars, Coil Springs etc.

1 Like

Since cotton prices are expected to trade higher,won’t that hurt the margin of textiles further

HI, Jiten,

Are you tracking Asahpura Minechem, Bentonite Major in india. What is your view on medium term.

Disclosure: No holding

Ashapura is extremely bullish on long term charts…something is going on there

2 Likes

Ashapura minechem , One of the Promotor sold 10% and Porinju’s equity intel baught 5%. Quite confusing signal. Really no idea for business tailwind, upcycle, seeking help from the VPmembers

Disclosure : Not invested

not tracking Beekay Steel. Planning to have a look at it.

yes. that’s a short term negative for them (reflected in stock prices). And, as I mentioned it’s a contra play. Will add to these over time, when I see cycle turn around.

1 Like

It’s a turnaround deleveraging story. Which has played out beautifully.

Thank you Jiten, Can you spell your rationale for investment in Ashapura minchem, Why do you think they will do better in future barring one off loss due to contingent liability.Just to increase my understanding about the stock and learn from you.

Hi Jiten, In the same space of ICIL, Sintex Ind what is your opinion on Trident as they have just completed their major CAPEX.