@phreakv6 , Thanks for the insightful reply and its always great to read your answers for understanding important valuation parameters and business models of quality businesses . Even i am planning to add Havells to the portfolio but was waiting for a correction as valuation seems pricey at the moment. Thanks for the HDFC Life update . All the companies in the list seem to have great runaways, IMHO Pidilite seems to be an ideal coffee can candidate . Eicher i added partial position . Is havells ok to br bought partially at current levels ?

Disc : invested in pidilite and Eicher and hold small tracking position in page.

thanks for the beautiful post.

Agree to you fully that if there is high ROCE ,even high PE multiple will still hold ground; there might be some time bound correction, but they will recover their glory in 3-4 quarters;

Curious to know if you have analysed between USL,UBL and Radico Khaitan: which one seems to be a better bet? USL past fundamentals look haywire, UBL look great but am scared of the promoter Mallya

Isn’t Mallaya only a minority shareholder in UBL now,?

Can u pls elaborate this thought? What do u mean by lower long tail risk for general insurance as compared to life?

1 Like

@Investor_No_1 long tail risk refers to concepts where tails are fat unlike a normal distribution where tails are thin . So chances of extreme event losses are low but if such events happen, the quantum of losses would be very huge and significant . The current world financial scenario follows more of fat tailed distribution as opposed to normal distribution. You may refer to the fat tailed distribution concept propounded by nassim taleb . What @phreakv6 says is , In general insurance the risk of uncertainty of huge loss is normally quite less compared to life business although life insurance business uncertainty risk may be less in India compared to world average due to young population and long runway .

https://www.quora.com/Why-does-Nassim-Nicholas-Taleb-hate-bell-curves

5 Likes

I am a believer of insurance companies for long term. I chose life over general as risk of underwriting losses in life seems lower as compared to general say crop, fire, natural disasters etc. Also in general my thinking goes like this that chances of a life insurance company going bust and bankrupt is little lower as compared to a general insurance company over long term…however some points are making me think more like I read that percent of retail individual life Insurancein US is at its lowest level in a decade and that there is need for US life insurers to really reinvent their products etc. Because traditional policies are not selling…so on one hand a motor and house insurance becomes a necessity like oxygen to US ppl while life is something they chose to skip and even the government don’t mind…in these respect then post the blah blah of underpenetration in India what is the future of life insurance…ULIPs are no longer charm, protection is for next few years…what next? Insurance is not a compulsion, not a perceived necessity…how do I ensure the machine keeps compounding for multidecades…really need insights on how in US and Europe where life insurance business is century old has evolved…

1 Like

First of all thank you so much for wonderfully explaining the concept of fat tail etc.! Regarding above statement, I think exactly opposite…in case of general the chances of huge losses are more due to various disaster events…in case of life as well there is event risk but seems little less than general. For US ppl where population is old means if that person had taken insurance when young, he must have already paid sufficient premium to neutralize the payout in case of a natural claim…so runway less or more may not affect profit/loss if underwriting was done sensibly…but yes event risk is something to understand that is that more for general or for life…

1 Like

“chance of life insurance going bust very low”

You would like to check history buddy. Look at USA, Europe, China, Japan in last 30-40 years, whether life insurance did well or general. Frankly, I find life insurance bit difficult to understand n predict . @rupeshtatiya n @Anant had done some amazing work on life insurance (available deck on VP ) , I did a small piece researching history of life insurance companies across the globe n it looked scary for the right reasons. Check the deck n all the links on same . It’s in VP Goa Chintan baithak. Will attach it down. To me, general n specially health insurance looked best among all on generic basis n also based on historic research

6 Likes

Yes Pidilite as well is a great company, along with Asian Paints. There are probably just around 15-20 businesses that you can buy and hold for decades and these two definitely qualify. These type of businesses will remain expensive though as they are businesses with long runway, that make money from millions of customers on a day-to-day basis with strong managements and brands and some of them have been around for decades selling products that are hard to disrupt and if you believe in Lindy effect - these products will be around for a long time as well. Havells I believe can be bought at current levels but just like you, I am also waiting for some sort of random volatility/correction to make an entry so it wouldn’t be right on my part to say current levels are a safe. When it comes to the wealth protection part of the portfolio, I am extremely cautious and selective.

I havent looked at USL and Radico in depth but I suspect the recent gross margin expansion could be due to depressed ENA prices (sugarcane overproduction). I like UBL because I think for a hot tropical country with a young population like ours, the market is better for beer than hard liquor. I see good improvement in working capital lately (last 3-4 years) and I like that they are introducing new premium products (like KF Storm, KF Ultra Max, Amstel) and they have pretty stable gross margins as well.

Long tail risk in general insurance arises in a few select segments - like third-party motor insurance and health claims related to occupation and these can be small parts of the whole business (bulk of general insurance business is in motor, health, property, crop etc. which are short-tail where claims are paid in the period of policy) but in Life, over the long-term there is significant interest rate risk - like long periods of subdued interest rates where the float earns significantly less since there are restrictions on how much can be invested in equity (15% in India). These periods of subdued interest rates could also make these policies unattractive thereby decreasing new policies making it a double whammy.

So what looks to be going well for a long time in terms of underwriting profits could take a sudden significant hit for extended periods in a depressed interest rate environment. So long-tail risk that I meant is not in terms of claims but in terms of risks arising in the environment over long periods that impact profitability. Not sure if I have explained myself well here. As @suru27 mentioned, life insurance businesses in other countries aren’t nearly as profitable as general insurance so the base rate for success here isn’t in favour of the shareholder in such business. However, I believe that such risks will materialise only over the very long-term and in the intervening period, life insurance companies could be pretty good investments.

7 Likes

https://globalmeetwebinar.webcasts.com/viewer/event.jsp?ei=1238330&tp_key=177a5427a1

A publicly available webinar update from Marcellus. They talk about the difference between such stocks and the rest. They also talk about why they pay such prices.

For their clients they have bought these stocks at close to current prices. They talk a little bit about some of the stocks they own. (Asian paint, Berger paints, pidilite, page)

It was a good watch.

P.S it is about 1 hour long (this includes a Q&A)

3 Likes

@1.5cr - thank you for sharing the link! I went through the recorded webinar.

I apply CCP philosophy to a portion of my portfolio. But I put a lot of weight on my entry valuation. In short - Quality growth at reasonable price. We all know how your entry valuation would impact ending CAGR.

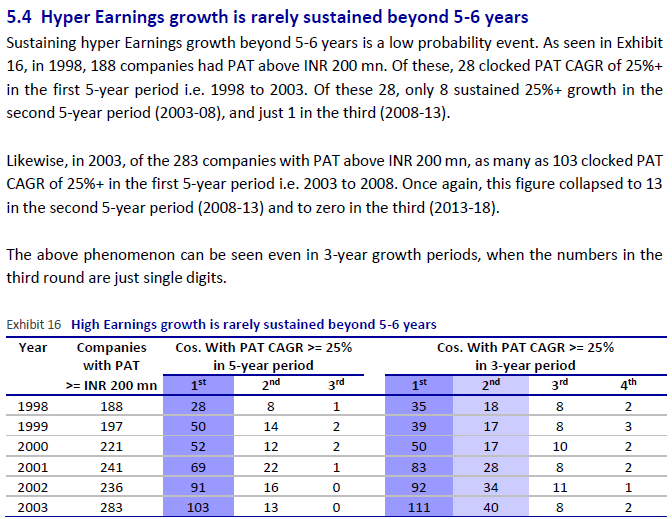

These guys own Asian Paints, Berger, Pidilite, Bajaj Finance, Page etc (each available at north of 60 PE). There is no doubt that these are fabulous businesses and these businesses might do well in future too. They believe that these businesses would deliver ~25% CAGR earnings growth in future (on top of giving 25%+ earnings growth in last many years). But the big question is will earning growth of 25%+ continue in future? Below screenshot from Motilal’s 23rd Wealth Creation Study would provide some insights:

The biggest takeaway for me from this study is that there has been not a single business that has been able to clock 25%+ earnings CAGR for 15 years since 2002. It’s simple concept of ‘law of large numbers’. Above shared findings prove this concept.

The biggest shut off for me was how Mr. Ranjan answered to a question on what returns should investors expect in their PMS. He confidently said expectations are of 21-25% CAGR return. And this return should be achievable in only 3 years and investors don’t have to wait 10 years for such CAGR return. How on this earth can one be so confident that 21-25% CAGR returns can be achieved in next 3 years? As we know in stock markets - it takes only few seconds for sentiment lights to flip to amber/red from green. No wonder Buffett said that forecasts tells great deal about the forecaster and not tell anything about the future.

I see shades of “nifty fifty” stocks from 1970s in above stocks trading at 65+ PE. Problem is not with the business, but with the insanity of institutional money managers proving again that stupidity well-packaged can sound like wisdom and promising investors of 25%+ CAGR for 10 year in such expensive CCP portfolio. We all know how things ended with nifty fifty stocks.

Disc: not holding any of the above mentioned stocks except Bajaj Finance which I have been holding since 2014. Things looked very expensive around highs of 2017 and exited then. Re-entered in 2018 October drop and now holding it as part of CCP portfolio.

23 Likes

Where can one find curent portfolio of Marcellus ?

1 Like

They hold around 12 stocks. Out of these Bajaj Finance, HDFC Bank, Asian Paints, Berger, Pidilite, Nestle, ITC, Page Industries, Relaxo and Cera Sanitary are known. This comes out to be 10 stocks out of the 12 which they hold.

7 Likes

@phreakv6

Does dmart seem to be a coffee can portfolio candidate considering its long runway and execution capabilities apart from low cost advantage ?

Thanks

Dmart is planning QIP in near future & promoter holding has to be brought below 75%. Post these events we can expect stabilization & could be good bet for coffee can type of long term investing method.

I recall earlier attempt by promoters to offload hardly 1% shares & big knee jerk reaction was seen in prices. When they plan to bring it below 75% (almost 7% offload), it will certainly have major reaction… may be short term but I feel its always better to wait for such events to pass by before making really long term investments.

Views of other boarders are welcome

4 Likes

Marico, TCS and Dr Lal Path is latest addition.

3 Likes

Not much has been spoken about ITC as a candidate on this thread. So I have added a small brief thesis on them. They can be a solid addition to a coffee can portfolio.

ITC

-30x for a business with such free cash flows and return metrics. The ability to build household brands. I think we are paying a reasonable, if not an attractive price for such a business. At 30x free cash flow and a 1.7% div. yield downside seems limited. And upside over a 10 year horizon seems very decent.

-

The FMCG business will turn around once Mgmt. slows down investments and slows down trying to cover white spaces. I think they will shift focus to profitability soon. Operating leverage will slowly kick in and margins should begin to inch up.

-

Anyway at this valuation it is like paying for the cigarette business alone. Disruptions can occur from vapourisers etc: but I think that is quite far out and ITC had also started thier own vapouriser but there is blanket ban in India and in many other countries on the product due to safety concerns and health concerns (correct me if im wrong). Based on what I’ve heard I understand that cigarettes have a different appeal compared to vapourisers.

-

Vapourisers could actually be a better opportunity for ITC as they can provide them at cheaper prices compared to the others in the market and also brand them nicely since there is no law on them like cigarettes. Further the catridges have to be refilled giving them a recurring source of revenue.

-

Tax issues are there on the core cigarette business but the govt. will always have a quid pro quo as cigarettes are a cash cow for the government as well. So they wont hit the industry too hard. Plus there should be a gradual shift from beedi and other tobacco forms to cigarettes as income and awareness grows in India.

-

The free cash generation should improve as the FMCG business hits profitability and contributes to earnings. Moreover, the core cash cow cigarette business should continue a single digit growth in terms of volumes for a long time. You can see the strong pricing power that ITC has in the cigarette space over the last few years inspite of adverse tax conditions and volume issues.

-

Mgmt. is ambitious as well and want to take the FMCG business to 1L cr from current ~11kcr in 10 years. Even achieving half of that with industry standard margins would great for investors. Further they may venture into new spaces as well (rumours of entering the hospital space). With a 10 year view I think this could give index beating returns along with a good dividend payout.

6 Likes

We should not wish that if we are long term investors. We want to be invested in stories which continues to find reinvestment avenues. There are not many. We should not worry too much about margins of these businesses in initial phase.