Annual report is still not available for current year but came across this very detailed research report from crisil. have a read and feel free to make comments.

Disc-Invested

Crisil-Report-on-CMI-limited.pdf (776.0 KB)

Annual report is still not available for current year but came across this very detailed research report from crisil. have a read and feel free to make comments.

Disc-Invested

Crisil-Report-on-CMI-limited.pdf (776.0 KB)

Why AR still not available are they are not obligated to provide AR by some stipulate time? And AGM is in December, did they taken special permission for that, I always wondering management quality in this company. Anybody knows company well let me know what is the issue with AR and annual report?

There is a notifiction that general meeting will be delayed by 2 months … Any idea about this …

They had same problem last year too, released it somewhere around December 26th or so, told the reason was because of amalgamation on Cmi Ltd and Cmi baddi plant, they were waiting for the approval, which dint got on time as per their expectation

Any reason why there is steep fall in price or just market hammer any change in fundamental of company

Does any one has concall for today’s meething?

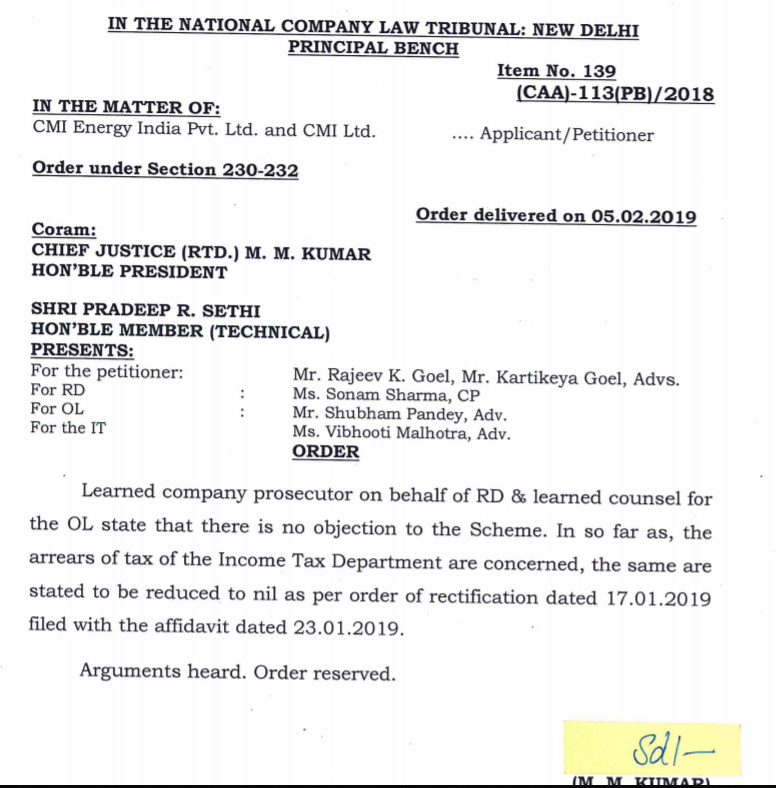

Merger of CMI with acquired subsidiary is nearing completion. Order reserved by NCLT Principal Bench on 5 Feb 2019.

Several developments at CMI recently so I thought it will be useful to write up a quick summary:

Disc. Invested.

Merger of CMI with acquired subsidiary approved by NCLT yesterday.

ref: http://www.cmilimited.in/img/pdf/Press%2028-02-2019.pdf

Apart from this, technically it looks like a good opportunity to buy this gem at almost all time low.

Disclaimer: Was lightly invested; have already added more before sharing the view. Therefore, you are free to consider this a biased opinion.

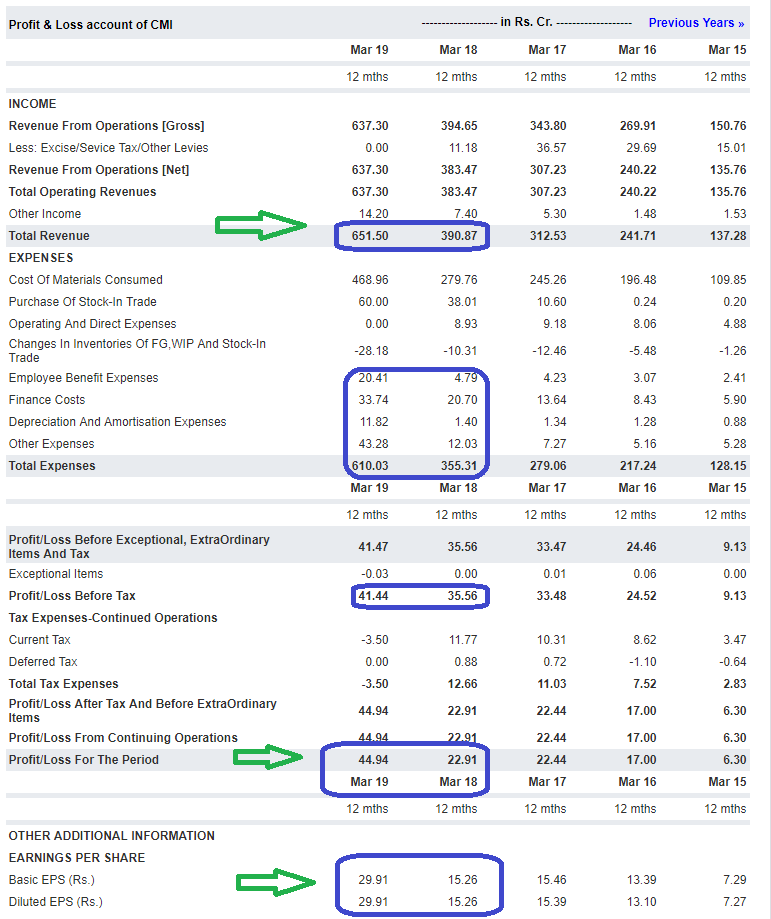

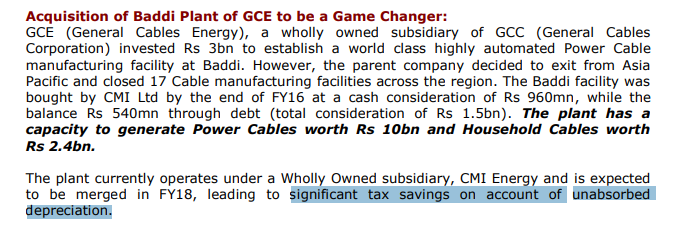

Benefit coming mainly from tax saving.

Yes, but that is a benefit. Isn’t it?

As per my understanding, this is due to Unabsorbed Depreciation related to Baddi plant.

Apart from this,

Enough red flags in the company.

One good part about the company rather two -

any update why cmi is falling like this looking at the stock movement it looks like it is heading towards penny stock any specific reason for such a big fall?

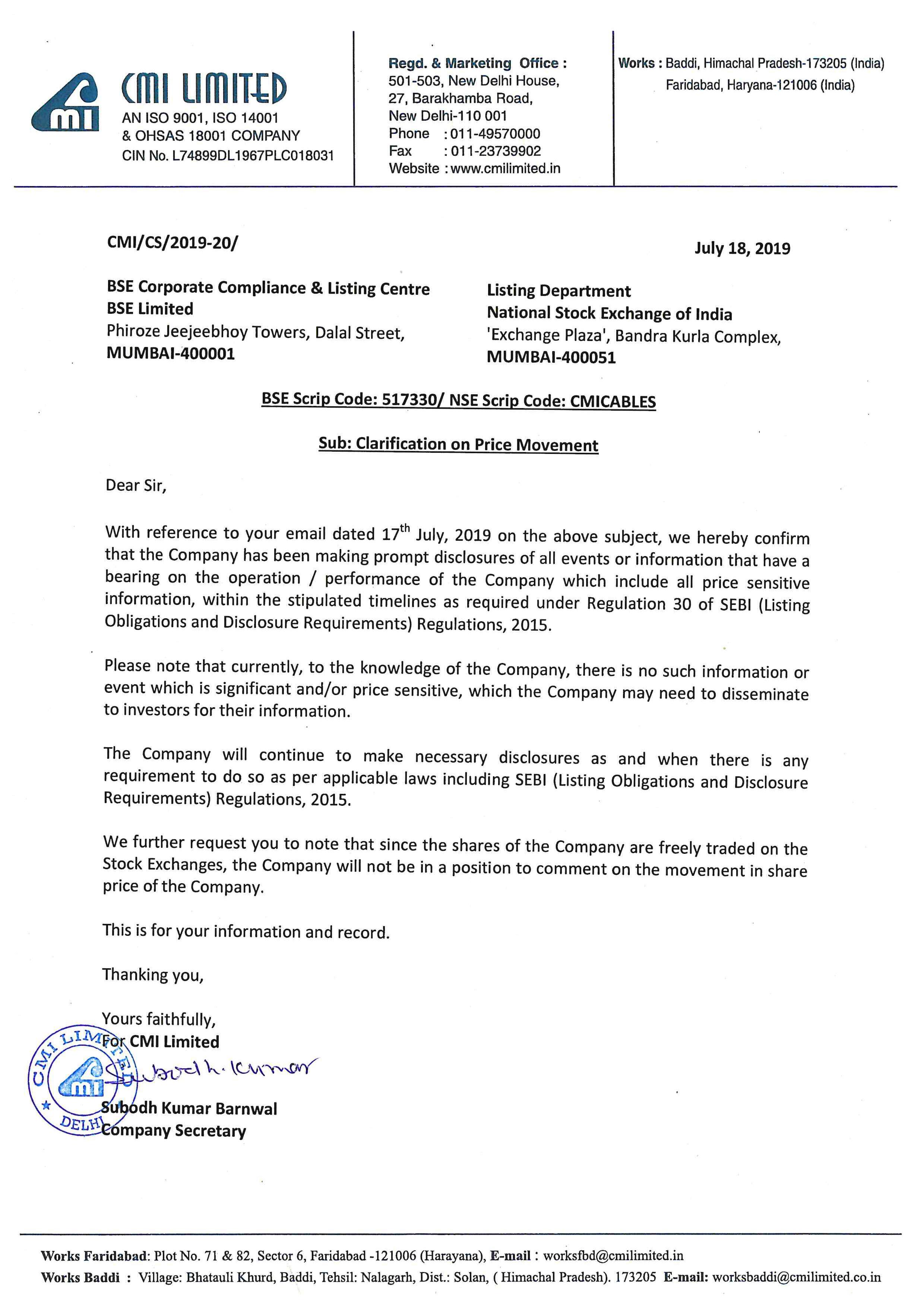

I have sought clarification, will update here once I hear back.

Very surprised by the sell off. Have been holding a large quantity for over 2 years and have not heard any news recently. Could be GMO and HSBC funds selling off coupled with low liquidity, their holdings have dropped in recent quarters. I have also written to the company for a clarification and awaiting their response.

Its GMO who is selling, rather dumping.

GMO sold 226,000 shares in Q4 FY19 and HSBC sold 10,000 shares.

GMO still holds 1,200,000 shares which is 8% of the total share capital.

No point asking for clarification from the company. GMO buys & sells in this haphazard manner. It impacts the price.

Business has no change IMO.

Look at Asian Granito where GMO had a sizeable stake. It nosedived to 130 per share. Post their exit, the stock swiftly came back and made a high of around 250.

Clarification - “Currently, to the knowledge of the Company, there is no such information or

event which is significant and/or price sensitive.”

Source:

Many companies may soon issue such clarification in view of pre diwali monsoon dhamaka sale.

Has no relevance.