Board of Directors at their meeting held on 29.05.2019 have recommended a final dividend of Rs.0.48 (24%) per equity share of face value of Re.2/- each for the financial year ended on 31.03.2019, which shall be paid within 30 days from the conclusion of the ensuing Annual General Meeting, subject to approval of shareholders of the Company.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aebef8fc-b56a-4e5d-a1b9-06fee6bc474a.pdf

However I have found that From 30-Nov 2015 to 15 May 2018 There are 130 Entries of insider transaction and surprisingly they all are disposal … IS n’t IT STRANGE

Source : Chaman Lal Setia Exports Ltd. - Disclosures under Insider Trades & Substantial Acquisition of Shares and Takeovers

Disc : Invested

Did anyone attend the conference call on the 7th? Please do share updates.

Curious about the gross margin drop in 4Q and the reasons for the deteriorating working capital cycle.

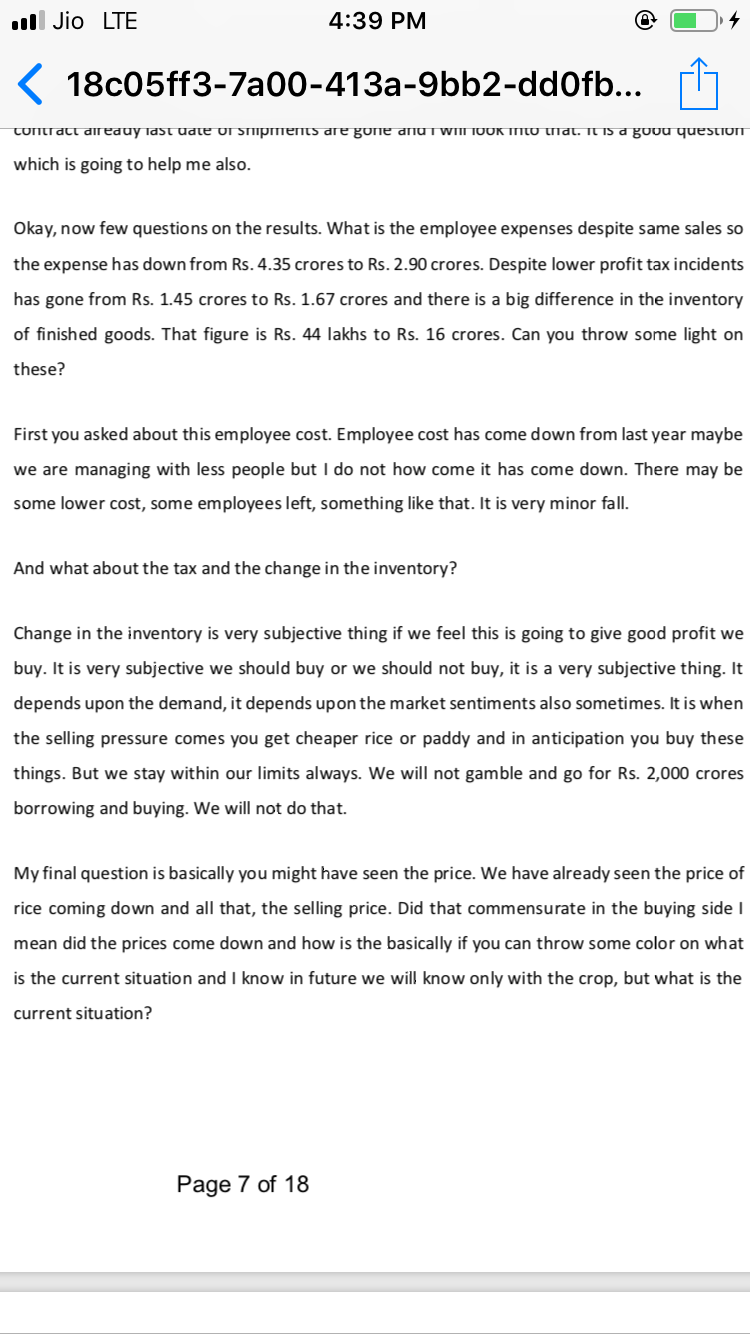

Extract from company’s Concall … Promoter not even aware about employee cost ? In opening remark focusing so much on Investors that never cheated and all (first time seeing such opening remarks, Any fear). Net Profit for the quarter- Rs. 3 Crore & decrease in employee cost by 1.45 cr as compared to last year & as per management “it is very minor fall” & “but i don’t know how it has come down”

latest filing by company

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f7e6cd96-00fb-41e9-a8ea-33764d9e5364.pdf

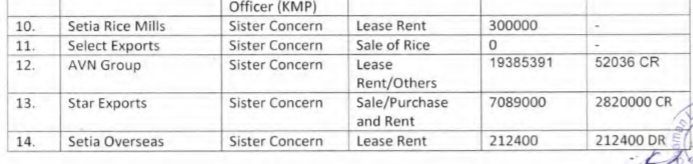

it is showing the company has taken money from the promotors thus paying the interest on that

also they have taken premises on leasing from related party

but i coundn’t find name of these sister companies on https://www.zaubacorp.com

i found some information on zauba some snip below

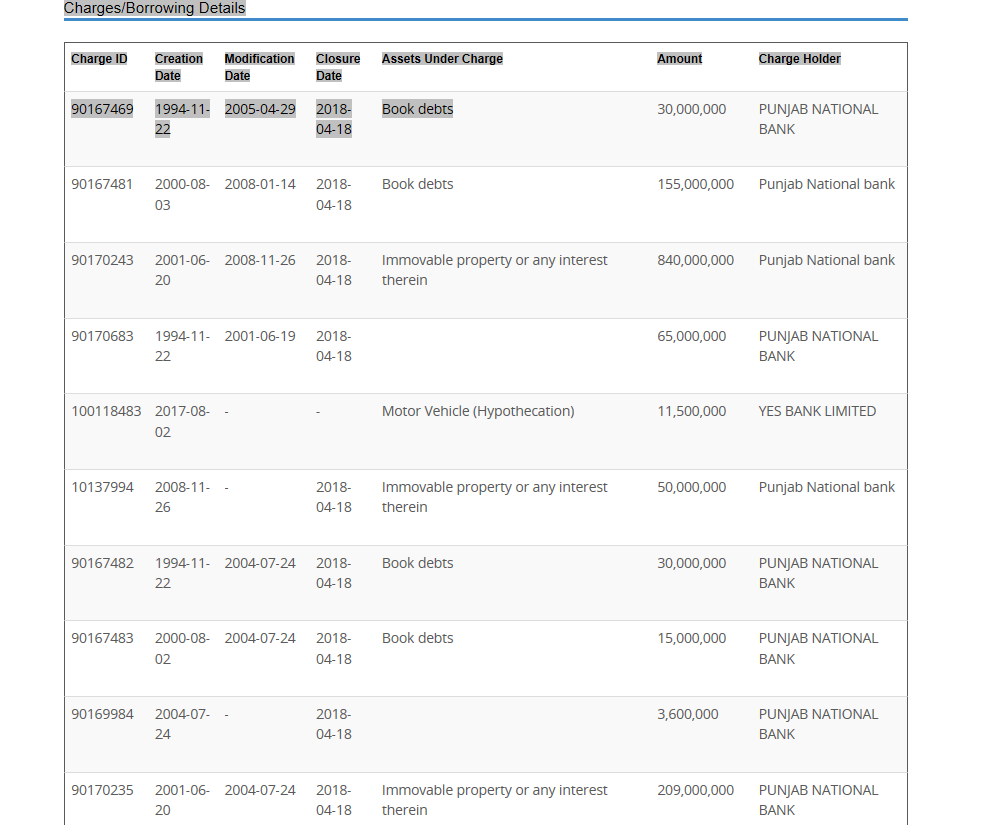

Could someone help me to understand these … ARE THESE CAHREGES PAID or STILL under DEBt HEAD ???

isn’t these are RED Flags …

Disc invested

Does anybody have any idea what’s going on that is leading to the continuing rout in share price? Cannot be fundamentals!

This is the reason.

No new order from Iran. Market very weak for Basmati

result analysis

Update regarding Credit rating

http://www.careratings.com/upload/CompanyFiles/PR/Chaman%20Lal%20Setia%20Exports%20Limited-08-14-2019.pdf

The results are not good. Rice prices went to supernormal ast quarter then also they were not able to generate good margin. May be they already sold inventory before the price went up on advance contracts.

Discl: Invested .

CLS is Creating bigger playfield to play

This company for the last few trading sessions or even for some time now is taking a severe beating without any credible reasons, atleast the common investor is unaware of. CRISIL in its rating report says the rating is withdrawn from the previous rating of Stable but non co-operating. CARE has always been maintaining a good rating . The AGM is on 28th Sept. If anybody is attending, request for their feedback.

could you please share the AGM Notice I didn’t received

Dec Qtr result out —>

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9a4dab1e-969e-4381-9ab7-7046f9beee8c.pdf Net profit increased from 8.85 to 16.56 Crs ( i.e 87.11 % ) which is not digestible under constrained conditioned so when one look in details and if one is taken out other income of 6.01 ( not explanation is provided ) i assume it may be single time than the Profit i only raise from 8.85 to 10.50 18.56% that is also not too bad .

note 4 of Qrt filing is as below

in plain reading of above what i made from it either the company has pre-charge the taxes or made some surplus pool to offset the tax rise with will be due on 31-03-2020 but i may be wrong may i request @ayushmit could you please help me to understand the above.

Disc ; Invested

Regards

This qtr results look to be much better than earlier quarterly run rates. One needs clarity on other income though.

The higher tax rate should logically get reversed in Q4FY20.

The valuations look very cheapThe stock is trading at 4 p/e.Not to mention it is less than 3/4 the working capital.Wonder what is going on here.The stock has corrected from it’s peak of 210 to 28 now without actually anything changing in terms of fundamentals.

Anyone else following the stock?

Yes @ gothamcapital

I think mcap at measly 140 crs which is 2/3 rd of working capital as you said warrants it for a worthy buy . Huge promoter stake , regular dividends ,tax all support to this thesis . It’s tempting and I probably might get into this if I can arrange for funds from somewhere

Well,according to KRBL management the Q1 2021 will be tough for basmati exporters.Also the price of rice has gone down.Seems like the margins may contract.But still the stock is at a discount very similar to the paper stocks like seshasayee papers,shreyans industries etc.