I guess u r right, they seem to be pumping revenue by trading in volumes of lower margin basmati or even non basmati rice.

From last yr AR I could see that majority of staff cost is salary of promoter directors, so spike in staff cost in the quarter may be promoters showering them with gold, else can’t understand the sharp yoy jump in Q2 staff cost, shall be clear only when This yr AR comes out…not a great sign though

Not a good sign

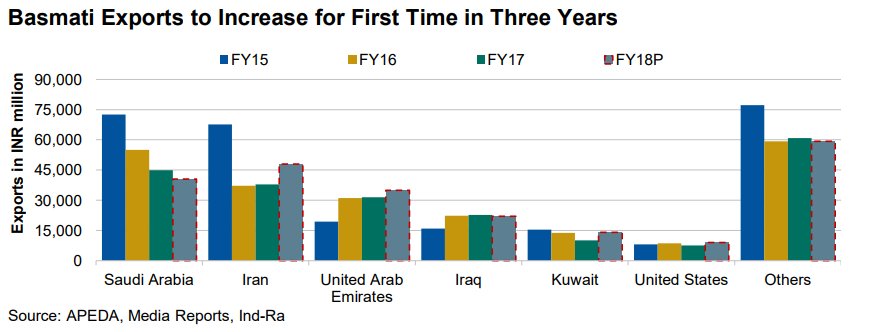

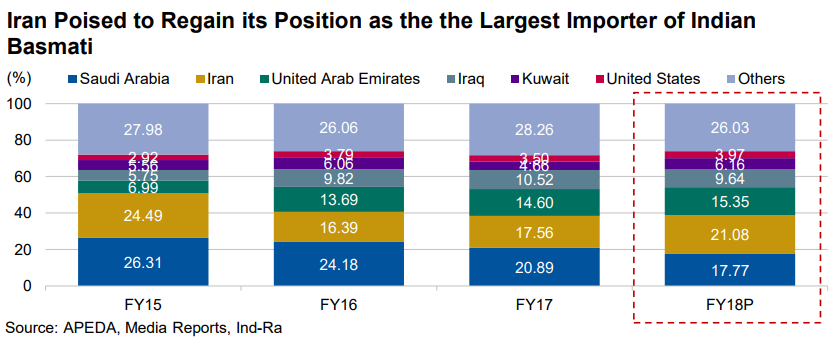

Basmati prices rise on higher demand from West Asia

Higher demand for basmati from Iran and West Asia is helping farmers in Punjab and Haryana get good price for their produce this year.

Although the area under paddy cultivation fell nearly 10 per cent from the previous kharif season, arrivals at grain markets have been healthy, say traders and mandi officials at Fatehabad and Karnal.

Crops are like babies. They have very specific requirements growing up, viz temperature, pH, moisture etc. Rice in this case is so finicky that they want abundant water in the sowing season but will not tolerate water once the crop matures.

Rice is susceptible to water logging in the harvesting season. The recent rains in parts of India have been detrimental, as this is the cutting season of rice.

Water logging saturates sub-soil, suffocating plant roots. It also creates very conducive conditions for pests and microbes to thrive, effectively washing away whatever pesticide, insecticide has been sprayed upon the crops.

Hi, thanks for the data. You can check icra n care reports also. ICRA highlighted change in trend in mar’17. Also, little difficult as they keep changing website but ministry to commerce shares export data on monthly basis. I did during June n oct’17 n it shows 30 percent price CAGR export growth for basmati rice .so, multiple venues to validate n track story. Will try to find latest working link for export data n post

So, the Promoter has a good amount of cash in his hand (I am not talking about the Cash & Bank Balance in the company). He wants to make money out of it. So, he loans the money to his company and gets around 15% interest - Directors’ Deposits increased from 16.99 cr (FY16) to 31.53 cr (FY17). If he gets the money from the Bank (for the Company), the interest cost will be much lower. Why would he do that?? Irony is there is already around 63 cr Cash & Bank Balance in the company (according to Sep’17 Balance Sheet)

Added to that, he is not even giving out proper dividends. Just around 6% Dividend Payout Ratio. Any news regarding capacity addition??

Couple of points to note. Though the company grows faster, they are doing it in lieu of the cash for the sales. They are not collecting the cash for the sale of goods.

Their Cumulative PAT (CPAT) for last 10 years is 154.62 Cr. Whereas their Cumulative Cashflow From Operations (CCFO) stands 57.15 Cr which is just 36.96 % of the CPAT.

Irony is that they give dividends too funded from debt which you would not want it to be doing.

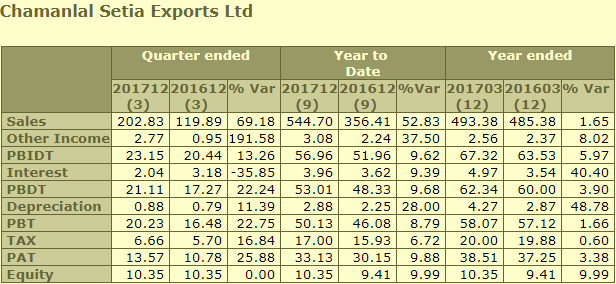

Good to see the good top-line growth in recent quarters after sort of flat revenues over last 3-4 years. Though to be fair, the company was growing earlier till 2016 (annual report of 2016 mentioned about 27% increase in quantity sold and there was consistent increase in exports before that), however it was not showing up due to fall in prices of basmati rice. But now the same is getting reflecting as the prices have increased.

The interesting thing is the net cash on balance sheet unlike the peers:

Hi Ayush, Thanks for the post. I guess the improvement in margins is on account of 1.) Increasing Basmati prices 2.) Finding new export geographies with good realizations. The management pays a lot of emphasis on “Branding” in their annual reports. Is there any traction on the ground in terms of domestic penetration through “Maharani” brand? Will the company benefit from ongoing broader theme of migration from unorganized to organized? They have deleveraged balance sheet, good cash balance and better receivables days than peers; however, higher inventory holdings leading to negative free cash flows. But cash +inventory looks better…what could be the growth triggers going ahead? In terms of valuations, the stock appears not very unfavorably priced compared to peers but can this be supported by earnings growth?

@ayushmit I always get confused by their stock in trade and inventory change numbers in P&L. Can you throw mode light there ? My understanding is promoter being head of association leverages on some price based info and tries to buy in bulk when time is right . Also from last 7-8 years data, it looks nice plays in 2-3 year cycle , so, unless they become brand ( they do not look like investing in brand at least in India , need to check this year AR), how do you see from holding perspective when you know it has high chances to underpeform n outperform in cycles of 2-3 years.

@ranjank - in ref to your points…i think the margins have fallen rather than risen. Plz look at their revenue breakup for last few years - they have grown due to traction in exports rather than domestic market. Hence I think its wrong to compare it with industry leaders like KRBL etc. Good thing is that they are trying to export to markets which seem uncrowded (refer to earlier post by someone on VP itself)

@suru27 - i don’t agree with both of your observations that they are making money just due to inventory gains. Try plotting the value of inventory they hold vs peers and it seems they have the lowest inventory