Cost of acquisition is provided by the company for the purpose of computing capital gains.Your purchase cost is to be apportioned in the ratio provided so that arrived cost reflects your cost for the respective demerged entity

Where can we get the financial statements of the individual entities?

I couldn’t find them in the scheme.

Hello fellow VP’ers,

I’m a newbie in investing and need help in some calculations. Really appreciate your work in this regard.

Stock price of CESC: 722 (20th Dec Close as per Google)

Market cap of CESC: 9569 crores (20th Dec Close as per Google)

Number of shares of CESC = 9569 crores / 722 = 13.25 crores

The scheme allots 6 shares of Spencers’ Retail for every 10 shares of CESC.

This means, Number of shares of Spencers’ Retail = 0.6 * 13.25 crores = 7.95 crores (+another 5 lakh pref. shares assigned to CESC Ltd)

Similarly, Number of shares of CESC Ventures = 0.2 * 13.25 crores = 2.65 crores.

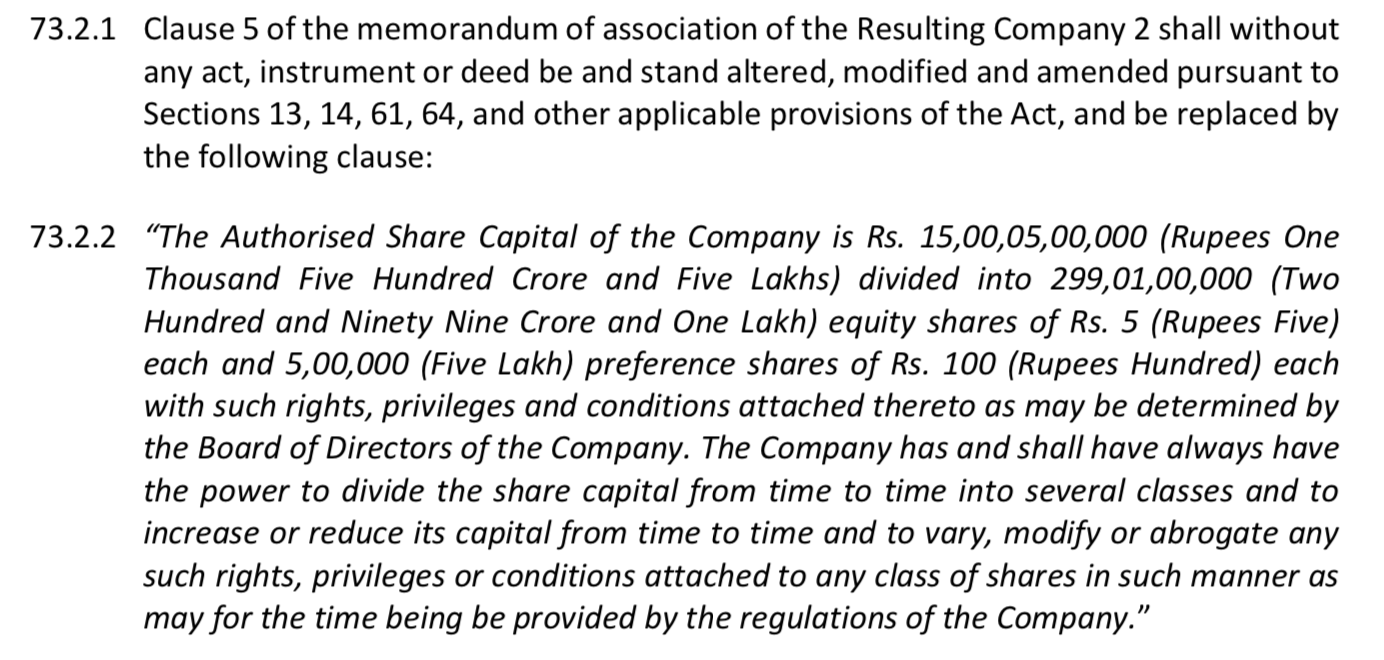

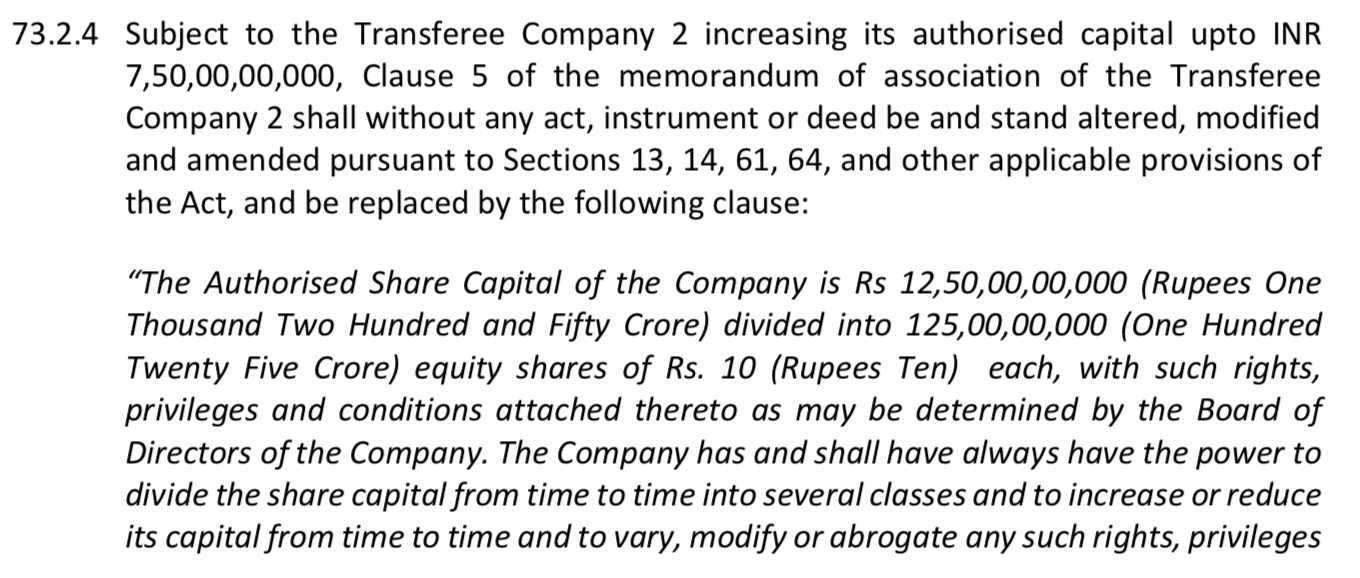

However, I see completely different numbers in the scheme. They say 299.01 crores shares (+another 5 lakh pref. shares) in Spencers’ and 125 crores shares in CESC Ventures.

Will really appreciate if someone can help me understand where my calculation is wrong.

Another question is that the scheme document doesn’t contain the financials of the spun-off companies. Is that expected? I couldn’t find it in FY18 annual report too. Where are you guys referring the financial data of the individual companies from? Found few articles on the web but I’m looking for an official source, which lays out all the numbers.

13.25 cr shares is Issued and paid-up capital, what you are referring to is the authorized capital, hence the difference.

Info memorandum is available on the respective websites of Spencer and Ventures.

1 Like

any idea if there is a time limit from a regulatory perspective for listing of demerged share? It has been more than 2 months now since the company split. Any pointers?

2 Likes

Finally some news on this , to list of January 25th

CLSA values the retail business at Rs 182 per share while it values CESC Ventures at Rs 141 per share as per a report post the demerger announcement. Nomura valued the retail business at Rs 93 per share while the balance business at Rs 143 per share. Citi had valued CESC ventures at Rs 130 per share and Spencer’s Retail at Rs 152 per share.

5 Likes

I can see CESCVENTURES and SPENCERS in my zerodha account, but not in ICICIdirect account.

Any idea? Why?

How will I be selling them at listing?

You will need to go to Equity > Transact > Demat Allocation > Allocate, and then you will be able to allocate the CESC Ventures and Spencers Retail shares for trading.

P.S. I tried doing the same a few minutes ago, but there is some issue with how the ISIN is mapped in ISec’s system. So the demat allocation did not go through for me at the moment. I have raised a complaint with ISec and they are looking into it.

Ya I went through this process. But it is giving the same error of ISIN mapping error.

I called up RM and customer care, but they were equally unaware of the situation.

Pathetic to know this thing happening with ICICIdirect. I sold my shares in Zerodha, but could not sell the ones in ICICIdirect.

@ajaymu

The issue seems to have been resolved and it has come to Demat Allocation. You can sell them now.

1 Like

Both demerged companies (Spencer retail & CESC ventures) are at continuous lower circuits since few days. Any particular reason for this ?

This is my first experience with de-mergers so any guidance would be useful.

Thanks

On examining the financial reports, I feel that a major chunk of money was coming in due to the electricity business.

Post demerger, this has become more transparent…

There has been lot of volatility in CESC Venture shares. There were continuous LCs (may be many of the MFs were exiting ) and now there have been series of UCs ( newbies trying to acquire based on FMCG story ) Can someone guesstimate the fair value of CESC Venture with the latest information available and in current market scenario?

- The 2 spin-offs (Spencer Retail & CESC Ventures) listed on Friday (25 Jan).

- They’ll be stuck in the low volume trade (T2T) segment for 10 trading days. Spencer hit 5% lower circuits for 8 days, while CESC Ventures did so on 7 days (but course corrected on day 7 itself and hit 5% UC thereon).

- Promoters hold 50% with large institutions holding ~30-35%, so none of those will get an exit. Day 7 for CESC Ventures was marked by high volume exits via bulk deals for institutions, which released the LC pressure on the stock.

- This is similar to the Solara Active Pharma spin-off which was also stuck in T2T lower circuits. It fell for a week, then an insti got out on day 7/8, after which the stock zoomed up.

- Spencer has improved to 2% Ebitda margin, from (-12%) 3-4 years ago. It has shut down many stores over 3 years, and CESC Ltd. took over its entire debt before Spencer was spun-off. Based on the Amazon-More deal, loss making grocery retailers are valued at ~1x sales. As such, Spencer’s EV could be Rs. 2000-2500 cr vs current Mcap/EV of Rs. 1,200 cr. The rumored Amazon deal valuation was Rs. 2,800 cr, but no one knows if the Amazon deal is still on. Spencer’s strategy is obviously still not as well calibrated as Dmart, but there’s definite operational improvement + growth. They also might’ve finally appointed a new CEO after 2 years. If Reliance Retail lists, then the whole retail sector (esp .grocery & Spencer) could get re-rated.

- CESC Ventures (EV ~Rs. 1,600 cr) basically holds 55% of First Source Solutions (mcap Rs. 3,288 cr, so holdings are worth ~Rs. 1,800 cr); a high-end mall (like Phoenix) in Kolkata & residential real estate in Haldia, WB (total real estate worth ~Rs. 500 cr); and the FMCG business (FY20 sales of Rs. 1,000 cr, worth Rs. 1,000-2,000 cr at 1-2x sales). So all in all, from an SOTP viewpoint, CESC Ventures offers greater investment value, however, it generally suffers from a lack of a clean structure as it could be subject to conglomerate discount as well as holdco discount.

13 Likes

Thanks for the post Mayur.

Are block deals public info? What is its source? It would be helpful if you can share it. Thank you!

Go to the moneycontrol desktop site and check the box on the right: “Action in Cesc ventures ltd”.

I don’t know see the sellers & buyers, but you can see that block deals happened on Jan 25 and Feb 1 for 2.25 and 2.2 lac shares.

Anyways, we can all see the higher volumes since that last LC which took the share down to 385.

1 Like

Spencers Retail is looking quite safe investment at current market cap of around 0.5x Sales. I have invested 3% of my portfolio in it in last few days and considering increasing this.I am not aware of any corporate governance issues with the group, there is no share pledging, no debts …so downside at current price looks quite limited.

I see short term issue of Mutual Funds or other entities exiting. Other thing which I am not able to find currently is what is management plan for Spencers Retail over next 3-5 years. Will appreciate if other members can highlight any potential risks or other factors that I should be considering for this investment.

Spencer’s Retail can turn out to be a good opportunity out of this demerger. Noticed couple of good things happening here:

- Improving profitability over the past few years

- Removal of Debt during the demerger

- Hired Walmart India COO as their new CEO

- Promoters bought 1.7% company from the market post-demerger

And it is available at cheap valuations of 0.5x sales.

One can relate to these points well, if he has read the book, “You can be a Stock Market Genius”.

However all of these points matter, only if reflected in the numbers.

They are indeed having couple of bad things to notice:

Lack of targeted customer segment.

Growing at a slow pace.

Strong competition like D-Mart.

Disclosure: Interested and tracking. No positions. Not a buy / sell recommendation.

2 Likes

Hi Mayur,

Very insightful

Retail business – Growth, margins disappoint; slippage in expansion

For FY15, Spencer’s (CESC’s retail business) posted a weak

performance – revenues (including other income) at INR16.7bn (up 15%

y-y) was 4% below our forecast, EBITDA loss (including other income) at

INR0.7bn (4% lower y-y) was 44% higher vs. our forecast and reported net

loss at INR1.5bn (10% lower y-y) was 16% higher vs. our forecast. EBIT

margin improved a bit from -7.5% to -6.8%.

Relative to our forecast, the earnings disappointment stems from both topline

growth (lower area accretion) as well as margins. Based on FY15

operating metrics, we believe same-stores sales/sqft in 4QFY15 was

INR1386 (up 2.7% y-y) and average sales/sqft stood at INR1305 (up 7.9%

y-y) on the back of area accretion being negligible vs. 4QFY14.

Management now expects Spencer’s to post a marginal EBITDA loss in

FY16 vs. previous guidance of EBITDA break-even. Delay in expansion

plans has been attributed to delays in property delivery; on a gross basis,

CESC now expects 10-12 new hyper stores to be added during FY16.

excerpts from a dated research on CESC

1 Like