Century Ply will be going for some de-rating with this guidance

Their guidance for FY17 has always been that this year growth will be low due to poor demand in real estate sector.

1 Like

Dear Abhishek, This company has always been conservative in guidance and i like the management for that. Real estate sector will not be recovering in a hurry but govt driven concepts like Smart cities can be a good game changer for this. Get afeeling like pidilite in its earlier days. 200-210 is a fair value for this one i feel. Norway pension is invested at 225. I am in since 2014 and got in last at 255.

2 Likes

Post 8th Nov…has management given any revised guidance ? I am expecting overall growth will be in the range of 6-7% max in FY 17. Kindly share your thoughts

Good part is FY16-17, all major capex is done. FY17-18 looking better

2 Likes

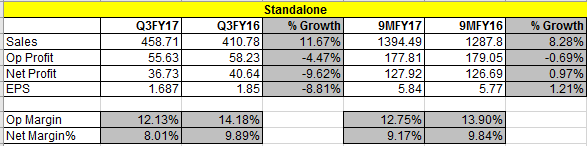

Q3 FY17 Results - Margins impacted due to increase in raw material prices.

Management expects formal plywood sector to benefit from demonetization and GST

1 Like

Management commentary after q3 results was a huge positive in my book. Sales growth due demonetization ( as local players were squeezed ) was a big plus. How many company reported a sales growth due to demonetization???

Additionally the implementation of GST will further hurt the local/unorganized players.

Hence entered the stock at Rs 200.

Q3 FY17 investor presentation and concall summary -

• Hoshiarpur plant for MDF is to start in Mar 2017

• Sainik sold 11,819 CBM (cubic meter) vs 12,037 cbm last year. This is despite impact of demonetization

• Ply sales have been strong in January 2017 as well

• There are around 3,300 plywood units in the country and out of 3,300 units, 2,500 are totally exempted, the turnover is less than Rs1.5 crore, 700 units are under the partial exemption their turnover is Rs1.5-5 crore and only 100 units are there which are in the full duty paying

• MDF plant: CPIL’s 600 CBM/ day capacity MDF plant is expected to come on stream by April, 2017. It entails an investment of 380 crore with 207 crore spent till December, 2016. The company would also use the MDF produce to make value added products like doors, pre-laminated boards. While it would also produce high density fibreboard (HDF) for manufacturing wooden flooring

• Market share: The company looked to maintain market share in difficult times post demonetisation. Hence, it gave dealers some discounts which led to a margin contraction. However, going forward, the management has indicated that they would reduce these discounts over the time

• Demonetisation impact: The management believes that demonetisation impact is over as the company witnessed ~5% growth in January, 2017. Though the unorganised sector is still witnessing problems, the company believes that it has a great opportunity to capture market share from unorganised players post demonetisation

• Pre-lam particle board plant: Currently, the company has a capacity of producing 1000 boards/day at its pre-lam unit and it would augment its capacity to 3000 boards/day by commissioning one more unit in next 3-4 months

• Commercial veneer: The realisations of commercial veneer increased sharply during the quarter as company sold premium veneer. It expects to maintain such realizations, going forward

• Pricing changes: The company has not taken any price hikes post demonetisation. It would benefit from softening raw material prices and so would look to maintain prices, going forward before the final rate of GST is known. Further, the unorganised players have already take price hikes of ~5% post demonetisation and could also take further price hikes. This would lead to contraction in price differential between organised and un-organised products which would help the company gain market share from unorganised players

• Winding up furniture business: The company has decided to completely wind up its furniture business which it started in 2012. Over the years, the division has accumulated losses of ~25 crore

• Laminates capacity expansion: The company is planning to rampup its laminates capacity by 50% to 7.2 mn sheets

• GST rate: The management expects a GST rate of either 18% against the current incidence of ~27-29%. Post GST implementation, a level playing field would be established and organised players are set to benefit

Near term triggers

• GST implementation is likely to migrate unorganised to organised sector

• Pre-lam is expected to give good growth

• MDF, new facility, is expected to give good growth - FY18 revenue is expected to be around 400cr; At full utilization it can generate 600 cr

7 Likes

- GST to aid organised players. Currently, the small scale industries (SSI) sector comprises ~3,300 units, of which 2,500 enjoy 100% duty exemption and ~700 are partially exempted. However, SSIs will be stripped of all exemptions as part of the government’s effort to create a level playing field, potentially shifting demand toward the organized sector.

- Opened plant in Guwahati, which will enjoy tax benefits for 10 years

- Laminates will fall under 18% tax bracket as opposed to 29% of current taxes. Again, this may help in migration of value from unorganised to organised. Century is enhancing capacity by 50% to be commissioned by Sep 2017.

- Major growth in MDF expected

6 Likes

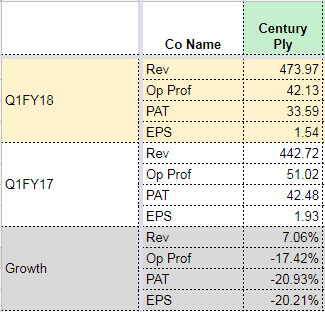

Q1FY18 Results

2 Likes

#Some of the key Points from Annual Report:

##Business Overview

• CenturyPly is India’s leading organized plywood brand with a market share of around 25% of the country’s organized sector.

• The Company offers plywood, laminates, veneers, MDF, block boards, doors, fiber cement boards and particle boards.

• The Company’s products are available across the country through 31 marketing offices covering over 630 cities and townships addressing 1,800 dealers and nearly 16,500 retailers.

##Current Capacity and Future CapEx

With Government push to Housing and Infrastructure Century ply created the perfect runway for sales to strengthen over the next few years.

• Plywood – Current capacity is 2,10,000 cubic meters. Centuryply’s existing capacity is ~60% higher than its nearest competitor. Century ply’s capacity utilization was ~85% with attractive operating leverage. We are commissioning a facility in Punjab to address incipient demand.

• Laminates - Centuryply is the third-largest player in India’s organized laminate segment. Current capacity is 4.8 million and we are scaling this by 50% by September 2017.

• Particle boards - Centuryply commissioned a 54,000 cubic meters particle board manufacturing facility at a capex of INR600 million in FY17. The location was strategically chosen to be Chennai as ~50% of the raw material requirement was accessed from a captive unit in the vicinity

of the plant and the rest from third-party units located in the hinterland. The plant

can potentially generate INR1 billion worth of revenues while operating at peak capacity.

• MDF - Centuryply is in the process of commissioning India’s largest MDF unit in Punjab with a 1,98,000 cubic meters capacity. The plant is expected to be up and running by H1FY18. We are planning to manufacture value-added products such as laminated MDFs, flooring and doors, among others. Consequently, we are hopeful of generating probable revenues as high as INR1.50 billion in the first year.

At peak capacity, the particleboard and MDF units are expected to generate annual revenues in excess of INR100 crore and INR450 crore, respectively and the unit is the largest MDF capacity in the country.

Along with product capax we will commission warehousing hubs in Guwahati (to service North Eastern India), Kolkata (to service Eastern India), Chennai (to service Southern India), Roorkee, Karnal (to service Northern India) and Nagpur (to service Western India), enhancing logistical effectiveness.

##GST - A Game Changer

The INR18,000 CR Indian plywood sector is largely dominated by unorganized players who account for more than 65% of the total plywood market.

• India has nearly 3,300 plywood units, of which around 2,500 units are exempt from paying any kind of duties or taxes; 700 units are partially-exempted. The organized sector pays 28-30% in the form of various duties and taxes. Besides, organized players also need to pay CST related to the inter-state movement of stock, making their products dearer by ~ 30-40 % compared to unorganized alternatives.

• The price difference will decline and to account for the reduction in exemption limit from INR1.5 crore to INR20 lac. Superior products quality offered by the unorganized players could propel customers to switch to organized brands.

• Besides, with exemption limits declining, unorganized players will need to rely solely

on bank financing; they would no longer be able to access credit for purchasing plantation timber. As costs rise, a number of inefficient plants could shut operations.

• On the other hand, idle capacities of organized players could progressively come on stream to address emerging demand.

• Centuryply is attractively placed; the Company expects to increase capacities at its existing facilities at a fraction of the capital cost and in quicker time, resulting in a timely, efficient and profitable address of marketplace realities.

##Some Interesting Facts about Century Ply Operations:

• As India encountered demonetisation and industry players complained of revenue sluggishness, Centuryply reported a 14.8 % q-o-q growth in net revenues and almost 50% growth in PAT during Q4FY17.

• The Company achieved a plant efficiency

of > 90% to moderate overheads. The Company sourced raw materials from Laos and Myanmar, which helped moderate the overall cost of raw materials as a proportion of revenues. The Company achieved the highest per machine productivity in the industry.

• Centuryply’s per person productivity, the highest in the industry, warrants fewer people. This was achieved by streamlining processes, incentivising outperformers, best- in-class practices and regular maintenance. Here’s proof: our press was running at 93% efficiency, targeted

at 100% in 2017-18; we increased laminate output >15% without additional capex.

• We were the first Indian company to set up a peeling unit in Myanmar, a country with abundant timber resources; the objective was to secure quality raw material in a cost-efficient manner. The peeling of logs in Myanmar and sending the face veneers to India has not only helped curtail costs but also cushioned Centuryply from the risk of nationalist policies by the Myanmarese Government. Timber logs, owing to their unwieldy dimensions, occupy more space and raise transportation expenditure; face veneers are convenient and cost-effective to transport. When companies importing timber logs from Myanmar suffered a body blow following the Myanmar government’s decision ban commercial logging, Centuryply remained unaffected.

##Management Outlook & Visions

The Company is promoted by first-generation entrepreneurs like Sri Sajjan Bhajanka, Sri Sanjay Agarwal, Sri Hari Prasad Agarwal and supported by Sri Vishnu Khemani and Sri Prem Kumar Bhajanka.

##Director said

I believe that Centuryply stands attractively placed to capitalise on the next growth level: we expect to generate incremental revenues of INR700 to INR1,000 cr during the current financial year with another INR500 cr of revenues in 2018-19. This indicates that even as we took nearly 20 years to climb to revenues of INR500 cr, we can potentially, replicate this growth in just the next two years. It is this optimism that I intend to extend to our stakeholders. All that we achieved in the last decade was in the face of sectoral and tax challenges; what we are now likely to achieve is with the tailwind of systemic support. And that could make all the difference.

6 Likes

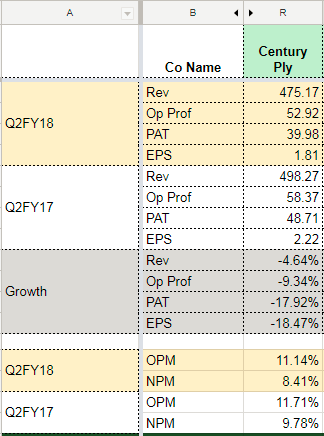

Q2 Results: Lacklustre results

2 Likes

I think untill e-toll is launched which has now delayed to April 18, the real benefit of GST won’t happen. Remember in one of concall management telling this . Also, seems unorganized players having free run. However, good to see 300+ cr of MDF assets being visible in balance sheet which is yet to contribute to profit . With a very conservative estimate, this should contribute to 35 crores of profit once it scales up by capacity utilization .

4 Likes

Latest presentation by company :

http://www.bseindia.com/xml-data/corpfiling/AttachLive/5c9ca171-6a2e-408c-b814-c1fd62aef99d.pdf

GST rate on plywood is decreased from 28 to 18.

NOTES FROM EDELWEISS CONFERENCE - 01-FEB-18

Plywood segment: Dumping of material by unorganised players prior to e-way bill implementation is impacting growth of organised players. However, Century has benefited from cut in GST rate from 28% to 18%, which has narrowed the price gap between unorganised and organised players from ~40% earlier to 25% currently.

Management believes expected benefit of GST has not yet come in and increasing compliance by unorganised players with e-way bill implementation should help Century gain market share. Management expects more than 20% growth in plywood segment post e-way bill implementation.

MDF segment: Century has already achieved breakeven in the MDF segment and is operating at more than 70% utilisation, which is expected to increase to 80% by FY19. The company can reach turnover of INR 500 cr with current capacity and expects margin to inch up 200bps with every 10% increase in utilisation rate. Existing plant has potential capacity expansion of 400cbm (current 600cbm) with incremental capex of INR1bn, which will further support margin expansion. Further, in light of robust demand led by growing applications, the company is evaluating expansion of MDF capacities in Assam and UP. Growth in this segment will also be supported by Century’s plan to add a MDF unit in JV with a Chinese player. The JV plant with capex of ~INR60cr will be able to generate INR200 revenue.

Laminates segment: Management expects domestic laminates revenue to grow by more than 10%, whereas export sales are pegged to jump 20%, leading to overall growth of 15-20% in the laminates division.

Investment conclusion: We believe, the plywood industry is going through structural changes—GST triggered shift of market share from unorganised to organised players and challenges in raw material sourcing. Further, Century is set to take advantage of its recently completed capex (INR3.5bn) in MDF division and is well-positioned to reap the benefit of anticipated demand upswing. On back of strong branding, widening distribution reach and ensured raw material security, we estimate the company to post revenue, EBITDA and PAT CAGR of 20%, 24% and 28%, respectively, over FY17-20 with RoCE expected to improve to ~27% in FY20E from 22% in FY17.

9 Likes

Hi,

I’ve been tracking the industry for some time. Had a few questions pertaining to the same.

-

Could someone please explain the reason for fall in volumes for MDF business in Sep-18 quarter? In fact, the rupee depreciation should have helped in substituting the imports and thus realizing higher volumes.

Is it just a subdued quarter? The industry has been gung-ho about India’s MDF consumption story. It’s quite alarming to see the growth being lackadaisical. -

Also, both Century and Greenply have seen a drastic fall in the EBITDA margins for MDF business in Sep-2018 quarter from the Jun-18 quarter. It’s quite intriguing as the plywood margins have remained as such.

I understand that the average price realizations have fallen by ~4% for Century. But, this doesn’t explain the whole story for such a significant fall in EBITDA margins.

Disclosure: I have bought a tracking position in Greenply during the recent meltdown. Yet to develop conviction for long term buy.

Century, Green n action , the three big players have come with a huge MDF capacity expansion at the same time (550cr CapEx by century , some 800 cr CapEx by green ). Result there is an oversupply in market n margins have been hit. Expect this to continue for at least 3-4 quarters n as demand supply balances, normalcy would come. The other thing is both these companies had foreign currency loans n they were unhedged and both have inoccured forex losses. Century never hedged n today mgmt said going forward they will hedge to avoid any future quarter loss which means there would b a new hedging cost for sure on expense item . Greenply plan to export 30% of MDF which should act as natural hedge but till that time it does not happen , I m not sure what is their plan B. The MDF margin fall n forex losses both were expected if one has gone through last 4-5 quarters of concalls of both players to understand industry dynamics . Also, as per century AR , a 5% currency fluctuations would lead to 49 cr of annual forex losses but let us hope with slight rise in hedling expense, they do what is prudent . Disc : Have taken 1% exposure each into century n greenply as valuation wise see some value emerging ,however, for any significant accumulation, waiting for stabilization signals at right valuation.

6 Likes

What is the reason behind very low Tax Rates ?

CRISIL has come up with the Ratings and mentioned about Non-Cooperation from Management in April 2018. The stock then corrected from 350 to 170 in last 8 months. Looking at the high debt on the books , is there any current update from any Rating Agency ?

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Century_Plyboards_India_Limited_April_10_2018_RR.html

3 Likes