I found continental sachets in Jim Corbett and Binsar Mahindra resorts.

Correct me if I am wrong, my understanding is that ccl has a small revenue from retail, most of their sale is wholesale coffee

Yes, you’re right. The Retail sales are currently miniscule compared to the Exports.

1 Like

ID’s Filter coffee has reached stores near me. I have not tried it yet. ID has the distribution and brand advantage. It is also widely available on ecommerce.

I though believe that more innovative products will only develop the market and increase the number of coffee drinkers.

1 Like

1 Like

What will be impact on CCL due to new additional supply capacity in freez dried coffee category by Tata? CCL has already has headwinds.

What to make of domestic business of CCL is the critical questions. And as you rightly said, when you are taking on Bru/Nescafe of the world, you have a tough fight.

Whether they will succeed or not, only time will tell. What we can do is look at the things they are doing to make themselves successful -

-

One of the first thing promoters have done is to hire Mr. Pravin Jaipuria to lead the domestic business. It requires different mindset to lead the B2B contract manufacturing business vs. a branded business. It was good of them to hire an external professional and it also looks like he has good autonomy based on conf call. Pravin has been a long time veteran of Dabur, following is his profile ->

https://www.linkedin.com/in/jaipuriar-praveen-7a4b2b9 -

Second thing as you pointed out is, CCL spent Rs. 20Cr. on advertising & promotions and they expect to invest all the EBITDA into A&P for next 2/3 years.

Let’s try to put this 20-30Cr A&P spend number in perspective - by management’s estimates instant coffee market in India is 1500-2000Cr and filter coffee market is another 500Cr. So total market size is 2000-2500Cr. Assuming 3% ad spends for whole industry, the total number comes to 60-75Cr. So CCL is spending 20-30Cr on ads on b2C sales of 30-40Cr. I think this spend number is already significant when compared to competition.

I think this kind of spend is needed when you are taking on two entrenched brands and CCL’s B2B business allows for this. Even Pidilite spends 3-4% on ads for Fevicol and others to keep competition at bay. Tracking A&P spends in companies that claim to be FMCG is an important factor.

Most of these ads are in local languages and hence I am unable to have any qualitative view on ad campaign. I would be happy to hear views of people who track and understand this. -

Another thing I was skeptical about was trying to create too many products and confuse customers - speciale, premium, strong, extra etc. In my limited experience, this type of strategy takes the focus away, esp. on B2C side. It seems they have gotten their act together and are focusing on only 2 brands - “Extra” and “Malgudi”. Continental Strong is cheaper spray dried coffee and looks to be targeted towards bulk institutional sales. Continental Speciale is the premium coffee targeted towards coffee connoisseurs. Based on Amazon.in, it looks like there is new 100% freeze dried product called “Continental Black Edition” focused on black coffee drinkers. This might be same as Speciale. In short, Extra and Malgudi are two mass market brands they are focusing on.

-

They have chosen to focus on 5 southern states for their domestic market which forms 60-70% of overall India B2C coffee market. In these 5 southern states, Bru is more dominant player compared to Nescafe. So I like that they are choosing the right opponent to fight as in my mind, brand equity of Nescafe is much stronger than Bru. Also “Malgudi” is filter coffee product targeted in these states.

-

I have seen their coffee being places in premium hotels, airlines & many people in this forum have shared this experience. I think they are using institutional sales to create brand awareness. When you find Continental Coffee in say Lemon Tree or some other premium hotel, one does not think of it as “cheap” brand but rather as a luxury/aspirational brand.

So overall it looks like the direction of B2C business seem to be correct.

What I feel is, end market size in India for coffee is rather small at 2000-2500Cr. I think first milestone would be to get to 10% market share and then things might become tougher from there. So overall domestic B2C business probably presents a case for multiple expansion but I think it is going to be a long drawn battle for which many investors might not have patience or investment case can not factor in B2C business.

The triggers on B2B business are quite encouraging as - all this year’s gains have come from increased capacity utilization in Vietnam plant. For FY19-FY20, new freeze dried capacity of 5000T will provide boost. By that time, hopefully additional capacity of 3500T in Vietnam & India packaging expansion might be ready. And In 3-4 years, hopefully with market expansion, management is able to find another 5-10,000T expansion opportunity.

The worrying part is competition on freeze dried side that Srishant has been flagging for over a year, 5000T capacity expansion by Tata and his comment in Q3 conf call that - “Premium for freeze dried coffee has come down”.

Overall, it remains a slow, boring business and not one that can generate excitement by delivering 30-40% growth. There are both optionalities and competitive threats on horizon. Let’s see how this unfolds.

Disc - I hold, 5% of portfolio, no transactions in last 90 days. This is not buy/sell reco.

24 Likes

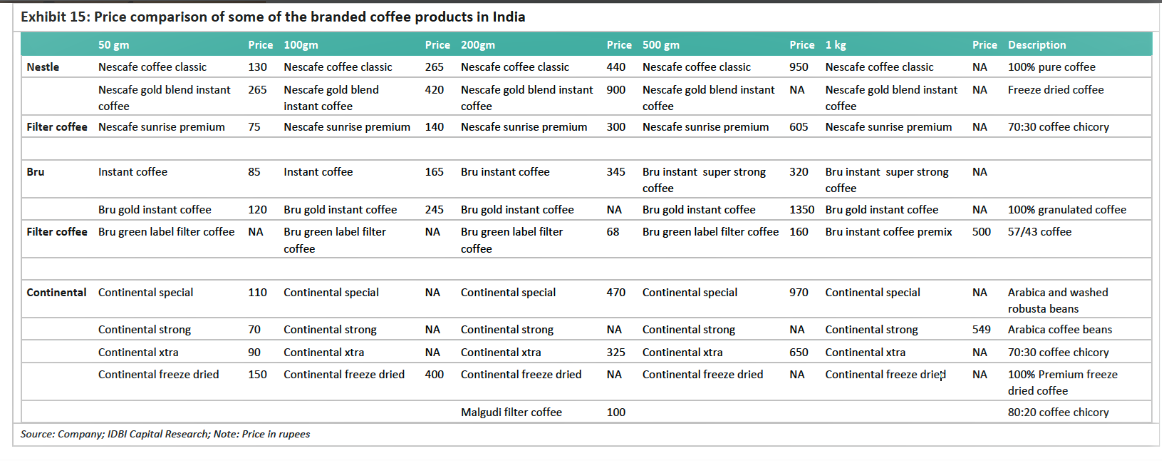

CCL’s pricing strategy is changing. To quote the article “It is interesting to note that the company is not competing with the two established brands based only on pricing. Small

sachets of Continental coffee are priced cheaper compared Nescafe which is considered a premium brand although they

are slightly expensive compared to Bru. However, CCL’s large packets (above 200 gms) are expensive compared to peers.

CCL has also entered the filter coffee market with Malgudi.”

7 Likes

Could you please share the article link ? Thanks

CCL Products (India) Ltd SEZ Unit in Kuvakolli Village, Chittoor District of Andhra Pradesh that was set up for manufacturing of freeze dried instant coffee with a capacity of 5000 Mts per annum will commence its commercial operations with effect from 20th April, 2019.

9 Likes

1 Like

Any idea whether these borrowings are from domestic institutions or from foreign ones?

Surprisingly poor Q4 results from CCL Products. I hope the lower revenues are due to one off reasons and not something concerning like losing client contract.

Hoping that Mr Shrishant clarifies on this soon in his quarterly post results TV interview

Conacall notes Q4FY19

-

Earnings and sales in Q4 were down as we lost one major customer during FY19. He was a repackager to whom we were supplying for the past 10 years. He has setup his own manufacturing capacity which was not anticipated. He used to buy 2000 tonnes and sales were around Rs. 50 cr. He was buying only spray died coffee. Whole of 2000 tn lost business was mostly in Q4 and partly in Q3.

Never heard in past 20 years that repackager gets into manufacturing, it’s always the other way around. Earlier we did not go after his clients but now we can go after them and sell to them directly. Infact of the 20 new customers we acquired some are his clients. We are offering him coffee at lower price than his manufacturing cost. We won’t be surprised if he sells his manufacturing unit in the future. -

It’s not easy to get into coffee manufacturing business. This business has always been closed network and requires a lot of expertise. People won’t buy from inexperienced manufacturers.

-

We lost 2000 tonne customer but we have gained 20 customers and will recoup 500 tonne sale to these customers. Profit on these 500 tn customer will be same as 2000 tn, as these are small packagers and profits in these are higher as compared to bulk booking. No receivable from the customer we lost.

-

Other expenses were higher in Q4 due to increase in Selling and Distribution expenses and it will continue at these levels going forward.

-

In domestic business competitions are taking us seriously. We want to be agressive in domestic market. That’s why other expenses won’t come down as we want to gain market share.

-

Depreciation was lower due to change in calculation method for Switzerland plant.

-

15-20% growth guidance for FY20 in sales, profits and volumes.

-

Volume were flat in FY19.

-

Coffee price down by 10-15%. Coffee prices expected to stay low. Farmers started hoarding coffee as they are not ready to sell at these lower levels.

-

Receivables were higher due to USA business. Working with a partner in USA for the past 20 years and expanded credit period to him to grow in USA markets. Earlier we were working with his father and two years back son joined in and now working with him. After initial two years the relationship is going great and we have expanded the types of products sold to them. Expecting 20-30% growth in USA business.

-

We don’t give any credit to new customers and this has been our policy from the very beginning and that’s why we never had any bad debts.

-

50% capacity utilisation in FY20 for new SEZ plant started on 20th April 2019.

-

Rs. 80 cr. domestic business which includes

Pure Retail B2C: Rs. 35 cr. (It was Rs. 9 cr. in FY18)

Army tenders: Rs. 15 cr. (Rs. 13 cr. in FY18)

Private Label: Rs. 30 cr. (at same levels in FY18). -

Looking to double B2C business in FY20.

-

Vietnam did better than last year on standalone basis. Will continue to declare dividend from Vietnam subsidiary going forward. Capacity utilisation was 75% in FY19 for vietnam plant. Sales in FY19 were Rs. 264 cr and PBT was Rs. 67 cr.

-

Switzerland subsidiary in FY19 did Sales of Rs. 38 cr and PBT of Rs. 77 lac. Applied for sale in 4 supermarkets and got approved as L1 supplier. Looking at $500K PBT from this unit going forward.

-

Capex:

$ 10 mn for repackaging and agglomeration unit at Chittor location of 6000 tonne. This will not be in SEZ area. At chittor we have 100 acre land off which 30 acres is in SEZ and 70 acres outside SEZ.

$ 8 mn for 3500 tonne additional capacity at Vietnam. -

Earlier we use to focus more on high volumes and capacity utilisation but for the past one year we are focusing more small package customers as it’s more profitable and more sticky than bulk customers. Built an entire marketing team to get small package customers.

-

Less than 20% of business is from small packages and premium products. Going forward we are targeting it to be 30% in FY20.

-

Interest capitalised during the year was Rs. 6.3 cr.

-

Advertisement expenses were Rs. 10 cr for FY19 and Other S&D expenses were Rs. 10 cr for FY19.

-

70-75% of volumes of FY20 already covered.

Regards

Harshit

31 Likes

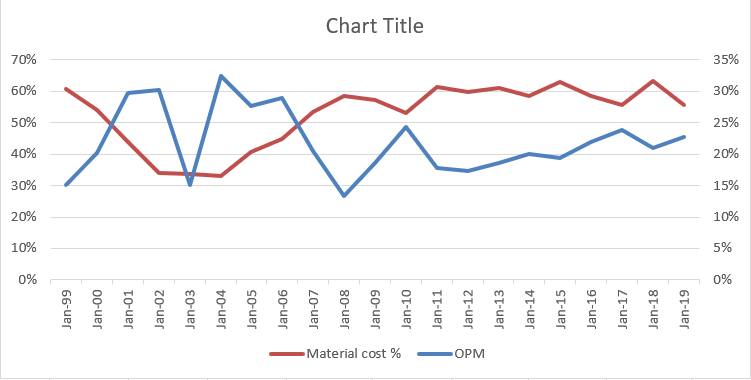

Just wondering about the claims of the company that the coffee price does not affect it, since it sells on cost+ basis. However if we look at the way the margins moved against the raw material price:

Year 2003 has a jump in some costs, barring that, the margin mirrors the coffee prices.

| Narration | Mar-99 | Mar-00 | Mar-01 | Mar-02 | Mar-03 | Mar-04 | Mar-05 | Mar-06 | Mar-07 | Mar-08 | Mar-09 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OPM | 15% | 20% | 30% | 30% | 15% | 33% | 28% | 29% | 20% | 13% | 19% | 24% | 18% | 17% | 19% | 20% | 19% | 22% | 24% | 21% | 23% |

| Material cost % | 61% | 54% | 44% | 34% | 34% | 33% | 41% | 45% | 53% | 58% | 57% | 53% | 61% | 60% | 61% | 59% | 63% | 59% | 56% | 63% | 56% |

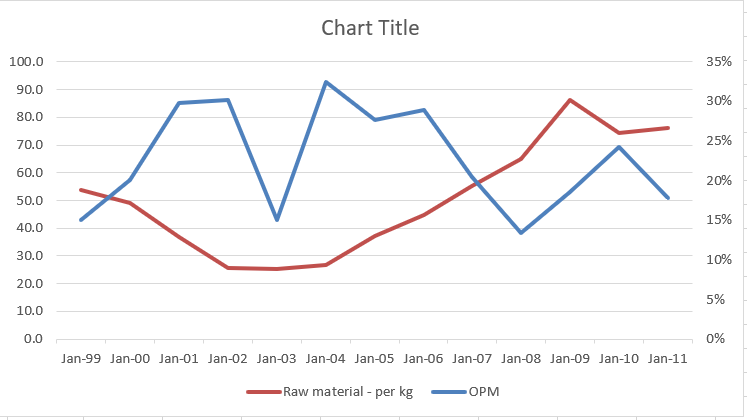

| Narration | Mar-99 | Mar-00 | Mar-01 | Mar-02 | Mar-03 | Mar-04 | Mar-05 | Mar-06 | Mar-07 | Mar-08 | Mar-09 | Mar-10 | Mar-11 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OPM | 15% | 20% | 30% | 30% | 15% | 33% | 28% | 29% | 20% | 13% | 19% | 24% | 18% |

| Raw material - per kg | 53.9 | 48.9 | 36.7 | 25.7 | 25.2 | 26.7 | 37.4 | 44.9 | 55.1 | 65.0 | 86.1 | 74.4 | 76.3 |

(This is from the raw material cost details from the AR, available only until 2011)

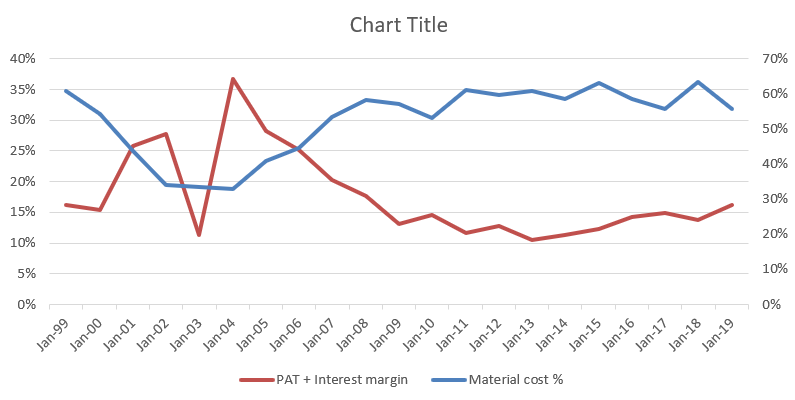

| Narration | Mar-99 | Mar-00 | Mar-01 | Mar-02 | Mar-03 | Mar-04 | Mar-05 | Mar-06 | Mar-07 | Mar-08 | Mar-09 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Material cost % | 61% | 54% | 44% | 34% | 34% | 33% | 41% | 45% | 53% | 58% | 57% | 53% | 61% | 60% | 61% | 59% | 63% | 59% | 56% | 63% | 56% |

| PAT + Interest margin | 16% | 15% | 26% | 28% | 11% | 37% | 28% | 25% | 20% | 18% | 13% | 15% | 12% | 13% | 10% | 11% | 12% | 14% | 15% | 14% | 16% |

This shows that the company does not have pricing power, isnt it?

And, keeping aside the domestic retail foray, how do we estimate the future margins and hence the profits? How can we say the company is going to sustain its profits? What if the coffee prices escalate to very high levels?

Or since the aforementioned is not so clear, is the investment thesis currently based solely on the future of its retail foray, that it will eventually rise above the coffee price variations?

5 Likes

Good work buddy. I have some questions that may help uncover this further:

- Is the % material cost a % of total cost or revenue?

- Can you add revenue per kg line next to raw material cost per kg?

Thanks!

Thank you @onlish2014.

-

it is material cost as a % of total sales.

-

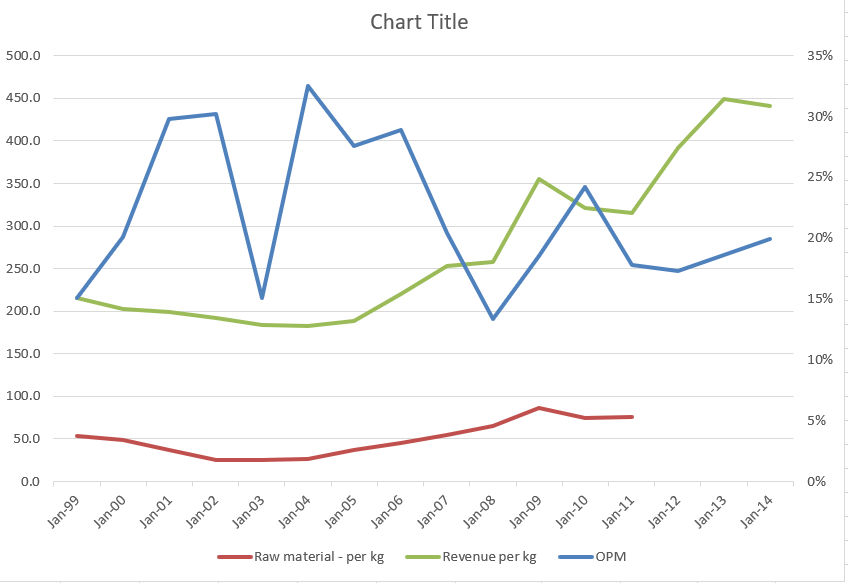

Here is it:

| Narration | Mar-99 | Mar-00 | Mar-01 | Mar-02 | Mar-03 | Mar-04 | Mar-05 | Mar-06 | Mar-07 | Mar-08 | Mar-09 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OPM | 15% | 20% | 30% | 30% | 15% | 33% | 28% | 29% | 20% | 13% | 19% | 24% | 18% | 17% | 19% | 20% |

| Raw material - per kg | 53.9 | 48.9 | 36.7 | 25.7 | 25.2 | 26.7 | 37.4 | 44.9 | 55.1 | 65.0 | 86.1 | 74.4 | 76.3 | |||

| Revenue per kg | 215.3 | 202.6 | 198.9 | 191.9 | 184.4 | 182.7 | 188.4 | 220.2 | 252.7 | 257.6 | 355.9 | 321.7 | 315.3 | 391.5 | 449.7 | 441.5 |

Unfortunately the volume details are available only till 2014, and the raw material cost details are available only till 2011 AR. I didnt take green coffee traded price from any other source thouh.

Until 2011, it looks to be reflecting the same as that of raw material cost per kg.

2 Likes

Investor conference call at 4pm, 11th July 2019

2 Likes