Thanks for the photo as it clarifies. Since CCL is also a contract manufacturer either the private labels or even the branded products owned by other brands would have been manufactured by CCL. This is the primary business of CCL all along and it has a range of margin. We do not ignore that as it generates the primary volume and the bottom line as of now.

But going forward we should be judging the brands owned by CCL namely Continental Speciale, Continental Premium and Continental Supreme. Because these are ones in which they are planning to invest in marketing and through which they can earn a higher margin. Probably far higher than what they do as a contract manufacturer of other brands or private labels.

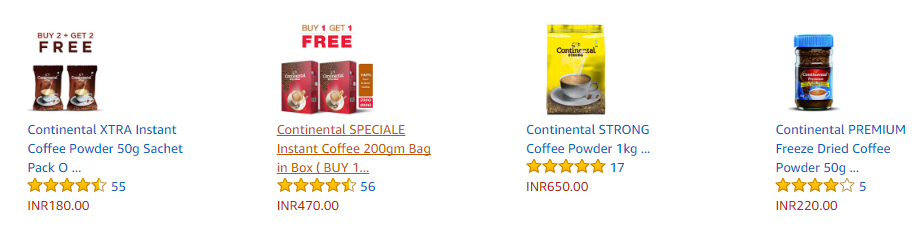

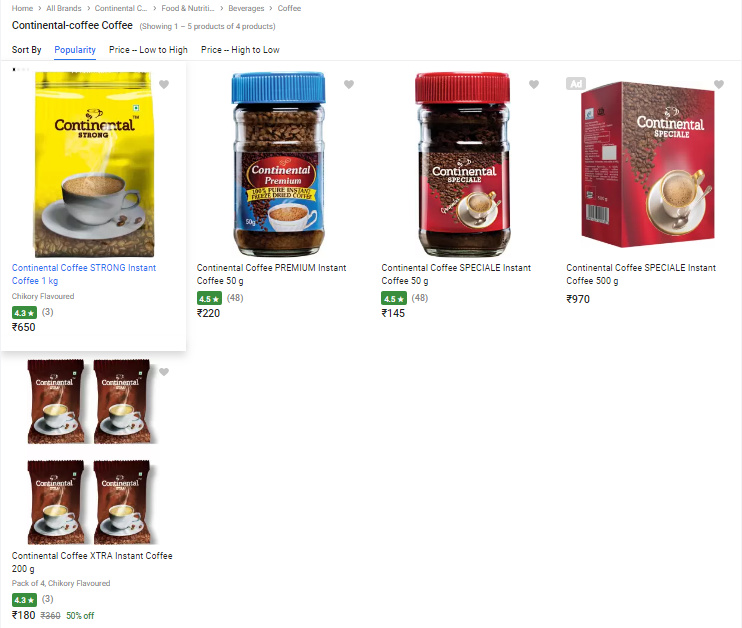

Just FYI this is private label. CCL sells its coffee to modern retail like Future and Future then repackages it and sells under its own brand. Quality and taste of this kind of bulk coffee that CCL sells might not be as good as the quality & taste of its own brand - Continental Coffee. Do try its all 3 sub-brands - Continental Coffee Supreme(chicory mix), Speciale (spray dried) and premium (freeze dried). Taste wise and price wise pecking order would be premium (highest) > speciale > supreme.

I am a connoisseur of coffee and I feel that Continental Speciale is on par with the quality/taste of Nescafe classic (Nestle’s spray dried version). Nescafe Gold (Nestle’s freeze dried version) I haven’t tried so will not be able to compare with CCL’s premium.

Just to add on to the discussion, Fresh & Pure should not be called as private label because it is also sold outside Future Group retail network (e.g. Amazon, Flipkart). In future it will become available in other retail shops similar to Bru or Nescafe. Thus it is stand alone brand by Future Consumer.

Hi,

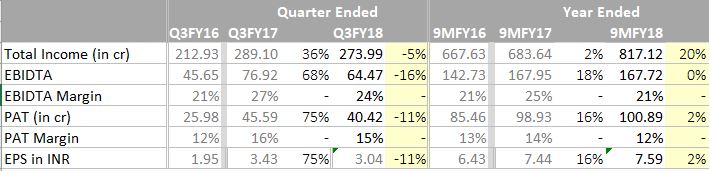

Last year q3 they have very high base due to q2 plant shutdown they executed some order in q3 due to that base higher, we see optically result looks flat.will wait for mgmt concal for more detail

Regards,

Sathish

Concall summary for Q3’FY18 (please pardon any typo or mis-interpretation), kindly listen the same to validate

Have tried to summarize points as far as possible (so this is not a transcript)

Margin likely to increase in Vietnam given Aglomeration plant is on steam since October 2017

Vietnam at peak utilization currently; Focusing on better product mix from Vietnam

Volume growth came from Spray; Freeze dried almost at full capacity so don’t expect until new plans comes up by 2Q of next year

Revenue growth projection of 15-20% due to decrease in green coffee prices; Margins and volume growth to remain intact

Have back to back contract to cover raw material in dollar terms which is 70% of raw material; Don’t speculate on green coffee prices

Continental: Revising supply chain margins, offers, schemes etc. ; Volume guidance to 70 Cr FY18E, increased gross margins % guidance to 30%

Continental strategy changing from alternative “me too” product premium brand; Response has been good so far; India is 1,800 cr market (instant coffee market) - all segments 4,000 cr market

Continental focus on South Indian states currently; Not much investment is required currently

Global coffee market growing at 2.5% but lot of consolidation happening; 1 big US manufacturing company on verge of shutdown (around 10,000 tonne capacity company) due to competition of Asian companies

Getting some new orders from Switzerland plant

Freeze dried plant on track to start in Q2 FY19

Overall Instant coffee market in India: South - 80%; North - 20%

Targetting atleast 10% profit growth yoy FY18 vs FY17; last year quarters not comparable; Expect strong earnings next quarter

New plant can expect 40-50% utilization next year

India and China has substantial instant coffee consumption; Soluble coffee growth due to this

Supplying to 90 countries; will not depend on specific geography

Global customers are brand owners and supermarkets + re-packers (they do blending and packing)

Might plan to enter filter coffee in future (roasted coffee); It is a 1,000 cr market

Avg realization in domestic: around INR 500/kg

Volume growth drivers for CCL: Customer relationships, Blend kept confidential and R&D with CCL, Blends difficult to replicate, Upgrading technology to give product before competitor can give, consistent timely delivery; Growth will come from existing and new customers

Competitors adding freeze dried coffee from 2 major companies; There is pressure on pricing and current margin looks sustainable

Currently focussing on volume growth and then convert client to move to higher wallet share

Trying to grow B2C in systematic manner

Capital allocation: Repayment of debt to start in 1-1.5 year + shifting dividend policy as required

Prices of Robusta to be firm but there is good crop this year

Targetting 1-2 big customers every year on recurring basis

Specialty coffee is max 5% of portfolio; Margins around 30-40%

Planning to grow low unit business going further (currently contributes to ~30% of portfolio)

Next year better utilization expected once new capacity is on steam

In my Hometown (Nellore,AP) continental coffee is getting huge positive response. Ppl tasted continental first due to thier marketing efforts(they kept free tasting stalls, buy one get one offers) but those who tried it many are permanently shifting to continental. Some retailers said that customers are particularly asking for continental.

Sorry, I could have put it in a better way. I should have asked about bottom line growth. Are there any unknown factors like depreciation, tax changes, one offs that could push bottom line disproportionately than previous years?

Currently they have given ~20-22% EBIDTA Margin guidance. Not sure about incremental depreciation from new capex, but yes it should marginally give higher growth than topline. We will get an exact idea once capex is completed.