News update

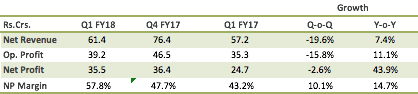

Q1 FY18 results announced:

Results were better compared to Q1 FY17, but lower than Q4 FY17. I have observed for last two years that CARE generally has Q2 & Q4 better quarters than rest two, kind of cyclicality. In that sense at least revenue growth is OK.

However when one looks at margins, picture is better - OPM & NPM both have improved Q-o-Q and Y-o-Y, which is certainly good news. The margins are improving for last two quarters (q-o-q and y-o-y) which seems to be suggesting operational efficiencies coming into picture. A confirmed trend, however, would be clear once we get results for next couple of quarters.

Disc: Invested, no transaction in last 6 months

1 Like

One may have to look at notes to account about booking of surveillance income which I understand is now spread over year as against booking on one time in year. It may have some impact but I am not able to quantify same. Probably, it not be material but we shall get more clarity on same

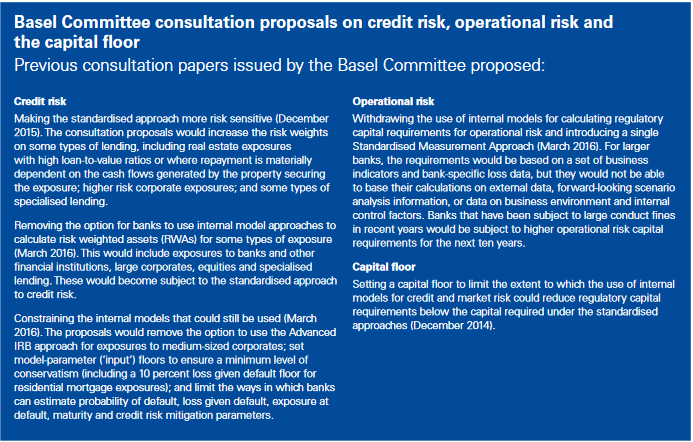

Dear Mr Dhiraj Dave, appreciate your postings about CARE in this forum. Could you please guide me on status of BASEL III implementation. Are banks being allowed to do internal rating of debt instruments ? If so, What would be impact on CARE’s future ?. Thanks.

Can someone has any perspective on the issues like… In case Ratings provided by the credit agencies goes terribly wrong( say by negligence or any other reason for that matter) is this guys(eithet Crisill, CARE , ICRA} are accountable …like consequences of penality or make good of looses for other parties… reputation risk anyways thats obvisiouly there.

I saw in one of post saying CARE ratings are liberal… that means in bluntly equality iissues… so wanted to understand consequences of lapses…will that be quantifiable in terms of finanacial burder if not is there any way to figureout?

Apologize if my post looks silly to other experienced members☺

I have no background in finance, but I place below my understanding of this topic, with a brief background and some references.

The Basel iii Accord

Basel III is a comprehensive set of reform measures, developed by the Basel Committee on Banking Supervision, to strengthen the regulation, supervision and risk of the banking sector.

The Basel Committee (India is a member) is the primary global standard-setter for the prudential regulation of banks and provides a forum for cooperation on banking supervisory matters. Its mandate is to strengthen the regulation, supervision and practices of banks worldwide with the purpose of enhancing financial stability. The Committee reports to the Group of Governors and Heads of Supervision (GHOS).

The Basel III reform measures aim to:

- Improve the banking sector’s ability to absorb shocks arising from financial and economic stress, whatever the source

- Improve risk management and governance

- Strengthen banks’ transparency and disclosures.

This reform translates into 3 pillars that are actionable, the first one is about Capital/Risk, second pillar is about Risk monitoring and the third pillar is about Reporting by banks. The goal is to curtail off-balance sheet exposures, and to decode the complex financial products that almost brought the world’s financial system to the knees in 2008. Now the banks also need to mandatorily report the exposures due to subsidiaries or group companies that can impact the bank.

If one skims through the Basel-iii document, it is clear the direction is towards better monitoring and disclosure of risks and credit risk is included in this accord. Each country may have its variant of implementing this accord, but our RBI has been more conservative than the accord in terms of norms and capital requirements and risk assessment. Note that sections of Basel-3 have been under implementation since 2013 and is expected to complete 31/3/2019, so this is nothing new that we are now encountering.

1 Like

RBI has its interpretation of Basel-iii here:

Risk assessment has two approaches – Standardised and Internal Ratings Based. In sec 2.2, pp 6, it is clear that the Internal Ratings has been available as a tool to Banks even since Basel-2, but the RBI recommendation is very clear, refer sec 2.2:

2.2 Keeping in view the Reserve Bank’s goal to have consistency and harmony with international standards, it was decided in 2007 that all commercial banks in India (excluding Local Area Banks and Regional Rural Banks) should adopt Standardised Approach for credit risk, Basic Indicator Approach for operational risk by March 2009 and banks should continue to apply the Standardised Duration Approach (SDA) for computing capital requirement for market risks.

Now what is Standardised approach?

The term standardized approach (or standardised approach) refers to a set of credit risk measurement techniques proposed under Basel II capital adequacy rules for banking institutions.

Under this approach the banks are required to use ratings from External Credit Rating Agencies to quantify required capital for credit risk. In many countries this is the only approach the regulators are planning to approve in the initial phase of Basel II Implementation.

What does RBI have to say on this topic wrt Basel-3?

8.3.9 The Basel Committee has suggested two broad methodologies for computation of capital charge for market risks. One is the standardised method and the other is the banks’ internal risk management models method. As banks in India are still in a nascent stage of developing internal risk management models, it has been decided that, to start with, banks may adopt the standardised method.

4 Likes

Does RBI say anything on the topic of External Credit Rating Agency?

6.1.2 In accordance with the principles laid down in the Revised Framework, the Reserve Bank of India has decided that banks may use the ratings of the following domestic credit rating agencies (arranged in alphabetical order) for the purposes of risk weighting their claims for capital adequacy purposes:

(a) Brickwork Ratings India Pvt. Limited (Brickwork);

(b) Credit Analysis and Research Limited;

(c) CRISIL Limited;

(d) ICRA Limited;

(e) India Ratings and Research Private Limited (India Ratings); and

(f) SMERA Ratings Ltd. (SMERA)74

6.1.2.1 The Reserve Bank of India has decided that banks may use the ratings of the following international credit rating agencies (arranged in alphabetical order) for the purposes of risk weighting their claims for capital adequacy purposes where specified:

a. Fitch;

b. Moody’s; and

c. Standard & Poor’s

Are banks adopting it?

Attached are the Disclosures (3rd pillar) from SBI, ICICI, PNB and as you can see, every bank has adhered to the “decision” of the RBI.

icici bank__Basel3-Pillar-3-Sep2017.pdf (565.4 KB)

SBI__new_basel_iii_disclosure_Sept_30_2017.pdf (1.7 MB)

2 Likes

Ok, so what happens to IRB? Here’s where we as investors need to do our own risk assessment of the industry itself and not just CARE. The entire direction of Basel-iii is clearly towards making the banking industry more transparent, to introduce better control & monitoring of risks and it might not be a long shot to think that this will be re-inforced in upcoming Basel accords.

Basel-iv.

Current timelines for implementation are 2021-25 and Basel-iv is formalizing the leftovers of Basel-iii & resolving known issues. So this seems to be a maintenance release more than a major release ![]()

References:

- https://www.capgemini.com/consulting-nl/wp-content/uploads/sites/33/2017/08/02-014.15_report_road_to_basel_iv_webpdf.pdf

- https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2016/12/world-awaits-basel-4-nears-completion.pdf

- McKinsey report on Basel-iv

Note from KPMG document:

Note that the Internal models of banks would be curtailed and Standardised approach would be the norm (this is already the case in India, so this merely reinforces status quo). Basel-iv recognizes that previous accords have resulted in enormously complex internal models for banks and more importantly, there is wide disparity between the risks assessed by each bank. In other words, the reporting by each bank varies widely under current Standardised model and there is now attempt to streamline this so that there is uniformity in reporting across all banks. It is expected that External Credit Rating agencies will have role of assessing risk drivers rather than merely risk weighted assets.

4 Likes

RBI feb 12 2018 notification.PDF (222.5 KB)

So RBI released a new Notification yesterday which supersedes many older notifications and is a sweeping reform of the Indian banking industry. The fact that they released it prior to a Exchange Holiday should give a clue as to the impact of the new Notification! From a pure banking perspective, this new notification is quite prescriptive in terms of how stressed assets are to be resolved.

However, what is of interest to this thread is that the Resolution requires rating from an accredited rating agency for loans over 100 crores and where the loan is more than 500 crores, there has to be two ratings sought. The lender engages the rating agencies and pays for their risk assessment. This is in line with the general direction by RBI towards tightening the norms and cleanup and not trusting banks on what they say. In fact, there are weekly reports , monthly reports being sought, so this will be a lot of work to be done by banks in terms of classification of loans, coming up with Resolution plans which are to be approved by the boards. But it looks like there is a bonanza for Credit Rating companies.

Disc: Invested in CARE.

4 Likes

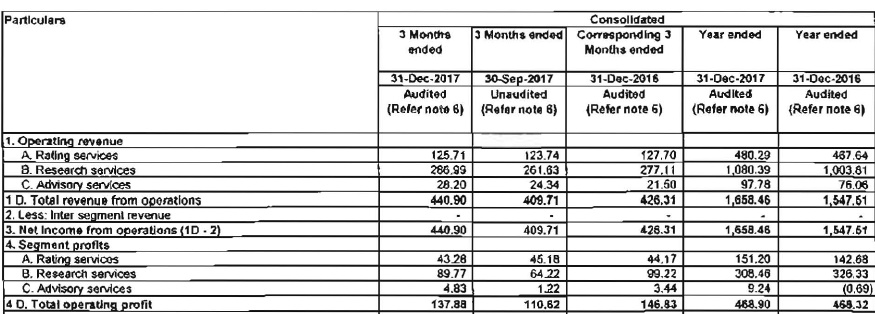

Care Rating quarterly PBIT is now highest in value term as well.

Find enclosed Crisil segmentwise performance

Care Rating has report PBIT (Calcualted at PBT-Other income) is higher then Crisil for last two quarters.

| Rs Cr | 31-12-2017 | 30-09-2017 | 31-12-2016 |

|---|---|---|---|

| PBT/PBIT | 50.22 | 71.75 | 50.20 |

| Other income | 4.65 | 6.25 | 6.68 |

| CARE rating Operational PBIT | 45.57 | 65.50 | 43.52 |

| Crisil Rating PBIT | 43.28 | 45.18 | 44.17 |

1 Like

The company is near its 52 week low although there has been no change in fundamentals over the past year. Does it not make up a value buy at this price. Requesting experienced valuepickr members to throw light on this…

I cant find the link to investor conference call link , dont see any transcript after Q316 on CARE website. Can someone please share the link to latest conf call transcript?

1 Like

On quick search, I found 7 rating agencies registered with SEBI and am assuming these are also registered with RBI.

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=7

Specially, SME Ratings limited is incorporated by leading banks and on their website, one can see dedicated link given for bank loans rating. So, possibility this being one of the two required CRAs will be high.

So questions to be answered

- How much business will come to other 6 CRAs?

- How much actually big ticket loans are (> Rs. 100 crs and above) and on verge of NPAs?

- What’d be on avg. fees per rating of bank loan in such cases?

Seniors of this forum or experts please share your views.

Disc: not invested, new to value investment.

Is anyone still tracking this story?

@dd1474 thanks for your valuable inputs

I am trying to study credit agencies at a fundamental level. To me the below interview after Warren Buffet was subpoenaed is instructional:

Apart from inherent conflict of interest in business model (which I believe won’t go away), what it comes down to is Price and Laxity.

Can anybody throw some light on how much does CARE charge v/s CRISIL and whether CARE is more stringent or lax compared to CRISIL in their ratings?

Thanks

1 Like

Did some digging myself on VP: It is suggested that going from ICRA to CRISIL is like going from silver to gold. Question is what is CARE in this range: Platinum Or… ![]()

Mungerisms never hurt anybody especially on investor forums  here is the Munger answer to why Berkshire doesn’t have a great bond rating:

here is the Munger answer to why Berkshire doesn’t have a great bond rating:

Lesson: Ratings agencies are always going to be wrong in some very obvious cases

Like accountants, risk evaluators and oh …investors

Thing is: The ones that they get obviously wrong is publicized like crazy v/s the ones they were right on

1 Like

It is very difficult to substantiate which credit rating is stringent and which one is lenient. Also, depending on management pereception and growth aspiration, these perceptions may also change.

Currently, there are Seven rating agencies in India which are allowed by RBI/SEBI to give credit rating which can be used for Basel Capital adequacy calculation. This include Crisil (S&P India associate), CARE (Promoted by IDBI, now professionaly run and owned by various institution) ICRA (Moody’s India Associate), India Rating (Fitch Rating’s Indian subsidiary), SMERA (SIDBI promoted SME focussed rating agency), Brickwork and INFOMERICS (the latest rating agency approved by RBI).

In my limited undestanding, in current environment, Crisil and ICRA are most stringent, followed with India Rating, CARE, SIDBI and then Brickwork. I have no insight about work of Informerics and hence would be inapporiate on my part of give opinion on same. Please note that this is my subejctive evaluation, rather perception and it may be completely wrong.

You may do your due diligence to get more insight.

Disclosure: CARE is among my Top 10 holding with no activity in last 3 months. My view may be biased due to my holding and investor shall undertake his/her own due diligence before taking any investment decision.

10 Likes

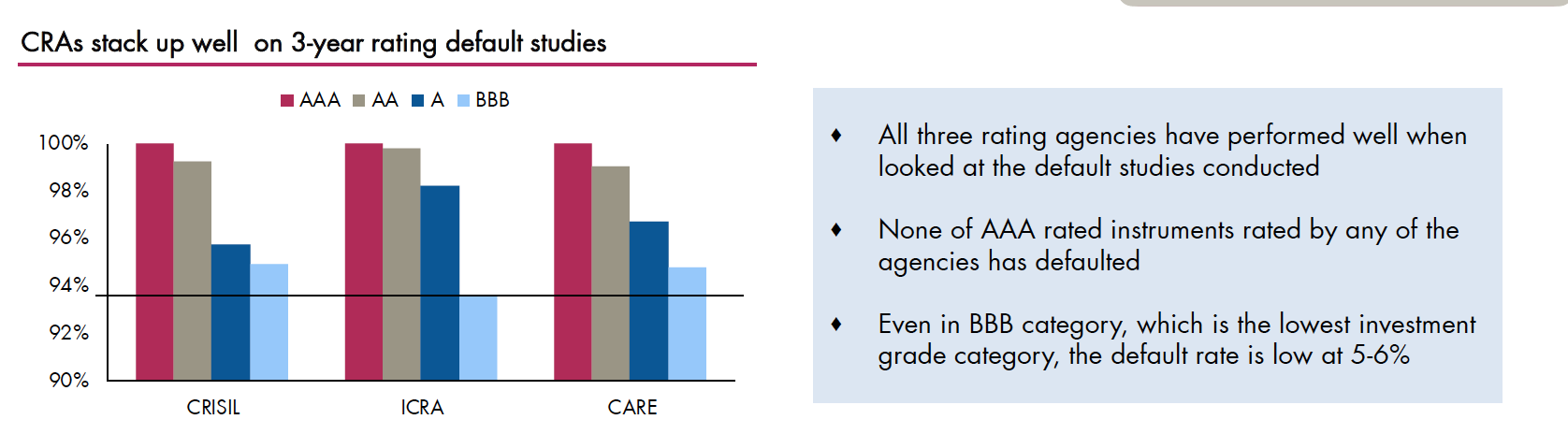

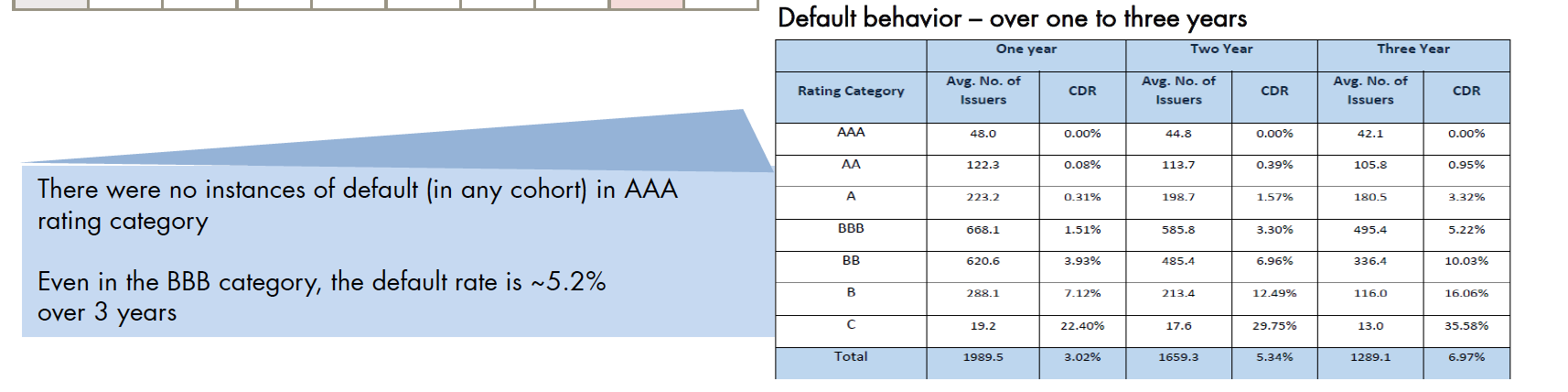

The default rates as a function of credit rating seem very similar across the agencies; which seems to indicate they are similar in this respect:

Some details for CARE:

These are from Axis Capital report below:

https://simplehai.axisdirect.in/app/index.php/insights/reports/downloadReport/file/Credit+Rating+Agencies+-+Sector+Report+-+Axis+Direct+-+22012018_22-01-2018_14.pdf/type/sector

7 Likes