Hi Aman are you still tracking CARE? I was curious why it’s at such a discount vs icra and crisis. I understand it’s less diversified and growing slower. But also has better ROE. Any thoughts would be helpful. Thanks

Did anyone attend the conf call today

is the result out? I can’t find it

What a joke!! - Received the ‘Fastest Growing Indian Company Excellence

Award’ at International Achievers Conference, Bangkok.

Hi v4value,

Have been tracking it passively only. According to me. reason for discounts are two fold:-

-

More cyclicality in business compared to likes of ICRA and CRISIL has research house as well as other business segments.

-

MNC parent vs PSU parent

In my opinion, rather than CARE being undervalued I feel others are overvalued. One of the strange things that is still prevalent in Indian markets is the premium we give to MNC companies. In 80’s o 90’s it was justified given their superior return ratios and policy of not withholding cash in their balance sheet, but now with most of the Indian companies following similar practices I think it has became a bias in Indian markets. You can see similar thing in other sectors as well

7 Likes

That makes a lotof sense Aman, thanks for your response. I guess the bull case then would be cyclical earning recovery + multiple catch up. Bear case would be MNC multiple collapsing and weak cycle continuing. Guess at 700 risk reward will look better.

Superior return values is one part of the story why MNCs were overvalued. The other part is the trust premium Indian investors placed in “phoren” companies. With few exceptions, the trust on Indian companies has been abysmally low and decades of scamming, low transparency and dubious promoters left investors with little choice than to buy the toothpaste and soaps companies. Over years, two things changed.

The Enrons showed that the wolves of wall street were no less crooked than the wheelerdealers of Dalal Street. And the second game changer has been when the IT companies of 90s-2000s like Infosys, TCS, Wipros showed Indian companies could be as clean as the best of global companies. Now there is a conscious effort on part of Indian companies to be cognizant of clean & ethical practices, because in the long run, the wealth creation of such companies more than compensates the short-cuts promoters may be tempted to take.

Would today’s investors trust a Mahindra or Tata Motors more than Volkswagen, or as much as a Daimler and pay a higher valuation? Why not? A Page or a Eicher commands as much a premium as a Honeywell, and Godrej consumer is as much a jewel in the portfolio as HUL used to be.,

I guess this MNC/Desi discussion was a bit of a tangent to the main discussion on CARE, but still not completely irrelevant. Once CARE has better investors than current ones, it is possible that the valuation improves, not as a stand-alone factor, because it will be driven by better company performance. An MNC holding in CARE will enable that, not merely as a vote of confidence in ROI provided by the investment, but allowing enhanced opportunities both in India and overseas via tie-ups.

1 Like

Sat through the call, and it looks like FY17-18 could be good years. Apologies for rather laymanish language

Most FMPs are maturing this year, and some in FY18. That should bump up bottom line quite significantly. Could lead to big Dividend Payouts?

SME subsidy is back in this budget, and they are looking corner a big share. In fact, they are expanding the SME team from 250 to 500 minimum by 2nd Quarter

ARC rating should breakeven in 1-2 years

Kalypto did 14.7 crores and Net Profit of 2.5 crores

Manish Bhandari from Vallum caused a bit of a stir by saying CARE is pretty generous compared ICRA & CRISIL when it comes to ratings. Management seemed quite upset. They decided to take if offline.

Invested at 1,400 - will hold for another year.

2 Likes

Umang replying to Umang

Joke apart, I worked at Crisil and trust me CARE more generous in ratings then Crisil.

My takes on the discussions:

-

CARE is trading inline with what it should trade at (ie correct multiple) see the growth there no growth in CARE its cyclical more dependant ono BLR and SME ratings.

-

Creidt offtake is poor in the industry, till that improves CARE wont do well

-

Next two years are expected to be much better than the past two so I believe driven by a low base and a better economic activity there would be a better credit offtake and hence better business for CARE.

-

But the risk is BLR business comes from PSU and if they are not recapitalized they wont be able to lend and less business from them.

-

I am not sure about FMP aint they MTM ?

-

Although I am invested into CARE but there are better bets in the market (unless you get a bargain)

2 Likes

Hello!!

Hello!!

They were quite clear on FMPs coming in this year & next. I think FY 18 onwards they are MTM

I think there is an investment case for care. Rating is good asset light business with good return ratio and good dividend yield as company don’t need money for investment. Reasonable vàluation at 25 PE compared to lofty valuation given to other two agencies. Overall credit will grow with the economy and care will have its fare share. Company is gaining good traction with fund managers and many marquee funds dsp black rock, reliance, mirae have invested. It has been recommended by one stock recommendation service last year. Interest of guys like Manish bhandari is also positive in my opinion as he is not an analyst who has to prepare a research report. He must be evaluating for investment by vellum. All in all seems like a good bet.

1 Like

Any opinion about the earnings numbers announced on 05aug?

Hi…was going through CARE numbers. Some key learnings on yoy basis are

- Rating Revenue 18%

- Operating profit 49%

- 555 new clients added in the quarter. Thats almost 8 per working day👍🏼

- Despite increase in clients…employees reduced from 627 to 569

- Total volume of debt rated up by 50% yoy

- Despite increase in rating revenue by 18%, expenses down by 10%

- Ebitda margin from 52% to 63%

- Pat margin from 34% to 41%

- New MD chosen. Rajesh Mokashi is a mba + engineer + cfa …ex kotak /otis / dsp. Definitely someone who understands market expectations.

- Q2 is traditionally been a great period where pat jumps 100% over q1 in past 2 years

These results are to be seen in the background of sluggish credit off-take.

Disclosure : Invested.

1 Like

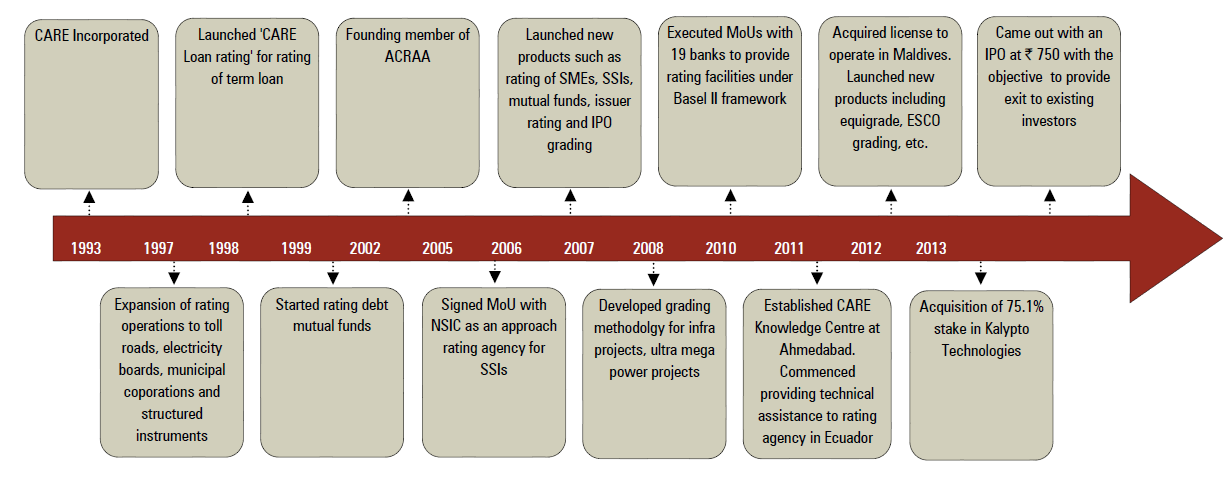

Background:

CARE is second largest Credit rating agency, promoted by IDBI Bank, Canara Bank and other FI during 1993. The company is third credit rating agency being promoter, First being Crisil (Now owned by S&P) in 1987 and ICRA (Now owned by Moody’s) in 1991. Subsequently, 3 more companies, given Credit Rating license by SEBI which is India Rating (Owned by Fitch) in 1996, and Brickwork and SMERA which began rating business in 2008.

Source: ICICI Securities

Key financials:

http://www.screener.in/company/CARERATING/

Industry:

Over the past years, Regulation has played major role in development of rating business. In 1992, credit rating became mandatory for issuance of debt instrument with maturity/converability of 18 months and more. Subsequently, RBI guideline made rating mandatory for issuance of commercial paper and issue by public deposit by NBFCs.

In 2003, SEBI made rating mandatory for debt instruments placed under private placement basis and having maturity more than one year or more which were proposed to be listed. There was also regulation related to certain class of investors to invest not more than a stipulated part of their portfolio in unrated bonds.

Further with Basel II, RBI introduced a phased approach to adopt a “standarised approach” for credit risk, Under the standarised approach, RBI recognised certain credit rating agencies as eligible credit rating agencies and Indian banks were required to use such eligible credit rating agencies to access their credit risk in order to determine capital adequacy.

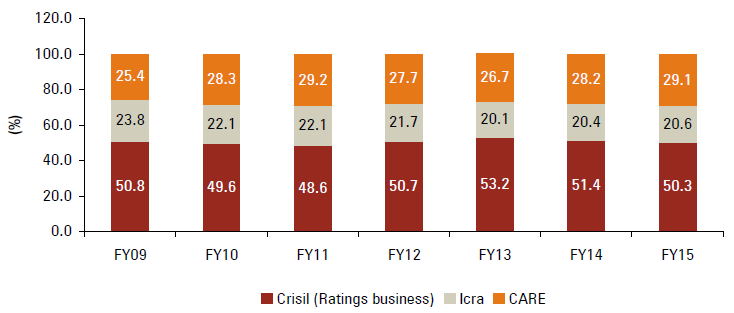

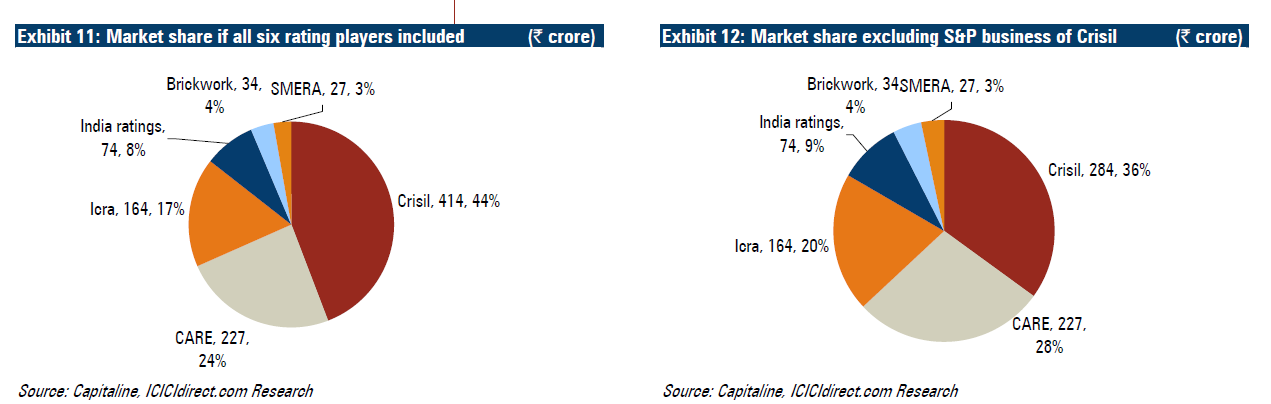

Past performance of CARE:

Source: ICICI Securities

Over last few years, CARE increases its market share as shown in image above. It has remained second largest player in Indian credit rating industry since FY2009.

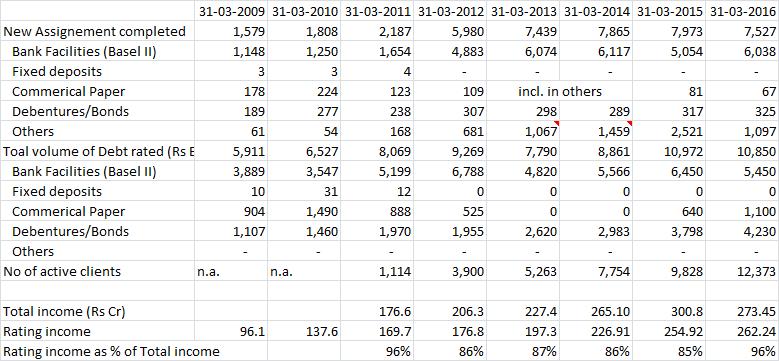

Past Growth driver for CARE:

During last 7 years, Basel II driven Bank loan rating was a major growth driver for CARE. It is pertinent to note that while number of assignment has gone up at CAGR of 27% during FY09 to FY16 from Bank Facilities, in value term same growth is 8%. Debenture/Bond (assumed now shown as Long term instruments) has shown only CAGR growth of only 8% p.a. for no. of assignment, same has grown in value terms at CAGR of 21% p.a. Please note that FY09 to FY12 data was shown as Debenture/Bonds which are presented as Long term instrument from FY13 to FY16. The above analysis assumes that Debenture/Bonds are same as Long term instrument, and Commercial Paper is same as Short term instruments.

Future Prospect:

Corporate Bond Market: Future growth driver:

https://www.crisil.com/bond-market/pdf/Are-Stars-Aligning-for-Growth-of-Corporate-Bond-Market-in-India.pdf

The broad factor driving Indian bond market is very well explained in the document. Slide 15 in the presentation give major change in bond market.

Further, in above link, please refer to Page 38 which provides Indian Debt as per cent of GDP as against Global peer. India Corporate debt to GDP is around 17% of GDP as on Dec 31 2015 as against 20% of China, 123% of US, 44% of Malaysia. During 2010 to 2015, same has grown from 10.31% of GDP to 17% of GDP.

Risk Factors:

- Change in Management: CARE is undergoing a major change with Mr. Dogra retiring from the company from August 2016. Mr. Dogra has been associated with the company since inception. The new MD Mr. Rajesh Mokashi has also been associated with the company since inception. However, Mr. Dogra was very good marketer as per industry sources and one need to see how company manage this change in guard.

- High employee attrition: As per sources, the attrition in CARE is very high at entry level. The stable middle and Top management kind of provide stability to the operations, however, given the importance of manpower, the company face problem in case attrition rate continue to remain low. In case the company increase salary to align pay at entry level with its peer, then the operating margins which are highest among the credit rating players would likely to decline.

- Shift to Internal Rating Based Credit risk Approach: As explained earlier, implementation of BASEL II, was the main driver for rating revenue growth for the company. CARE derive around half of rating revenue from BLR segment as per brocker estimate, which is around 11% for Crisil and 25% for ICRA (broker estimate). In the event the bank opt for IRB, then CARE would have maximum problem among all industry players and also need to look at other segments to maintain its revenue and profitability.

- Regulatory risk: Approval from regulator has been key entry barrier in the industry. However, the recent defaults among emerging corporates with credit rating range from A- to BBB-, may adversely affect the performance of player. CARE is among large players in this segment and any regulatory adverse action would have major impact on the performance of the company.

Disclaimer:

I have recently purchased CARE shares in my portfolio and hence my views may be biased. The investor is requested to do its own due diligence before taking any investment decision.

13 Likes

New Change in RBI regulation is expected to bring around 25% of borrower from Banking sector to come for rating agency. The number of borrower around 2000-3000 companies to come under rating purview as per interview of Mr. Mokashi Interview to CNBC today.

1 Like

Mr Dhiraj, would it call for more business to all rating agencies ?

I am unable to understand entire business spectrum of care. In the concall, they keep on talking about the bank loan rating. My understanding is rating is done by corporates when they raise money and floats debt instruments. Is it even when a company takes a loan from a bank, the bank does a credit rating for the loan amount and check credit worthiness of the company and assigns a rating for this loan tranch.?

Now coming to new guidlines, how exactly it will benefit credit rating companies, is not clear. would be beneficial if mr. Dhiraj @dd1474 can just explain.

RBI Has stipulated risk weightage based on rating given to borrowers of bank. A borrower with AAA rating (strongest credit profile) would get around 10% risk weight. So bank giving rs 100 loan to such borrower need to keep only Rs 10 as risk capital. However, as rating deteriorate, risk weightage increase and hence bank need to keep more risk capital for such borrower.

In case of unrated borrower, RBI stipulated risk weightage of 100%, however for BB or lower rating, risk weightage was 150%. Hence many borrower whose credit rating deteriorated from BBB to BB or lower, cost of borrowing increased due to higher risk weightage for bank. These corporate borrower did not share information with rating agency due to which that rating was suspended.

So they got classified as unrated and got better risk weightage of 100% as against 150% weightage driven by deteriorating credit profile. Under new rule, the corporate which got rating suspended would immediately carry risk weightage of 150-200 depending on last rating. Hence, there would no incentive for borrower to get there rating suspended and all small borrower would also now get into rating domain.

I would suggest you read CARE offer document which has various weightage linked to rating and also business prospect and also presentation made by company.

Hope this clarify your doubt.

10 Likes

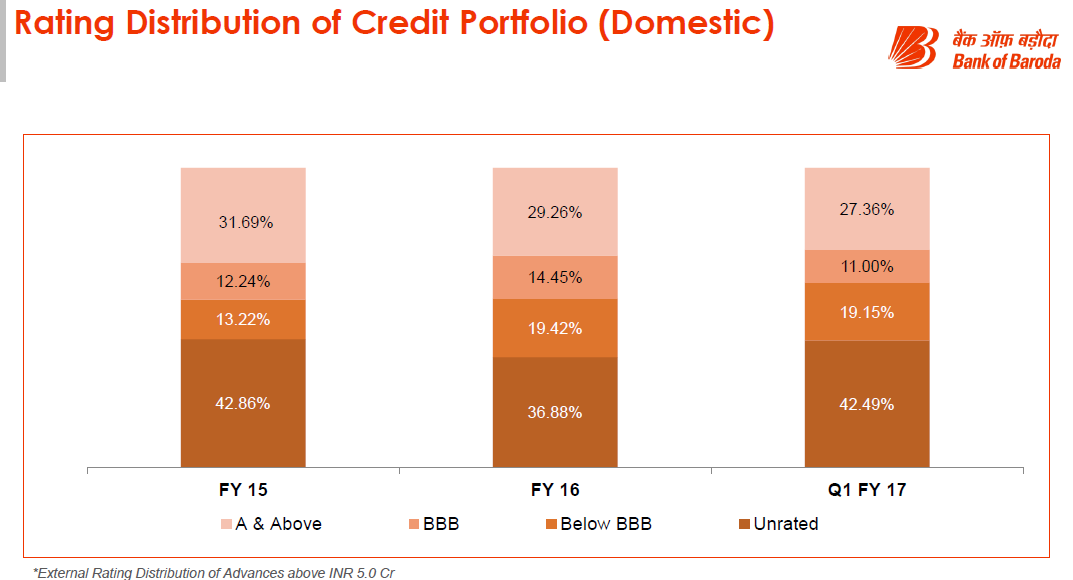

I was going through Bank of Baorda Q1FY17 presentation. Came across interesing slide about rating of domestic accounts by Bank. While not sure whether same would be case with other Public/Private Bank, it give some indication about potential of 1-2 years growth in BLR for rating industry

http://www.bankofbaroda.com/download/Analyst_Presentation_Q1_FY_2017.pdf (refer to slide 16)

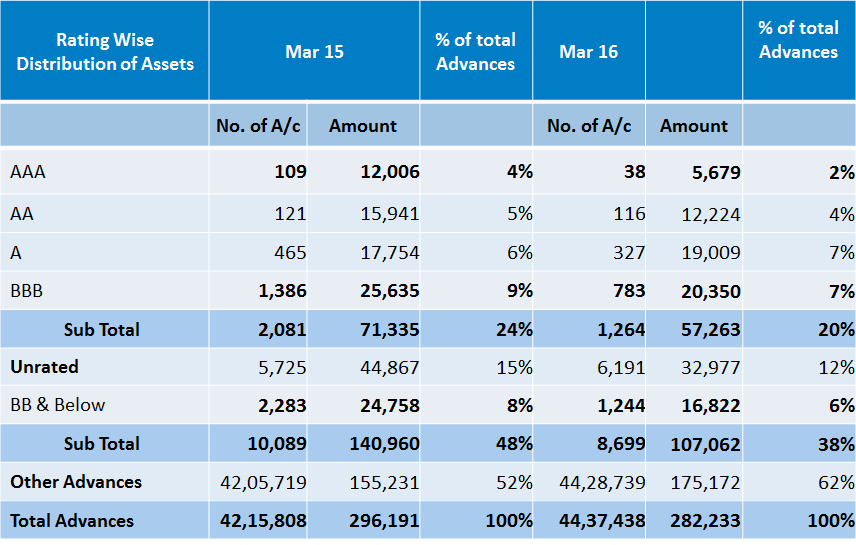

Similarly, find enclosed Bank of India Presetation for March 31 2016 results, providing details about rated accounts:

4 Likes