Yes it does. But the dividend payout is much less for a company whose ROCE>30% and postive cash flow…

Notice of Board Meeting. The details are in the notice.

@atulastra you are invested here for a long time and you also got direct contact with the management.

Any updates which you could share please?

Discl: Exited @676. No holdings now. Looking for an opportunity to re-enter.

I will wait for the outcome of the board meeting.

Edit: Although I talk to the management of the company, they don’t share any non-public information with me. Having said so, they take active interest in resolving my questions which are frequently shared on the forum. To be honest, I like this professionalism.

3 Likes

Outcome of Board Meeting - March 12th 2018

The Board of Directors of the Company at their meeting held today, deliberated the need to identify partner(s) - (technical / marketing / financial) to exploit full potential of the Company including that of liquid injectable facility—CP IV, which is approved by the Food and Drug Administration of United States of America. Further, the Board also deliberated to explore opportunities of acquiring entities which would enhance the value to all the stakeholders of the Company.

The Company’s Chairman, Managing Director, and Chief Operating Officer, have been duly authorized by the Board to explore opportunities and hold discussions with potential partner(s) in this regard.All the above proposals are subject to Board’s, Statutory and Regulatory approvals, if any, as and when required.

Thanking You,

Yours Faithfully,For Caplin Point Laboratories Limited

Company Secretary

Source: BSE India

Entering into US markets will invite the regulatory risk of USFDA. We have seen in past 2-3 yrs many quality stocks (Lupin , Sun pharma , IPCA , DIVIS etc) getting severely hammered due to USFDA.

Should we consider this risk while assigning valuation for future growth ? If yes, how much ? How much revenue/profits they are expecting from US in next 3-4 years. Would appreciate if people can share thier views on this.

Disc : Invested

@atulastraji,I am a new boarder in this forum, Going theough Caplin thread and have same question which @Rohitsharma have ,To me till now Caplin does not have any risk from USFDA but as usfda profit is going to include fom fy19 , fear of usfda will be there but it seems as the profit percentage generated from US market will be still less , then it should not be consider as big risk. Please correct if I am wrong. Senior boarders Requesting you to please put your views

Dear Ranjan ji,

The profit contribution from US wont be big initially, if you have read the annual report of the company. They plan to make FY16 top line as bottom line for FY22 ie 240cr bottom line and substantial portion of revenues to come from regulated markets which i assume should not be less than 40%…

We are currently at rs109crs for 9M fy18. Considering the points mentioned above and operational performance of the company, I am hopeful they will be able to achieve this number much before than the actual target of FY22.

Having put up the rozy picture, stock is trading at 20X+ of book value and 10X of annual sales making it fairly expensive stocks even if the PE of the company does not look bad.

Hope above points might help in your investment decisions.

Disc: Vested interest and biased views

5 Likes

Interesting development this :

Caplin COO Vivek Partheeban appointed Honorary Consul of Guatemala in Chennai

Wanted to invest in this company this year. But company is changing its business plan. Instead of concentrating in Africa, company is in the process of exporting to the US where the margins are low and competition is tough. The company is also looking for an acquisition. Considering the risks, I decided to avoid investment in the short term. Looking back at the 10 year performance of this company, the company seems to have come out of a bad debt situation and seems to be looking for trouble again, by abandoning their successful formula.

1 Like

Results Declared . Doesn’t look so good this time. Trade receivables has increased YOY in balance sheet. Any one knows the reason for this, As far as I remember they use to have negative working capital and customer advances. Than why receivables has shown an increase.

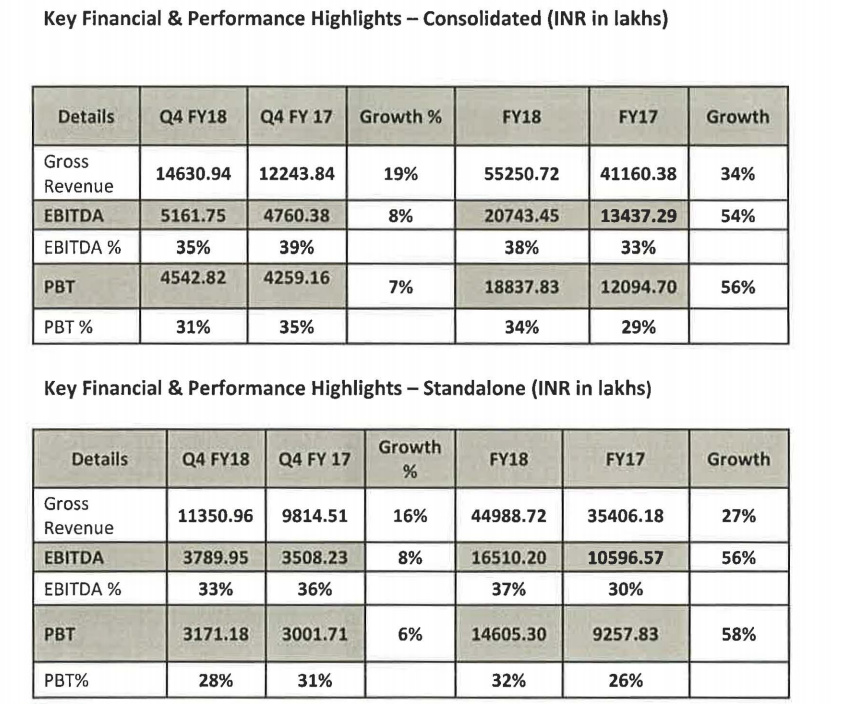

Financial (consolidated)

…* / Top line crossing INR SOOcr mark - 34% growth over previous year

-

…/ Increase in Contribution Margin by INR 82cr - growth of 40% - higher than top

-

line growth .

-

…/ Contribution% increased from 53 to 55 - 2 % on account of higher contribution

-

from manufactured products ( accounting for 60 % of growth in Revenue) .

-

…/ Opex increase only by INR 20.3 er (cash opex by INR 14.6 er and depreciation by

-

INR 5. 7 er). Opex as a% of Revenue decreased by 3 % (26 to 23) despite

-

quantum increase of INR 20cr .

-

…/ PBT grew by INR 67 er (121 to 188) - 56% growth over previous year. PBT as a

-

% of Revenue jumped from 29 % to 34 %

-

…/ PAT registered a growth of INR 49 er over previous year .

-

…/ EPS grew by 52% - from INR 12.65 to 19.26 - second successive year

-

registering> 50 % YOY growth .

-

…/ Company invested close to INR 52 er in Fixed Assets. One Third of Cash Profits

-

invested in Fixed Assets .

-

…/ R & D spend at 23 % of PAT, with continued focus on new product development

-

…/ ROE at 50% (despite an increase of INR 120 er in the Average Capital Employed

-

over previous year) .

-

…/ Debt-free Company (having Cash & Cash equivalents of INR 125cr, up from

-

110cr the previous year) .

-

…/ Current asset management :

-

• Less than 60 days consumption as inventory

-

• Trade receivables - INR 126cr represent 86 days sales

Non-Financial -

Emer~n~ Markets

-

…/ Commercial entries into Chile, Paraguay, Panama and Costa Rica .

-

…/ Geographical Revenue Breakup : Latin America - 85%, Africa - 13%, US &

-

other markets - 2% .

-

…/ New Liquid Injectable plant at CP 1 to be completed within the coming months,

-

for Emerging markets. This facility is capable of manufacturing Injectables in

-

Vials, Ampoules, Pre-Filled Syringes and Lyophilized Vials .

-

…/ Long Acting niche injectables under development, including emulsion and

-

liposomal formulations.

-

Recent launches of products in niche segments such as Pharma Softgels,

-

Suppositories and Branded/OTC range contributes to growth.

-

Plans underway to start a Clinical Research Organisation (‘CRO’) wing of

-

Caplin, initially targeted at emerging markets, with mid-term plans to target

-

Regulated markets such as US. One of the few companies in our size segment

-

to go for own CRO operations. To become a commercial revenue generating

-

operation over a period of time .

-

./ Awarded as “Emerging Company of 2018” by Economic Times Family

-

Business Awards and “Best SME with Global Footprints” by ET Now,

-

National Productivity Council and Arrucus Media.

-

Re1mlated Markets

-

./ Two ANDAs approved, one commercialized and one about to be

-

commercialized in the coming months .

-

./ 3 AND As filed and accepted for review, of which 2 are under Caplin’s name .

-

./ 7 more ANDAs targeted for filing under Caplin’s name in FY 2018/19 .

-

./ Targeting 7 product filings in Brazil in the next 18 months .

-

./ Plans underway to ramp up production capacity from CP-IV, regulated market

-

plant, targeting 60 million units from Phase 1.

-

./ Targeting a revenue mix of own ANDAs and Contract Manufacturing .

-

./ R & D strength increased by another over 30% from last year to 180 scientists.

-

R&D facility upgraded to 3x the size.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7e2f49b8-5d32-48d4-b3a5-9d7f46ede822.pdf

3 Likes

Return ratios for Caplin continue to be extraordinary. ROCE of 60% (I take the more conservative PAT/(NFA + WIP+ Inventory + Receivables - Payables). If one takes EBIT/(capital employed), the figure will be 77%.

Return on equity at 50% is also great (using average networth of last 2 yrs).

The only thing missing is growth. However, the hope is that with investments in a new injectable plant, entry into regulated markets with injectable, growth should return.

P/E of 29x does not seem out of place for this company. But it will surely test the patience of investors.

2 Likes

Their is a v high increase of trade receivables this year compared to previous years. What could be the reason ? Are they selling on credit now ?

1 Like

They are giving credit. But despite giving a 90 day credit, the return ratios are extraordinary. That is the best part.

1 Like

This is possible when foreign subsidiary payment received by Indian parent company with delay sometimes to hedge foreign currency fluctuations…you will find such in torrent pharma and other pharma companies having foreign subsidiary

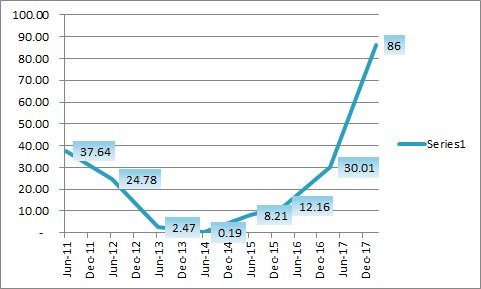

I plotted a simple graph for debtors days (taken from screener.in , last entry (86 days is from yesterdays results)) in last few years. You will see that their is a sudden increase this year , which is the cause of my worry (if the sales are real) , plus their is v low growth this quarter.

I hope these sales are real and they will receive the cash for these. If someone attends the con call , kindly clarify this with management.

I think it is time to accept that debtors are going to be around 90 days like any normal business.

The comforting part is that despite increase in debtors, it remains a nil debt company (in fact, with cash of around Rs 120 cr). And with great ROCE, ROE.

The real upside will be when they start selling their injectables in the US market. Have invested a lot in the plant, I think a huge amount of money is required every year to even maintain the injectable plant to USDFA specs. So funds are being spent on the plant while revenues have to yet commence. Lets see how the future unfolds.

1 Like

Just an observation… Return ratios can be made to look great by giving long credit terms… Better to look for croic…and free cash flows…

My first post in this thread…this stock is in my shortlist…No investment as on date… After looking at the rise in receivables in this quarter - I want to be cautious…

1 Like

Regarding trade receivables

If you look standalone result - Trade receivable upward from 3.20 to 86.35 cr while in consolidated result it 33.02 to 125.88 cr. Hence, if you deduct 125.88 - 86.35 = 39.53 cr ( from previous year 33.02-3.20 = 29.82 cr). Hence, there is no significant trade receivables as money is with foreign subsidiaries which might be for currency hedge!

However, someone should call management and get their input on this issue? Once if any one has feedback from management, request to post here the same

1 Like

Than why this aberration in this year only. In this year only such a high rise in receivables is seen. If you see debtors days for last 5 years its around avg 20-30 days ,than sudden rise to 86 days. The scenario which you are saying should be applicable in previous years also…right ?

1 Like

rvetri

It is good to analyze threadbare of what is happening on the balance sheet. Will give us more clarity on how the business has done in FY2018.

Net fixed assets (including wip) is up Rs 29 cr

Inventory is up Rs 6 cr

Receivables are up Rs 93 cr

Despite the sharp increase in receivables, total liquid cash is up Rs 14 cr

(investments up Rs 28 cr, cash up Rs 19 cr and bank balance down Rs 33 cr).

The above is without taking any debt (remains a nil debt company & paid Rs 40 cr as tax).

The surprise in the pack remains their injectables business where they have invested a lot of money, got USFDA plant inspection approval but not yet started sales to the US. Remember, this plant has been set up without taking any debt. Incidentally, they are setting up another injectable plant for non regulated markets, again without taking on any debt.

Lets see how this story unfolds. In the last management calls a few months back (Nov 2017), they guided for 20% -25% pat growth in bottom line. They have done 51% pat growth this year. I do like companies who under promise and over achieve (they could well have guided a 50% growth but stuck to their 20%-25% growth guidance). Leaving aside growth analysis quarter se quarter tak, 20% annual growth should be possible.

Incidentally, in the management call attached, they did mention about receivables cycle going up as they are getting into OTC products, soft gel and wellness categories where the receivables are higher but margins are better. This is actually borne out by the fact that ebitda margins are up from 32% last year to 37% this year.

3 Likes