Paragon is managed by Sid parekh son of deepak parekh. Capacite bags all the contracts of oberoi. HDFC is the prime lender to Oberoi.

This came to my mind, when i realised such a young company faring out so well and having the rich clientele in no time.

Pls do not comnect any Dots… Lots of difficulty with this company, poor cash flow n total mismanagement. Do not go only by order value… Chk weather they have able to pay to vendors or not. Many orders are cancelled due to delay execution. Nobody declares that to exchange. Pls do not waste yr time after this stock. I posted this msg before 2.5 years also when stock price was 450.

Despite clear linkage with Pratibha Industries, many investors ignored this and trusted the company. This again proves the fact that management integrity is as important as thier execution capabilities.

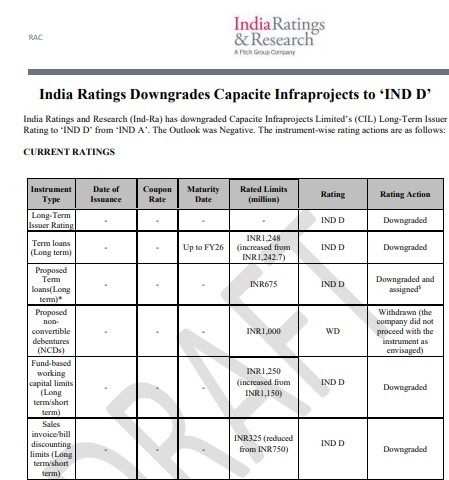

India ratings has downgraded the credit rating to ‘D’

(I.e.default) yesterday

Valuepickr members have done a commendable work of identifying the linkages & other issues and highlighting them from beginning. This is the reason, reading entire thread of valuepickr is compulsory part of my research process before I invest in any small/mid cap.

Looks like this was a technical default while rolling over loans in ECLGS 2.0 scheme post COVID, and Ind Ratings is trying to do a CYA (Cover your A…).

The company’s debt is at a managable 165 Crore and 280 crore on a net and gross basis respectively. Please read the IND RA report before panicking.

To my surprise, management reached out to another rating agency for fair rating . This just shows how impatient the management is about stock prices. In the last 3 years, PSP projects did much better than Capacite. Based on ky understanding of the management, they talk so high but deliver low.

So many flaws noted in their execution ability. They always talk about orderbook, revenues increasing, however, profits and cashflows god knows when they will talk about it. Pre-Ipo, their financials were growing at massive rates, post-Ipo growth vanished. Every quarter they complain of some or the other issue and show brighter picture, which doesn’t come.

This year could be much better as their biggest government project is getting executed. However, management failed to excite me. This made me book losses and find alternative opportunity.

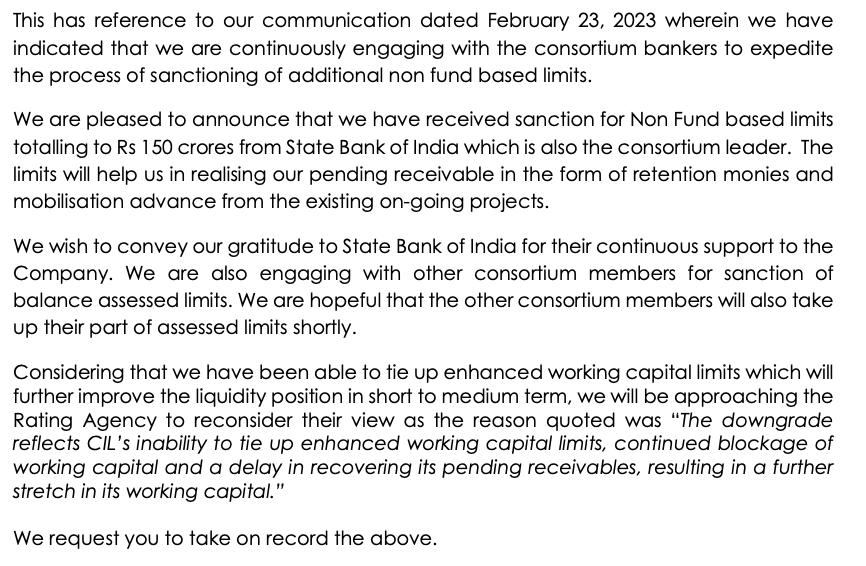

Credit rating upgrade is expected by Q2FY24. The company was able to secure bank guarantees of Rs. 150 Cr from SBI during Q4FY23. Further, Rs. 250 Cr are expected before Q2FY24.

Order book stands at Rs. 9513 crores till Q4FY23 (Public: 70%; Private: 30%). The guidance for FY24 is to maintain it at par with revenue guidance level atleast.

Last year revenue was Rs. 1791 vs order book of Rs. 3400+ Cr.

Working capital days to reduce by 20, bringing it down to 85 days(ex- retention money).

Current asset turn is 4.23x. The expectation is to improve it to 4.75X during FY24.

Around 150 Cr. of depreciation will be done in next 8 quarters besides the regular depreciation. It will come down to Rs. 50 Cr on annual basis, and will be comparable to the industry peers after 2 years.

One time tax expense of Rs. 6.64 in Q4FY23, and it is non-recurring.

Substantial settlements which have been written-off earlier are expected to be accrued to the bottom line in next 7-8 quarters.

Enabling resolution has been taken for the QIB, and then it is upto the management to avail it or not. The decision will depend on the future growth prospects of the company.

I believe the bad times for Capacite are over and it will show good growth in the medium term.

Looks like Ratings have now been changed to stable from negative implications. There was mention in con call that ratings upgrade will happen but since the outlook alone is changed for now is this negative for the company?

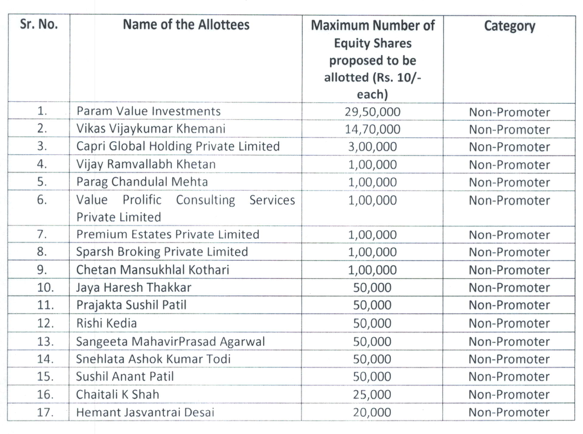

AGM on 21st September. One of the item to be discussed is raising of current authorised share capital from 80,00,00,000 to 90,00,00,000 by issuing 1,00,00,000 shares. Please share some information on how this might be alloted.

Authorised capital is the total shares the company can have. That is it cannot issue more than the authorised number of shares. No shares will be issued at this stage.

. This just shows how impatient the management is about stock prices. In the last 3 years, PSP projects did much better than Capacite. Based on ky understanding of the management, they talk so high but deliver low.

. This just shows how impatient the management is about stock prices. In the last 3 years, PSP projects did much better than Capacite. Based on ky understanding of the management, they talk so high but deliver low.