Tgt. achieved means network target achieved. (the column to the left is called tgt. and has total network numbers in it).

Well established branches may be able to generate incremental business. But for that, the company first needs to establish a new branch. Hence the emphasis on network growth.

I’m not sure how accurate is the company’s assessment regarding competition because competition is not new to the housing finance industry. Despite that, they were able to grow up until a year ago when RERA reared its head in Karnataka.

As regards Karnataka, RERA doesn’t seem to have matured yet. This should take another quarter or two may be (company has also indicated a pick up from Q3 onwards). However, the positive in the network expansion is that 14 out of the 15 new branches opened in July are in high growth areas outside KN or areas where RERA has stabilised. Hence, the Karnataka impact should come down slowly.

Point taken. Adding new branches will be a stepping stone to achieving the AUM growth

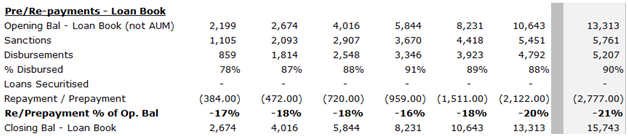

Pre/Repayment in Loan Book of Canfin clearly showing signs of rise- which is due to rise in competition resulting in balance trf. Pls note that Canfin’s rates are @ 40 bps premium to the large HFC and hence higher risk of trf. Banks due to their NPA issues on corporate side - have not been able to grow their corporate loan book and hence have focused on Housing Finance

As highlighted in yellow below, the non-food credit growth by Banks post FY 15 have been in single digits Vs Housing credit which has grown in double digits. So, I do think there is some truth in the management stating that growth has suffered due to banks and other large NBFC’s getting aggressive. While % growth in the Housing credit is similar to the past years - absolute disbursal have been rising on YoY basis

Excellent point. My point is management states that it has supply side issues in Karnataka - which may not be resolved in a Qtr or two. I think if we can get some data point on the kind of launches happening in Karnataka in affordable category - it will help us gauge when the growth in Canfin will return. Karnataka is still 33% of the loan book.

For the past couple of years, the target kept by CANFIN was to have a loan book of around Rs 35,000 Cr for FY 2020. (Vision 2020)

This year, they have changed it to Rs. 40,000 Cr by March 31st 2022.

For the short term target as well, they set a target of Rs. 17,000 Cr for 2017-18 in the last year’s AR. They could manage to reach Rs. 15743 Cr from 13,313 Cr.

In the last year’s annual report, they mentioned that they would be opening 20 more AH centres.

This year’s AR reports only 10 being opened and they are ‘planning to open’ 10 more.

Although it is good to set high targets, it seems CANFIN has not been able to effectively deal with the implementation.

Ideally a change in their Vision 2020 ( A long-term target) should have had some explanation in the AR, but there is none.

The fund representatives from Mahindra Asset Management Company Pvt. Ltd., Reliance

Strategic Investments Ltd., Seven Canyons_ Advisors LLC, Tamohara Investment

Managers Pvt. Ltd.; DHFL Pramerica Asset Managers Pvt. Ltd., Goldman Sachs Services

Pvt. Ltd., Motilal Oswal AMC Ltd., Steadview Capital, TATA Investment Corporation Ltd.,

Ishana Capital Ltd., New Horizon Investments and Anived Portfolio Managers Pvt. Ltd.,

participated in the group meet and had one-on-one meetings with the representatives

from Flowering Tree Investment Management Pte. Ltd., Wellington Management

Company LLP and Motilal Oswal AMC Ltd.

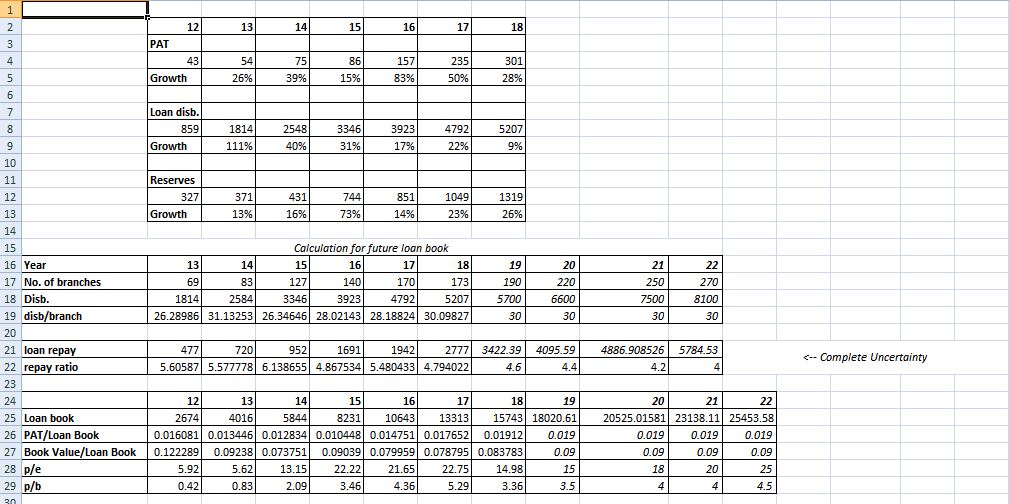

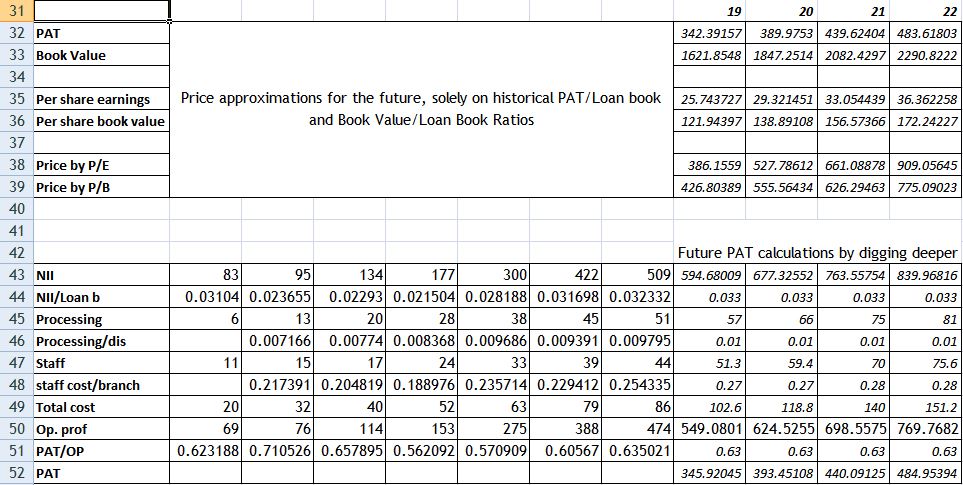

Building on the number crunching done by @Yogesh_s, I have tried to approximate future earnings and valuations.

I have done the following:

Estimated the loan disbursal per year till FY 22.

Have given a rough figure for Loan repayments solely based on the historical ratio of Loan Book of previous Year against this year’s loan repaid. I believe this is the most vague number going forward and we must keep an eye.It is difficult to estimate this as the loan maturity periods vary from 5 years to 30 years. If this increases more rapidly wrt the Loan Disbursal, the loan book will be gravely affected and hence the Net interest Income.

After coming at the estimate for the loan book for the future years, I have estimated the

i) PAT and Book Value solely based on the historical ratios for PAT/Loan Book and Book

Value/Loan Book. I have then approximated prices by P/E and P/B multiples.

ii) PAT after drilling down from Net Interest Income, considerations for processing fees, staff

costs, tax costs, etc.

I have taken a bullish outlook while considering the numbers. What is clear from this number crunching is that CANFIN can give good numbers only if it does serious branch expansion in the next 4-5 years and does not deteriorate its interest spread.

Edit:

Assumptions:

Processing charges are proportional to loan disbursal.

Staff cost is proportional to the number of branches.

Total cost is approximately double the staff cost.

I think distribution per branch should be lower. new branches will take some time to mature. Secondly, the board of the company has expanded much to included representatives from Canara Bank. Mr Hota was doing a good job before, then why such expansion of board? Is it more interference from Canara Bank? Does this mean the policy decisions will lag behind? Also, I would like to see the impact of increasing interest cost or declining spreads. Mr Hota himself specified on TV that they are facing huge competition from banks and their cost was rising / margins thinning.

Also, it will be great if you could share your excel.

While it is true that the newer branches will take time, the older branches would start out churning as well.

30 is again a bullish consideration, conservatively one can take it 27-28, given that more branches are being opened or already opened in non-South regions this year.

Is there some way to know why the change? They increased the rates in May 18 by around 50 BP approx on average and then again reduced them by 20 BP now.

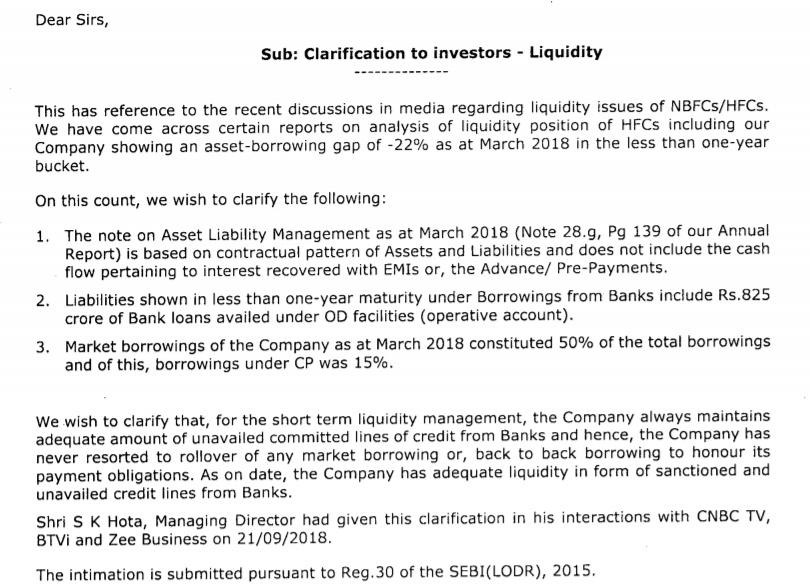

In practice, banks and NBFCs can run into liquidity issues, mainly because of asset-liability mismatches.

For Can Fin Homes, for instance, 18 per cent of its total liabilities (including bank borrowings and market borrowings) are maturing within six months, while only 5 per cent of its assets (advances and investments) are in the less than six-month bucket.

I am surprised that in such a busy, active thread, no one has updated about a quarterly result, after it came out several hours ago. I checked and re-checked before putting in the results link below…but no one updating the story also tells me, how shine on this stock has worn out so badly…

and as far as the result, at first glance, my untrained eyes say what can I say,nothing that you did not know already…flattish is the word but in all this carnage in HFCs, at least, there is nothing new to blame and drive an axe through it

Disbursements up 7% YOY.

Loan book growth up 17% YOY.

NIM, ROE and ROA have compressed slightly YOY.

Gross NPA and Net NPA % has gone up YOY…

Valuation wise, P/E is at 10, P/B is at 2.26 (compared to 5 year average P/B of 2.48).

Just holding on to my shares, neither buying nor selling. Once the competitors results are out, at least we can compare and see what’s going on overall.