Canfin homes has revised the lending rates. It starts at 8.95% now as compared to 8.5%. Quite a steep jump. Is this showing confidence in growing loan book OR just to protect margins at the cost of growth?

It was 8.5 % till last week. This change to 8.95% is very recent so we need to see what other banks / HFCs do post RBI meet. Also, perhaps they don’t want to compete in that segment of PSU banks etc. Canfin’s target segment is LIG & MIG1 - lower end and those who cannot get loans from banks and big HFCs. So, perhaps they are sticking to their niche and protect margins (not worthwhile competing with lenders with lowest lending rate)

He was also uncharacteristically absent on Twitter for the period of the March 31st to the April 4th. One would presume that he lying low all the time he was selling and surfaced back only after the disposal was done with. Nothing illegal or unethical on his part, but nevertheless a lesson to be learnt for novice investors who blindly coat tail big investors for both the buy and sell decisions.

I invested in Can Fin in August last year (which, in hindsight now, happened to be just when the stock price broke below its 50-day moving average and was witnessing a correction involving lower lows and lower highs just after failing to take out its previous top). I dumped it post-Q2 results after paying a good tuition fee. The stock’s June top, I guess, also happened to be the time around when the company first reported a serious deceleration in loan sanctions.

Moral of the story: trust price action; it generally reflects the truth about a company’s fundamentals better than any expert opinion.

Baratis left even before the marriage was to be cancelled. Investors need to have foresight and act decisively when facts change. That is the learning of the story. He is also indicating deterioration of the asset under the new management. Looks like he doesn’t trust the current lot. Anyway this risk remains with all PSUs stocks.

I had already posted in my comment the very next day that BM and others would have exited on wed/thursday (28/29th Mar) when CANFIN was sliding down. But apart from lessons for investor, we should not blindly follow their exit. Canfin has again jumped back to 450 yesterday. Make your own judgements.Following big investors can be treacherous sometimes- (Repco Home,Hawkins etc)

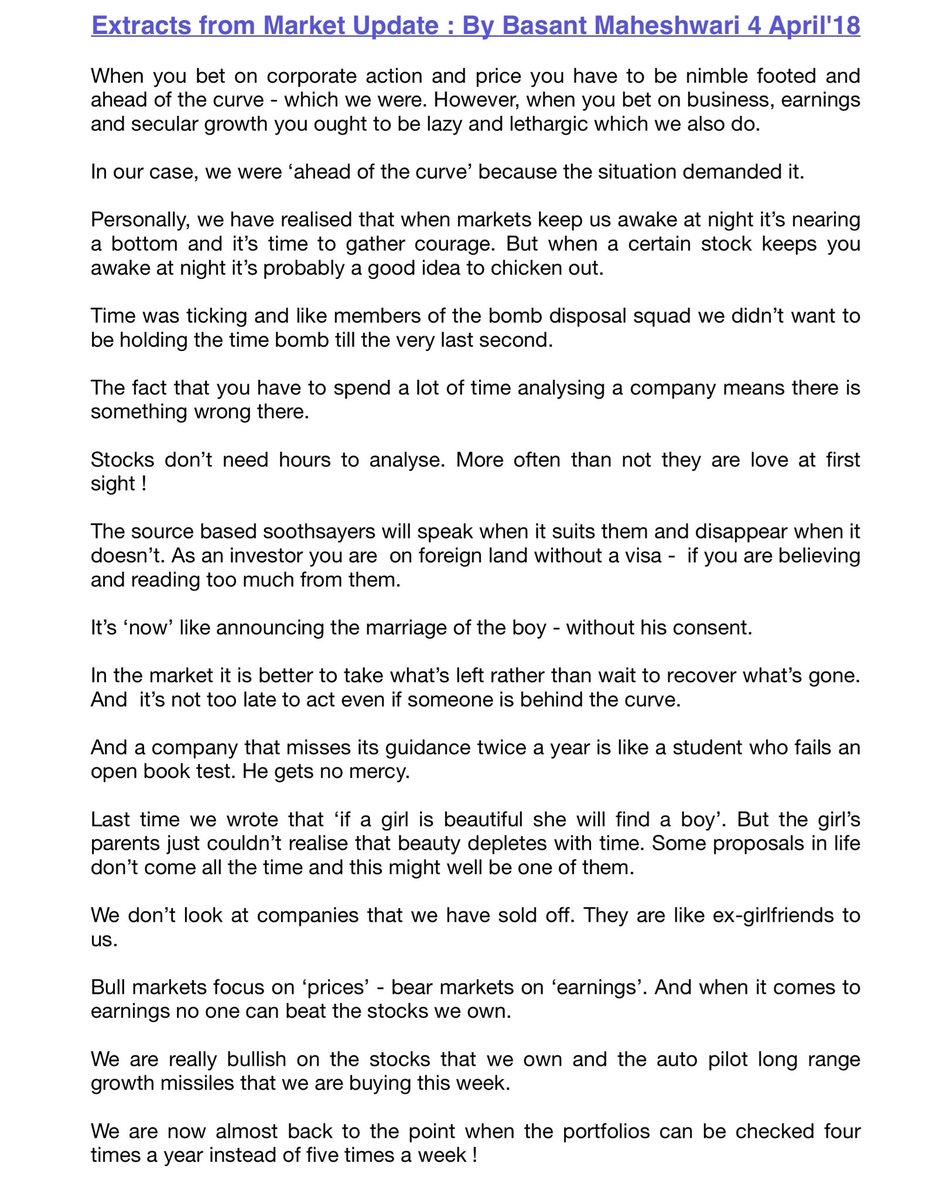

Wonder what are the auto pilot long range growth missiles, Basant had brought this week after selling canfin. Is it the other housing company he is holding?

Is Canara bank still keeping the sale process open? Listen to the Q&A at timestamp 12.40 minutes in the video where the interviewer asks Mr.Keki Mistry (1) If they are still interested in Canfin, (2) That she hears / knows that Canara bank has not concluded the process & (3) that there are reports that HDFC is interested and to that he doesn’t say that Canara bank has closed the process and gives a generic reply that they are interested in quality companies at the right price. This interview was on Apr 3rd whereas Canara bank’s announcement of stopping the process was on Mar 31.

Ignoring the noise around acquisition/stake sale, at 450 rs, at a p/e of under 18, if CanFin can maintain its growth with 22-25% ROE kind of returns, it does look attractive. The industry certainly provides a lot of headroom for growth, even for the average kind of management. IMHO the reason for selling our shares should be only if and when the growth rates on a YOY basis keep coming down…

Sobha, the Bangalore based developer reported strong sales volumes for the last quarter. Signs of realty demand in the south picking up? Could be a positive for CanFin.

Disc. Missed the 10x journey in canFin from 2014 to 2017. Invested recently in March

A lot of discussion on can fin on the board and elsewhere has only one thing that competition can hurt it. Otherwise it is well performing company with best NPA profile. If sector is growing and will keep on growing then can fin’s loan disbursement will surely grow. The company is still growing its network which is important in mid to lower segment where tag of PSU gives a trust of fair treatment. An expert cited example of Bajaj Finance that few years back a 10% holder exited just because he made good enough but see the company’s growth(or stock price growth) after exit. I think well touted investor exited as he was not the early buyer in it and so his price difference with the current one is not much. IMHO if market does not break can fin may be at place where a fresh investment can be made for few years.

Disclose: Invested when adjusted price was in double digit.

a. Loan book growth - Can it touch 16000 crores (as revised by Mr. Hota in January during Q3 results) from 15058 crores at the end of Q3? As pre/repayment would be around 740 crores, the disbursements would have to be around 1680 crores

b. NIM - Could they maintain it at Q3 levels? They did do a few high cost market borrowing at 7.5+% (so did HDFC and other institutions but now bond yields are falling - below 7.2% now)

c. NPA - Can they get Net NPA to zero as they have done in the past year ends? Can they recover all the loans as mentioned in the first quarter? Can GNPA be reduced as well?

d. Net profit - possible to get it at 84+ Crores?

Point to note: A report by Investec mentioned that management was distracted in Q4 due to the stake sale process while Mr. Hota denied it in CNBC.

Appreciate views from fellow boarders who watch the company fundamentals regularly.

Lets address some of the key points we need to monitor for Canfin

It derives 33% of the business from Karnataka & 15% from Tamil Nadu. From what I understand, Karnataka public is well read and educated society - Mr Hota has admitted this several times in the concalls. Hence, will the rise in rates result in more Balance trf. to lower cost HFC’s

Karnataka has a very large inventory of Non-Rera projects. How will these impact real estate prices in Karnataka - once all these inventories hit the market. How will this impact HFC’s in Karnataka

Is GST on under construction property - impacting demand. Govt recently exempted GST on under construction property person eligible for interest subsidy under CLSS. But others have to pay it.

I think guys, lets focus more on these fundamental issues, rather than discussing issues of who recommended it and what he should have done etc etc… It will help us build more sound knowledge of the company and sector.

Yes, better to focus on company fundamentals. I am still unable to figure out why they would increase the lending rates to start at 8.95%. Perhaps they realize that they cannot compete with banks and other HFCs at the lower rates segment and want to create a niche, like Gruh, Repco?

Guys, stick to the discussion on the company and sector. If anyone’s buying or selling decisions affects your own buy/sell decisions, then go back to the basics and re-invent your investment thesis.