Hope I have answered your comment in my previous revised reply. Actually nothing is under control. Everything is a result of some previous action. It is inappropriate to blame or praise anyone. But everything is appropriate in its time, since it is part of the entertainment.

1 Like

I hadn’t seen the revised reply by you. I’m sorry. People will always have different opinions. I respect that. Thanks for sharing your thoughts. I appreciate it. Finally, all that matters is that Can Fin does well. That’s what all shareholders wish.

1 Like

Interview of Canara bank MD to CNBC TV 18.

He mentions that the offers were above the market price but they were expecting more as a control premium. Also he said at least 5 times that the want to “strengthen” canfin business. Does he refer to fund raising by rights issue? That would make sense if the loan book growth goes above 25 - 30 %

Keki Mistry - stating clearly that it had not revised it’s offer made 15 days ago.

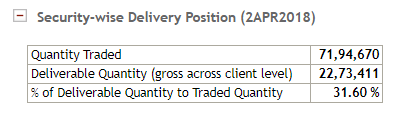

Very high delivery volume (in absolute numbers). What does this mean? Selling of big quantity by individual / HNI / funds / Institutions ?

Herd of cattle exiting. Read Baring,BM and other panic driven individuals as if the sky has fallen on Canfin.Nothing fundamentally changed now and 6m back except expectations. IMO price should climb back to 500 levels in 3/4 months time.

Discl: not sold anything still invested

2 Likes

BM - I understand. But Baring? Do you mean Baring bought recently and sold now?

Today’s interview with canfin MD. Employees of Canfin are celebrating. No targets and no capital infusion for FY19.

Check out @CNBCTV18News’s Tweet: https://twitter.com/CNBCTV18News/status/980680663278825473?s=09

1 Like

A big lesson learnt. Never buy a stock on media speculations. Owned canfin before and added a lot more after stake sale news. To be honest, I am a bit confused on if I should book the loss or wait out. I understand this forum does not offer any stock specific advice and it’s completely up to me on what to do. I am just letting it out to relieve myself.

the interview was not at all helpful for investors actually…he kept talking about the housing fin ind. on a whole and about fy19 etc but that too without any targets/numbers…not sure what conclusion to draw here…I’ve been following this guy in all his interviews/conference calls…he seems intelligent but is a typical psu-trained executive who always shies away from talking numbers…not sure if he can provide the right kind of leadership to bet on.

Mr. Hota could be happy that the sale didn’t go through as otherwise he had to move back to Canara bank and not continue as the top guy of a company

1 Like

I think the key question is whether the valuation is justified given the slowdown in the loan growth. No doubt the asset quality is excellent but growth has been quite bad over the last 4 quarters and Mr. Hota does not give much confidence that he has the hunger for growth. I have listened to a couple of con calls - his strategy appears to be over dependent on government’s housing for all. While Canfin grew exceptionally well at a time when competition in that segment wasn’t that high, with every one jumping in to the fray, situation is very different now. It will require extra ordinary leaders to stay ahead and Mr. Hota does not give that confidence. Hence I sold out today - losses in recently bought (on the hopes of hdfc buyout), but overall profit due to older holdings. I think some people knew last week and jumped out on Tuesday and Wednesday (just my interpretation looking at price movement). This is no advice to you, but just wanted to share my story.

5 Likes

The growth slowed down, yes. But it is still better than OR similar to thatbof Gruh. And Gruh trades at 20 times book whereas Canfin is at 4.3 times as on today CMP. Granted Gruh will deserve better valuation but telling canfin growth is bad is not correct. It has slowed down compared to previous years but is still at 20%. The main question atleast for me is if Canfin / Canara bank management can scale up further. Not to say they cant but just a doubt given PSU parentage legacy.

Also, if you look at the likes of the bidders (HDFC, a good set of big global PE players, Kotak bank etc), it is clear that the company and the future prospects are very good. Its just that Canara bank differed with all the bidders only on valuation.

Boys (HDFC, Banks, PEs) came to see the beautiful girl (Can Fin Homes) and the parents (Canara Bank) were eager to get the marriage fixed. But the relatives (minority share holders of CFH) were looking for mouth watering 5 star hotel treat very soon. But the parents had a tough condition which all the bridegrooms felt was onerous and walked off.

The parents came out with a announcement that they have decided not to marry-off their daughter in the next few months considering various other factors.

The relatives who were salivating for their own enjoyment got pissed off and decided to break their relationship with the family for all the disappointment caused to them.

The maids (employees) in the family who were expecting a job loss if the marriage went through rejoiced for the luck smiling at them even though they know it will not be permanent.

Meanwhile the VP moderator was so aghast that the Can Fin Homes thread was growing with lots of unnecessary posts.

29 Likes

I guess it would have been difficult for Canfin employees to suddenly shift to private company culture, especially if it was a PE player. If so, good for them. Of course, current company operational parameters already indicate the company / employees are very productive and efficient.

One thing that i absolutlty cannot comprehend is the way mkts are valuing CANFIN AND GRUH - Two companies doing a very similar business , very similar top line and bottomline [ around 1600 cr and 330 cr resp ] , at very similar NIMS s and NET PAT . But one is valueD 5 times books and the other at 21 times book !!

Of couurse HDFC managemt gets a premium. But, that cannot be more than 40 or 50 or 60% or even at best 100%, not 300% premium .

Cluesless when both will be fairly valued !! #thinkingaloud.

Note : holding both 6 % of pf .

1 Like

Comparison between Gruh Finance and Canfin are noteworthy. Sales for canfin lagged in the 2007 to 2011 period. There is no such lag for Gruh. Canfin appears to have reached a slow down period. You may notice that while the ratios for Canfin are great, those of Gruh are the best in the industry. For example RONW of 26 for Gruh against 21 for Canfin. A PSU type organisation however good cannot compete with a private one. Gruh for example gets low value orders allotted to it from HDFC without any sweat, while Canara bank doesn’t do so for Canfin. I am not saying that Gruh Finance deserves 15 times book. I am only pointing out that with its inherent advantages, Gruh finance will maintain its run rate for decades to come.

1 Like

Apt analogy. Bottomline-this girl is beautiful with or without HDFC. HFCs as a whole had a difficult year. Now the tailwind should come for this sector as PM has to build houses for his dream of housing for all. 2019 is looming, Now or Never point is coming for this scheme. There are other beautiful girls in the same community. Beauty(valuation) lies in beholder’s eye.

Disclosure- Invested in Canfin, PNB Hsg & Repco

Request Hitesh ji to guide in this prime sector HFCs.

2 Likes

Excellent analogy of daugther’s planned wedding and then cancellation. Very well drafted.

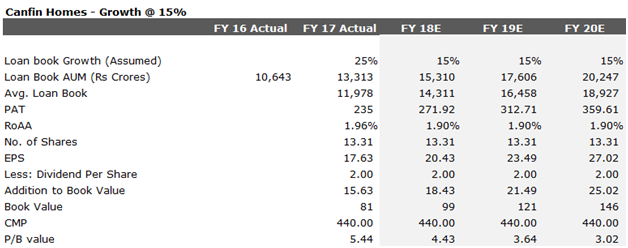

Now, as regards valuation of Canfin homes is concerned - it is an annuity business with the company receiving interest and principal in the form of EMI. So, let’s make simple back of the hand calculation and see what the valuation looks like for 1 year forward and 2 year forward.

Canfin’s Loan Book

FY 16 - Rs.10,643 Cr

FY 17 - Rs. 13,313 Cr

Avg. Loan Book - 11,978 Cr

PAT for FY 17 - Rs 235 Cr

Return on Avg. Assets (RoAA)** = PAT / Avg Loan Book

RoAA = 235 / 11,978 = 1.96%

** Canfin’s Total Assets are only marginally higher than Loan Aum, as it does not have many Investments. Hence, I have used avg Loan Book instead of Avg Total Assets, in my RoA calculation.

EPS = PAT / No. of Equity Shares

= Rs 235 Cr / 13.3 Cr Shares

= Rs 17.66

The Loan Book for 9MFY18 is Rs. 15,058 Cr - (13% growth over FY 17). Hence, one can reasonably assume that by the end of FY 18 - the loan book will grow by atleast 15% YoY - which comes to 15,310 Cr.

Now - with this background - lets extrapolate the numbers - assuming Loan book grows at moderate pace of 15% for the next 2 years also. Assuming that the RoA also drops from 1.96% to 1.9%.

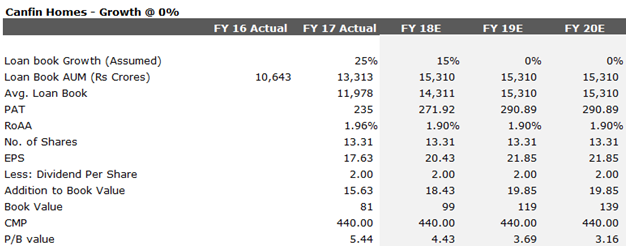

Now - someone will want to argue that even a 15% growth in loan book may appear difficult. So, in the next scenario, I have assumed 0% growth. The Book Value at 0% growth is lower only by Rs 7/- for FY 20.

Hence - either ways, for long term investors, the valuations are not strecthed, in my opinion. Pls note, that these are my assumptions and one should do one’s own calculations to arrive at fair value. Pls also note that I have invested in this stock and hence my views are biased.

Canfin Homes.xlsx (12.5 KB)

8 Likes

The market is agog with rumours that India’s largest home lender Housing Development Finance Corp has revived talks to buy out the state-owned lender’s 30 per cent stake in the once again exploring the option of buying a controlling stake in Can Fin Homes. E-mail queries to HDFC and Canara Bank on the matter went unanswered till the time of going to print.

Perhaps, this could be a reason but Canara bank is quite well capitalized as per its MD.

1 Like