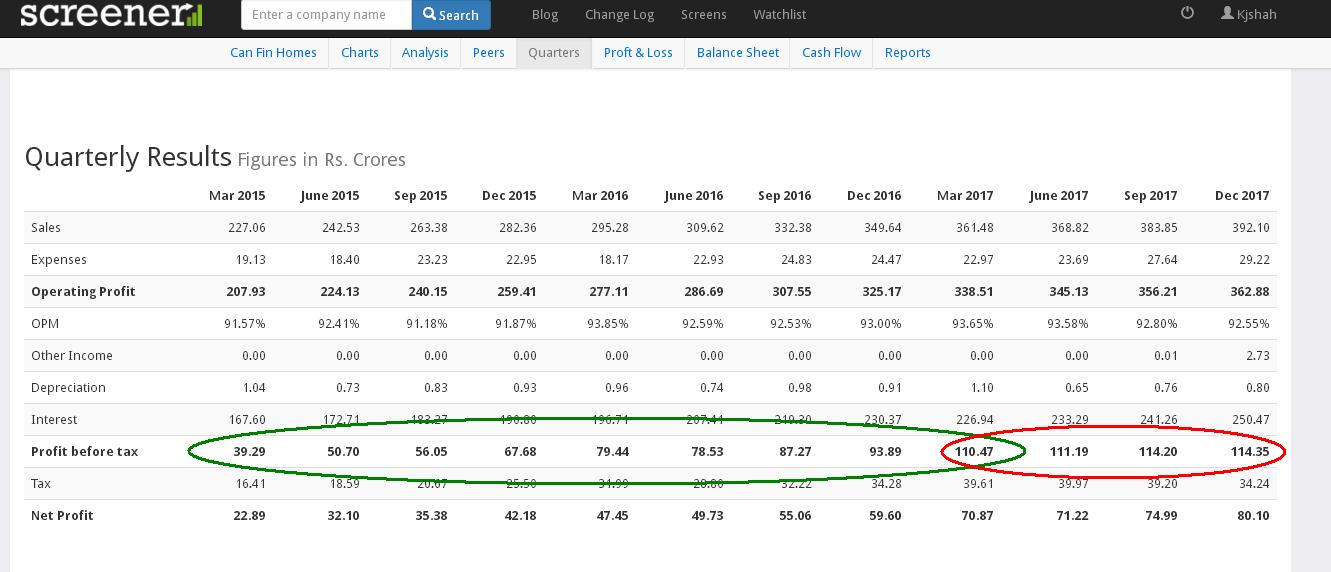

as we can see profit growth qoq was @10% (from q4fy15 PBT of 39 cr. to q4fy17 to 110 cr) but in last 4 quarters profit is stagnating (hardly any growth), mean while valuations are not very cheap at P/B @ 5 times. disbursement growth YOY is also slowing down. tailwinds(lower interest rates) are gone and with more headwinds (rising interest rates, more competition from newer and existing players) i see very little upside here. only saving grace was supposed improved performance driven by change in management or rerating .

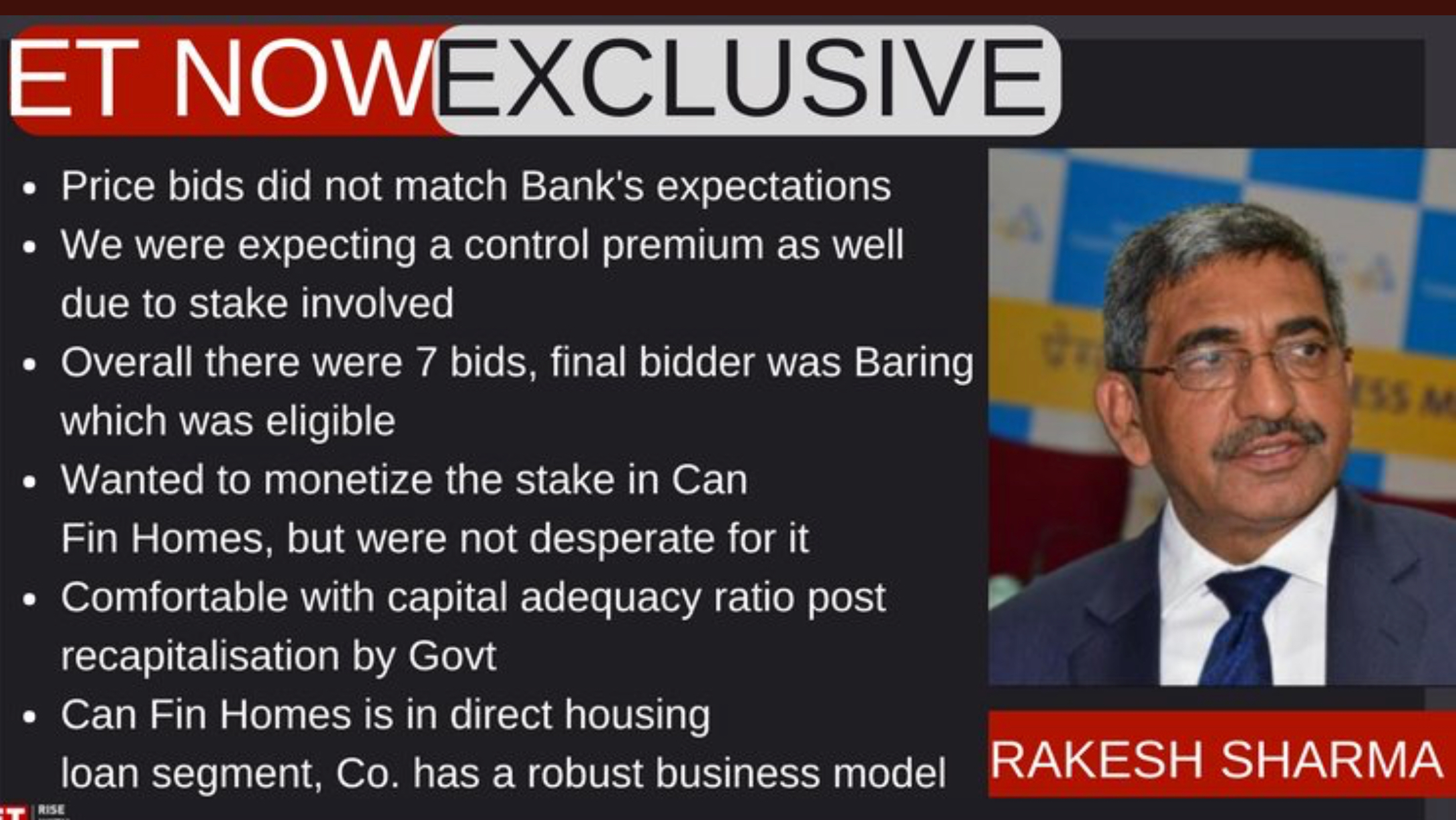

I am not sure about this interpretation. HDFC has mentioned on TV that they have indeed made an offer to buy. So no doubts on company credibility. It could probably be that the price expected by Canara bank was very high as they were not really desperate to sell their stake but were forced by Govt to sell non core assets

What does Canara bank MD mean by saying “Baring was eligible…” when they did not accept their offer as well? Does he mean Baring offer was matching expectations but Canara bank didn’t take it based on other parameters?

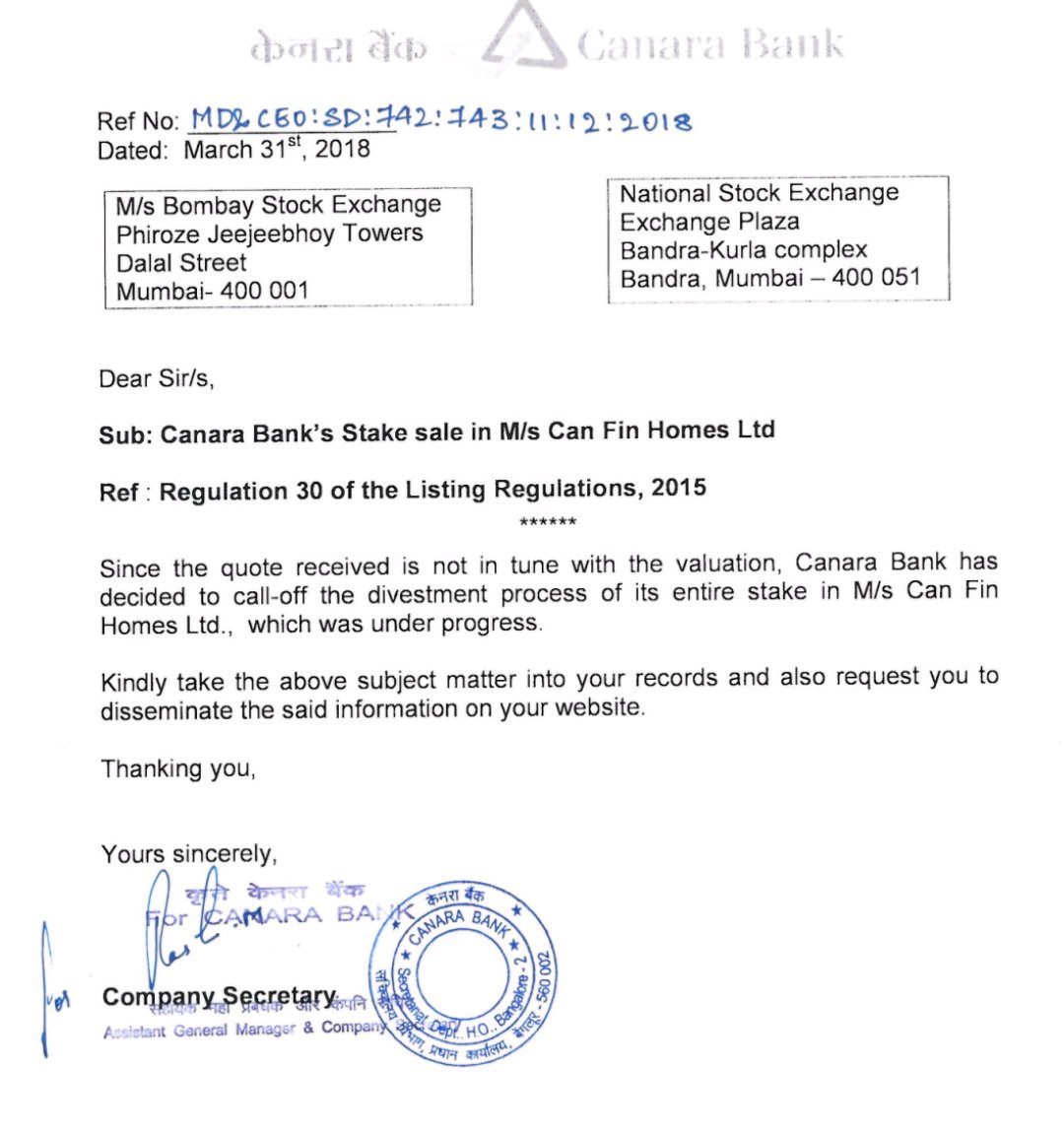

Yes it is short term negative but not very surprising. Please remember HDFC is a hard bargainer and CANBANK management must have been expecting 600+ per share which obviously did not materialize. I do not think the floor will collapse now but the scrip needs to survive on its own merit.

This whole episode contains learning for all in general and specific one for some big investors. They should remain discrete about their stock picks despite the disclaimer " this is not a reccomendation. I can sell it tomorrow…" The buildup of the event was great then came the crash. Interesting to see that the stock fell sharply even before the actual news came out.

Big lesson learnt.

Don’t buy anything expecting some news to take place. If something which you know all know then it will already be priced in.

Don’t build your conviction based on some one else’s conviction. “A beautiful dream” for someone may not be beautiful for you.

Although these are basic learnings somehow fell prey to these in excitement.

funny thing is both the buyers had own reasons not to pay top dollar for Can Fin. HDFC is too big to pay so much for Can Fin while Baring’s biz is all about buying low and selling high. Why should anyone pay so much. Ideally Gruh Fin should have gone for all stock deal given the synergy. Would have been an idea thing for Can fin holders but Can Bank might have liked to get cash immediately. Another thing is some RW politicians are raising issue about selling of family silver as potential scam. Banks have been nudged by the Central govt. not to sell loans or assets cheaper especially just before election year. Some of the banks have backed out from selling NPA loans given strong visibility in IBC process. I don’t think it makes sense for Can Bank to accept percieved low valuation for a good asset.

This news article last week seems to be spot on, isn’t it?

Canara bank MD confirmed that there were 7 offers out of which top 2 were selected and then one was finally shortlisted and that it was Baring.

It also says that Baring offered 570 rupees per share but Canara bank will ask them to revise upwards ( clear now as Canara bank MD says that even though Baring qualified, the offer was not matching expectations).

It also says Baring is unlikely to revise it upwards and if so Canara bank has to call off the process or look for new buyers, which indeed happened that they called off the process.

If all the above are indeed true, then it’s good that big institutions made offer higher than 500-550. It could also be due to control premium but then if the deal had gone through they would have given same price in the open offer as well. So that gives an indication of how institutions value Canfin business.

On a side note though, not sure if such reporting and gathering / leakage of information is legal

The return on assets and net-worth of Canfin is fantastic and almost as good as Gruh. Neither private equity like Barings or a titan like HDFC can do much to better it. Hence the price of ₹550 was appropriate. The sales growth has fallen drastically in the current year, whereas the profit growth has not and the management has been trying desparately to show the profit to entice buyers. Considering that the margins cannot be bettered, something has to be done to bring back the sales growth. This requires a Sanjaya Gupta or Choksi at the top, which clearly HDFC and Barings are not having and hence the reluctance to pay top dollar. Elango had warned of a decline in performance before leaving canfin and he left at the right time. Next the profit growth decline too will follow, but the ratios will be as good as ever, since this is a business with good economics. It required an Alexander to galvanise the already powerful Greek army to conquer the world. The canfin army is ready, but where is the Alexander.

What is the sales growth of the great HDFC? Their company will one day be crowned as King of the market, even with the present run rate. Yes, they will be the biggest company, even though their best days are behind them. Choksi I believe is close to retirement and doesn’t have anything to prove.

very well said and articulated.However what is puzzling is why sales growth is coming down? Because they are very conservative or marketing is weak or management bandwidth?

Sanjaya Gupta prays for his competitors that they don’t fold up, first time in the morning and last time before he goes to sleep as revealed by him in a recent concall. He has said that PNB housing will grow 1.75 times the housing finance market and maintain the run rate for decades to come. Only the mightiest of men can pray for his competitors. But first he has to defeat the Persians. Egypt will wait for its Pharoah.

In my limited understanding, the role of managements is often overstated. Sure, good leaders play an instrumental role in deciding a company’s direction but it’d be a flaw to attribute a company’s success entirely to them. Yet again, in my opinion, sectoral tailwinds and factors that are completely beyond the management’s control will play a more important role.

A company needs a management that’s not bad and tailwinds and the company will do just fine. A lot of company leaders experience consequent luck. We tend to ascribe the good outcome to the top management. We label them efficient, visionaries, dedicated and shower them with appreciation. Had the same action led to an adverse outcome the same leadership will be disparaged, belittled. Sometimes even the best intentions may not lead to good results and sometimes even seemingly reckless decisions lead to extraordinary success. It’s hard for us to resist the outcome bias.

To summarise - Management that doesn’t end up doing horribly wrong things and sectoral support should often lead to decent performance.

Even an idiot can run canfin homes. With bad management a mediocre Aspire home finance can have 4.6% NPA or more and negative profit from the previous years 100 crores.

With good management, an already good PNB housing has become unbeatable.

Frankly, I don’t possess the ability to tell if the management is good or not. For PNB, is it possible that their management is being termed good based on the outcome of their actions. Only if there’s a study that tries to correlate management actions and outcomes will we know their actual contribution.

And, we’ll know whether Can Fin actually can be well run or not by a simpleton only when it’s run by one.

First a sales growth decline . Then a profit growth decline. These are the first indications of a simpleton at the top. Then the good economics will kick in and the margin and return ratios will be maintained. These will the indications of such a business.

Well, this is precisely what I’m trying to find out- How do you know if the management is smart or not?

Can Fin’s growth hasn’t been per the expectations of some shareholders. Despite the management’s best intentions numbers may not be very impressive. Hence, such disparaging assessment. However, in a couple of quarters if growth resumes the same management will be termed dynamic, aggressive, foreseeing. Our opinion of the management is based on the outcome. Even if you bring the best leader but other factors don’t complement it the leader can’t do much. We’re victims of the illusion of control. There are too many factors beyond the management’s control. Hence,in my opinion, it’s inappropriate to blame them.