Don’t think so. In one of the interview he said either of Canfin or PNBhsg will reach 5 figure, which one first difficult to say. That means he is looking for 2000 after division of Canfin

Yes true. But then he also has the pressure to deliver returns to his PMS investors.

If HDFC buys the stake, I would prefer to continue holding the shares.

1 Like

While nothing is clear in this world till the entire information is public, the job of a clever investor is to invest on the basis of likelihood and range of outcomes and the ability to construct a possible theory which rests on the basis of collection of multiple seemingly unrelated data points:

So a lot of points seem clear to me basis the information on this thread and recent cnbc stories on Canfin deal as well as disclosures by Canfin and interviews of management. Ofcourse I could be wrong but I would peg that as a low probability event.

-

BM tweets are solely for Can fin homes (wonder why would anyone get excited about listing of Bandhan Bank which is already priced to perfection like most IPOs are and whose IPO was always a given as RBI informally mandates all banks to be listed within a particular time frame)

-

BM has Canfin as one of his top positions

-

Canfin homes deal is almost done now and what remains to be known is the identity of buyer and price. I would find it highly surprising if the deal falls after so many rounds of interactions and with the owner like Canara Bank - which may not be as demanding on valuations as many private owners are (whats goes of Canara Bank’s MD if the deal gets priced +/- 10% - all he needs is cash to shown on his 31st March balance sheet so that his capital adequacy looks good and he can hope to see a promotion as MD of a even bigger PSU bank). This is not to say that deal will happen necessarily, just that the probability of not happening is low enough.

-

Buffett has taught us that very good/great companies are those who perform even if a idiot runs them, because someday an idiot will - long term investors in Canfin homes like me know Canfin is one of such companies. So exiting Canfin just because HDFC hasn’t aquired it is an unreasonable argument. I don’t think Canfin performance will materially divert because of change of ownership.

-

PE guys in most cases are equally if not more careful over value creation as well as valuation - plus they have the ability to generate great M&A when they eventually exit. So again, exiting Canfin just because some of world’s best know PE firms like Blackstone or Barings has aquired it is equally unreasonable.

-

Valuations are rich in Canfin - with or without deal - exiting Canfin because one finds much better opportunities elsewhere for mid to long term (which may not have smooth earnings growth like Canfin though which gives good peace of mind to some) is a perfectly valid argument.

-

Fund managers like BM have many more reasons to become over happy at a Canfin home deal. A) its gives them bragging rights amongst their peers and people around them - when you are rich enough in life bragging rights count and for many they count even more than performance - for starters please read one of the Barton Briggs books B) 31st March is near and it helps them to get high performance fee regardless of whether they sell Canfin or not because performance fee is calculated on portfolio valuations and not actual profit booked, C) it makes their performance data looks good which helps in more clients and hence more fee income. So speculating on when BM would exit just because deal is done is equally uncalled for as he has many other reasons to want this deal. Although if the prices do rise a lot, it will be bad for all new investors of BM as most fund managers mindlessly run model portfolios for their clients but most clients, unfortunately, mostly focus on just past.

-

I have my thoughts on price as well but lest we promote speculation on this forum, I would rather keep them to myself.

One more whacky thought - Ideally Canara Bank should have stopped all its business and merged itself with Canfin homes - taken all the money to buy 75% of Canfin homes and given rest of it as just equity to be deployed in future and meanwhile be put in safe bonds issued by HDFC. 10 years hence they would have been so happy about their share performance. What a tragegy for Canara Bank minority shareholders to instead sell 30% leftover stake to someone like HDFC and continue running their business. But who cares !! certainly not the government.

Sarvesh Gupta

Disclosure - Invested multiple times in multiple roles in Canfin in my career. Invested from lower levels at present and can exit anytime.

15 Likes

Can we expect details of the bid to be disclosed by Canara bank tomorrow (Mar 15th)?

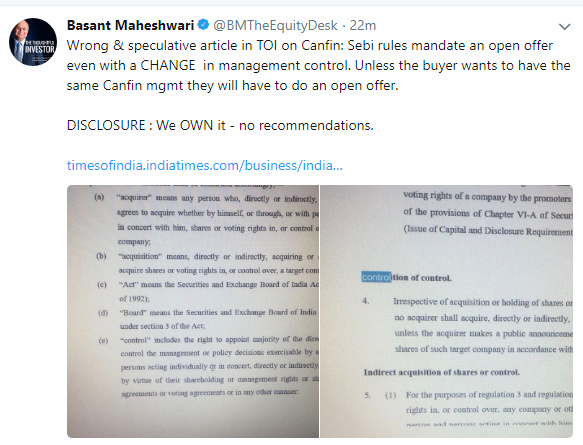

Interesting developments for those following CanFin Disinvestment deal by Canara Bank.

TOI report is full of noise without substance and BM’s counter.

Note: By now it is almost confirmed what was BM’s dream, hopefully it wont just remain a dream.

Do you mean HDFC will not be buying the stake? Or the noise is about the open offer part?

Open offer will follow. Deal might happen arnd 540-550.

Please msg if anyone has confirmed update about stake sale.

Somehow I don’t understand rationale for HDFC bidding for CanFin. HDFC’s quarterly addition to its AUM is more than entire CanFin portfolio. HDFC is adding one quarter worth of growth but paying a price that is more than what the market is valuing its own business. There is no cost synergy, no opportunity to cross sell, no entry into new geography, no acquisition of technology, personnel, markets nothing.

By this logic many existing HFCs, and banks will not be interested in CanFin. High valuation of CanFin is also a deterrent. Only those entities for which some of these benefits will be applicable will be interested. That’s why we see some PE firms are bidding for it.

Having said that, I don’t understand rationale behind many M&As so this might be just another one.

7 Likes

Perhaps, looking at why HDFC bought GRUH way back will give some idea I guess. When HDFC did that, GRUH was a miniscule company but GRUH is specifically targeting a niche - that is, the non-salaried & low income class, which something would have been difficult for HDFC to do on their own - as their employees are more tuned towards salaried / high income segment. In a similar way, perhaps HDFC is looking at Canfin Homes to cater to the affordable housing market in the MIG-1/2 segment, where the income of the buyers is much less than that of a typical HDFC customer and higher than that of a typical GRUH customer.

Just my opinion…

But keeping asides the valuation part, initially almost 12 entities met with Canara bank / Canfin Management in January when Canara bank formally started the sale process. Even Kotak Mahindra bank was interested, so I guess the company looked attractive from business and growth perspective. And there were almost 8 big PE players as well - including Blackstone, which is primarily into real estate (commercial though) market deals.

So, the segment looks very attractive perhaps, without which obviously such interest woulnd’t have been seen. But I guess valuations kept few of them away in the initial phase. Now there seems to be around 5 to 6 players interested (as per comments from Canara bank MD)

3 Likes

Synergy is there. HDFC big ticket loans, Gruh non-salaried small ticket & the gap is filled by Canfin which caters to salaried small ticket loans. As soon as management pedigree is changed to HDFC,Canfin will have premium valuation like Gruh

I agree. There is definite synergy - else the management of the pedigree of HDFC would not bid. They obviously would have evaluated the pros and cons of such investment, and bid accordingly.

Lets put ourselves in the place of HDFC and think. While, my qtrly addition to AUM is higher than Canfin’s total loan book - Why would I wish to bid for it?

- Housing Finance is highly competitive space - with Bank and other HFC’s all vying for increased market share.

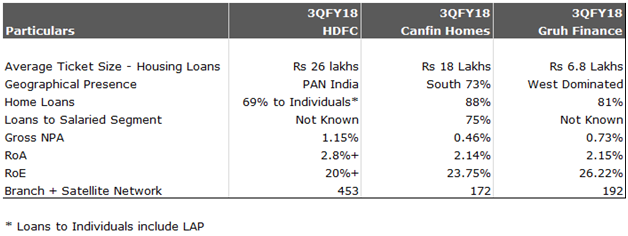

- I would like to acquire a company who has very clean books - Gross NPA of Canfin are the lowest in the industry. Besides, it lends predominantly to Salaried employees - which gels very much with the HDFC Culture

- Would not wish to acquire an HFC lending too much to non-housing segment. Canfin’s 88% of Loans are to the Housing Segment (highest in the industry)

- RoA & RoE’s should be superior - Canfin’s RoA @ 2.14% and RoE @ 23% are higher than HDFC’s

- Will I be able to leverage the Branch network - Canfin has a branch network of 152 Branches and 20 satellite offices.

- Will my acquisition be beneficial to shareholders of HDFC. HDFC acquired GRUH which trades at multiple of 12x Price to Book. I am getting Canfin at 5x P/B. Can I create another Gruh?. If yes, we must bid for it.

Now - talking to some analyst friends - they say while the above logic seems reasonable, the counter logic is

-

HDFC as per their latest presentation says, their stock is trading at 2x Price to book. Why should I not buyback my own shares, instead of acquiring Canfin @ 5x P/B

-

Canara Bank is selling it’s stake as they are in dire need of capital. Hence, apart from a better price - they would ideally be looking for an all cash deal. HDFC’s recent raising of equity of 13,000 Cr has allocated 8,500 Cr of cash for HDFC Bank, and balance for 3 other ventures - Affordable Housing business, Medical Insurance business and launching Stressed Asset fund in real estate segment. Besides, if their bidding would lead to open offer, they would have to shell out more cash.

I guess, we will have to wait and watch how the thing unfolds.

8 Likes

@Yogesh_s, what if HDFC wants to merge can fin with Gruh Finance? It will be like buying a company at 6 times book and post acquisition your investment in that acquired company will be valued at 10 times the book.

Added advantage is readily available branches, staffs and customers.

Just a few cents.

1 Like

Excellent thank you-very valid arguments

Thanks for excellent inputs to members of the forum.

I am just looking at the other side in case some private equity firm buys the stake and not HDFC. How the market will react to this news and if there will be a knee-jerk reaction to this since stock has moved up from 450 to 540 odd.

Can the forum members throw some light as to how their strategy will be in case HDFC buys stake and more importantly if HDFC doesn’t?

Thank You

Salil

http://investment-mantra.co.in/

When is the announcement due - does anyone know?

1 Like

Checked the Baring website. Interestingly they hv a stake in HDFC too.

Is Canara bank management taking too much time to decide OR is this process generally a lengthy one?

Dear newone

Good to meet you here besides Moneycontrol forum.

On a lighter note, I think we are getting bit impatient.

Can Fin Homes has been a gem for Canara Bank and it has to part ways because of its Core banking has been in a mess due to increased NPA’s.

In desperate need of funds, it would like to do a hard bargain with contenders and get the best possible valuation. So it may take few more days but I think Canara Bank CMD clearly mentioned in an interview that it will be closed before March 31. So the decision is not far away.

As investors, we also are bit impatient because of so much build up if HDFC will be able to make it as we long-term investors believing in Housing for All story and HDFC towering stature want it to come out a winner.

Above views are my personal and holding 1850@320 odd. Opinion may be biased.

Salil