Can it be even backdated? What’s rationale of the same?

1 Like

Company came out with clarification on why they went for split

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/9d15fc3a-e2fa-46c3-a98c-bc3df07a9723.pdf

As expected - cited excuse of retail investors’ inability to afford such a ‘high priced share’ for going ahead with the split.

I have a simple equation to calculate the affordability of a stock for a retail investor - as per SEBI IPO guidelines, the minimum value of 1 lot of shares that a retail investor must bid for must be between Rs. 10000 to Rs. 15000. Hence if the retail investors can subscribe multiple times to any IPO (Ex. CDSL, D-Mart) they can surely buy CanFin at 3300.

Anyway seems all hogwash to me.

3 Likes

Actually I feel that new investors look twice before buying something over 1000rs. For a newbie quantity matters and not quality. Take example of MF, they go and pick the ones with lowest nav and not a best MF at higher NAV. I have been in that boat when I started as well. So it does hold some merit.

Cheers

G1

I only hope that CANFIN management does not bother too much the stock price and are focussing on their work. HFC sectors are heating up with more and more players joining the fray. Even banks are aggressive on housing loans. Don’t know how big is the pie but it is getting too crowded.

As on Mar 2017, the book value is at Rs.404 per share where Rs.1076 is in their books. Assuming another 300 crore rupees are added to the books by Mar 2018 and adding 1000 Crores coming in via rights issue, the total own funds by Mar 2018 would roughly be Rs. 2400 Crores. Assuming the total equity share base to be roughly between 2.9 to 3 Crores after the rights issue from the current 2.662 crore shares, the book value by Mar 2018 would roughly be Rs. 800 per share or above. Is my calculation right?

6 Likes

Hi newone, Your calculation looks perfect and reasonable to me, assuming that, the rights issue will ultimately happen for the full Rs.1,000 crores itself

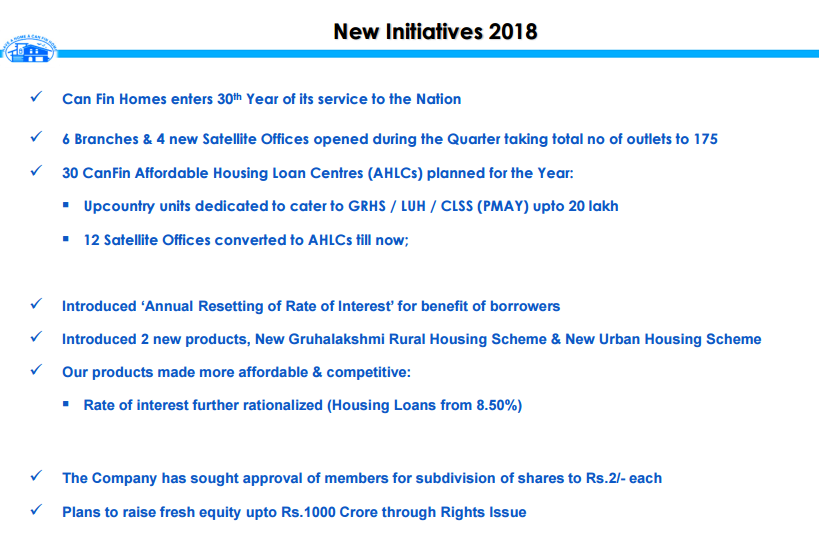

I infact missed the stock split part. But thats more of a technicality. The book value will then be Rs. 160 instead of 800 considering stock split of 5:1

I think you’re on the right path but I’d like to be a bit conservative in my approach based on past history.

-

Rights Issue - You’ve assumed issue of 34 lakh shares for raising 1000 cr which works out to Rs. 2941 / share. Previously in 2015 - they did rights issue at 35% discount to 52 wk high (infact stock tumbled from 690 to 620 during the trading session when they announced rights issue at 450). Going by that - I’ll be very suprised if rights issue is around Rs. 3000 / share (unless stock comes near or crosses 4000)

-

Book Value Growth Rate - For FY16 and FY17 earnings have grown between 45-50% for both years, but book value has grown by 14% in FY16 and 23% in FY17. So your growth rate assumption of ~28% may be a bit on the higher side

So overall I think book value should be somewhere around 725-740.

5 Likes

Hi Gurjot,

I am assuming issue of 24 to 34 lakh shares as part of rights issue thereby considering a wide range of Rs.3000 to 4000 as the issue price. In the previous rights issue, the share price was around 400 when the company announced the intention to raise capital via rights issue (it was July 2014). By the time they announced the issue price in Jan 2015, the stock price had already reached 600+ The discount was to the price that prevailed in Jan 2015.

For the current rights issue, as their approval process in lengthy, the share market price of Canfin could be at a higher level that what it is now by the time they complete the approval process and decide on the issue price.That is the reason why I have taken a wide range. But still assuming a rights price of 3000 is too conservative I admit.

About the book value, I took an estimate of FY18 profit to be in excess of Rs. 330 crores and added 300 of the same to the books. This is rough calculation. Do you know how to calculate this assuming a profit of 330 crores?

http://www.bseindia.com/xml-data/corpfiling/AttachLive/09a266a6-e891-496d-87b9-c69c84041c61.pdf

Results came out at 13.35 today…

Still digesting it and hence not commenting on it immediately

CANFIN homes Q1 Presentation

http://www.bseindia.com/xml-data/corpfiling/AttachLive/b17abc71-69c6-46ec-b4fd-ee6904a85a3f.pdf

Management in CNBCTV18 interview said seasonality behind NPA rise n moderate loan disbursement

2 Likes

Good results but two important points -

- Increase in NPA (highest in % and absolute terms that I have seen in the past few years)

- QoQ de-growth in disbursements

Need to see the management commentary on this but otherwise this is a bit of concern for me.

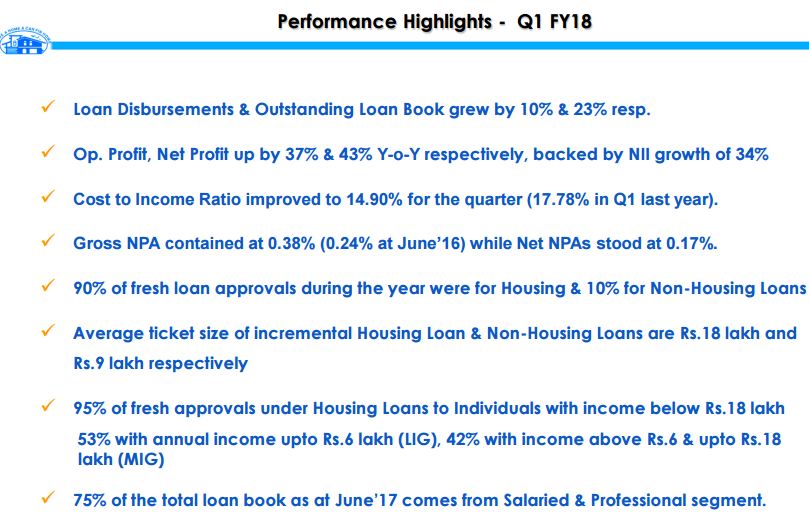

Can Fin Homes Q1FY18 standalone net profit rises 43.2% yoy to Rs.71.2 crore:

Net profit for the quarter grew at 43.2% yoy to Rs.71.2 crore. This was due to an increase in interest earned by 19.1% vs. a slower increase in interest expended of 12.5%. Its Gross NPA for the quarter stood at 0.38% and Net NPA at 0.17%.

Besides the growth, my second most important aspect of investing in Canfin was asset quality and extremely low NPA.

The Gross and Net NPA have increased significantly compared to previous half year. I hope they are able to arrest this trend early.

Balancing growth with asset quality (when the growth is slowing down) is a challenge for these companies.

However on second thoughts, wrt NPA, they are still much better than peers.

1 Like

Did anyone listen to the CNBC TV18 interview with Mr.Hota today? He mentioned some reasons for the increase in NPA but could not really understand it.

As far as I could understand, they made internal proactive adjustment and declare NPA so that it can be handled by year end. Hota mentioned that they expect Q4 NPAs to be much better.

Ya, he also mentioned something about demonetization hangover effect + impact due to confusion over section 269st (where more than 2 Lakh cash payment is banned by govt). Not sure how the latter has an impact but we need to see how things pan out in the next quarter.

Even canara bank has mentioned demonetization related moratarium impact on GNPA. Can anyone share how these two factors (demonetization related moratarium + confusion over section 269st) could have caused the increase in NPA levels for Canfin?

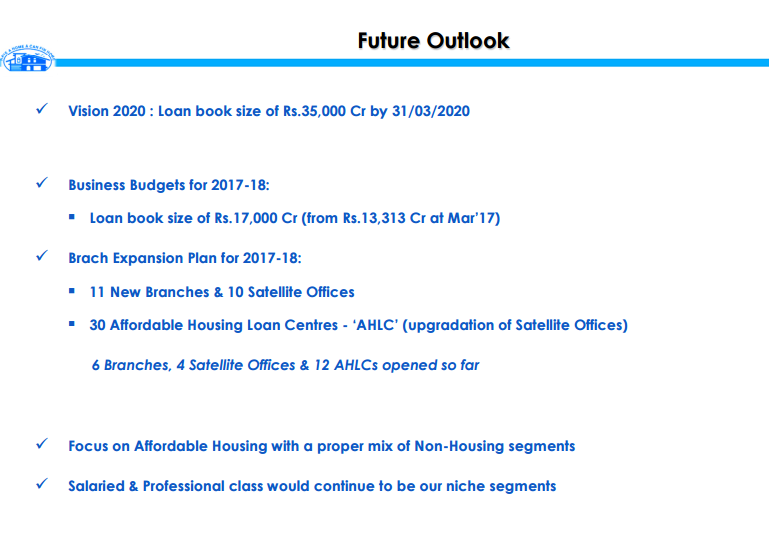

Forward looking indicators are down/low for 2nd consecutive quarter now. Can’t blame it on demonetization anymore.

Approvals are down and disbursements are up only 10%. This will result in low growth going forward.

This may be because they are running out of capital so they are raising additional capital or it could be because competition is catching up fast.

Source: Company Presentations.

12 Likes

Mr. Hota blamed it on seasonality and confusion due to Rera. As per him, Q1 has always been muted whereas Q4 the best.

Regarding the NPA, he blamed the lingering effects of demonetization (I did not get that). Second, reason he gave was that CF have put high servicing delinquent accounts in NPA at the very first quarter of the year so that they have enough time to deal with them. He mentioned that Canfin is very committed to it asset quality.

Disc: Invested and may be biased.