Thanks guys , @jk321@amitayu , it was pure luck to got estimate right.

We must congratulate @hitesh2710 bhai for this great find, it has been a 10 nagger for him and many in this group, I entered bit late. I always used to wonder how ppl make 100 bagger , if in next few yrs can fin delivers 30 % growth and rises to 30000 cr m cap . It will become another 100 bagger for VP TEAM

on the lighter side , valuepickr has made us some sort of analyst who are getting even their quarterly estimates bang on

Credit goes to vp core team for nurturing some of us and all the learning , way to go for learners like me

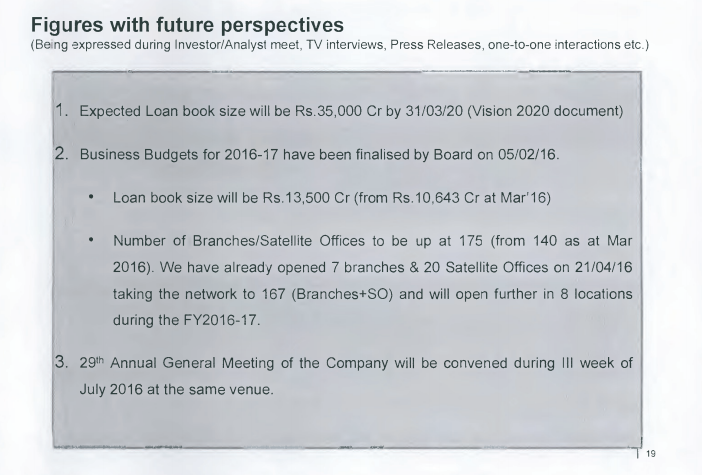

To fulfill 2020 vision of 35k cr loan book, Canfin Homes needs to grow at 35% annually.

But in the last 10 quarters, loan book growth was pretty steady at around 2200-2400 crs on a yearly basis.

and the interesting thing is that 2 years back he didn’t give much chance to can fin homes.(Dec 14 cnbc interview) It shows how well the company has out-performed and surprised everyone.

Agree they have executed flawlessly over the last few years… many investors who never wanted to buy PSU backed companies have realized this one is DIFFERENT

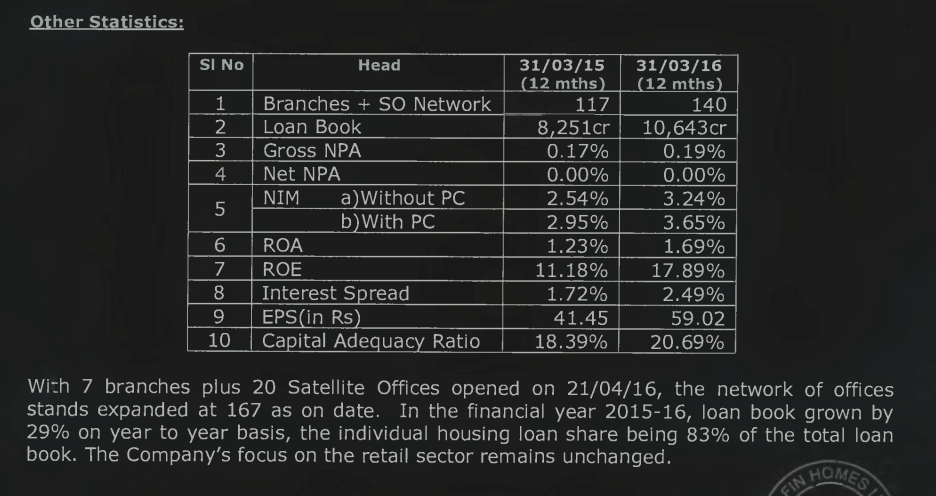

Here we see how Can Fin performed from FY12 to FY16. In FY13, co. had disbursement growth 111%, Loan book growth 50%, NIM 2.5%, Gross NPA < 0.5% and P/B 0.7. No wonder it hit seasoned VP seniors’ radar then (around FY13). Since then co. has flawlessly delivered on key parameters i.e. Interest Spread, Cost/Income ratio, NPA and Loan Book size growth. Here we also see what to expect in FY17 and FY18, assuming the momentum (in key parameters) continues.

Here is the spreadsheet source file if you like to change values and see its impact on co. performance. It has helped me understand the business better than before. Hope this helps you. Please use it responsibly and wisely.

I could not understand Provision and Taxes (Row 24) for FY17 and FY18. It would be great if you can share your assumptions.

My back of the hand calculation shows that CFH has to provision/pay for extra 28cr at least next year due to NHB provisioning (25-25-50) and NCD payment schedule.

So growth has to be very strong in operating profit else bottomline growth may be a little subdued.

The above table does not show payment schedule for Q4 FY17. If that is higher than Q4 FY16 - then the amount to provision/pay will get higher than 28cr.

Suggest using the spreadsheet (FY12 to FY16 part) to better understand key parameters driving this business. Meant for NBFC beginners. For NBFC veterans, it has nothing new to offer. Am sure we all understand that any focus on FY17E and FY18E would be futile. Cheers…

Good to see your effort and sharing of the documents. A few quick questions - 1. I have been pleasantly surprised to see the expansion in the “interest spread” and I feel the cost of funds got lowered due to raising of money via rights issue. So for next couple of years, as you haven’t considered any increase in equity, whats the assumption for decrease in cost of borrowing? 2. I think we need to also focus on the lending process of Canfin…its rare to see such low gross npas. Last time we saw something similar was in Muthoot Capital and after reaching a size, when the growth slowed the gross npa’s just shot up. Hence we need to understand as to what the company is doing different than the competition to have such rare feat and what could be the risks to it. Any work/insight should help.

One of the reasons for borrowing costs coming down is higher proportion of borrowings in form of NCDs. Impact of funds raised during rights issue might have run out by now.

Decrease in cost of borrowing (better Interest Spread) -

High level assumptions -

Softening of interest rates in the system (rate cuts) to led to a drop in the cost of funds.

Lag and some transmission loss in passing rate cut to clients to have a some +ve impact on the IS.

Strong AAA ratings (for borrowing/NCD) to hold.

Above average loan book size growth and low cost operation (impressive Cost/Income ratio) are key positive parameters in Can Fin’s favor even if “Interest Spread” holds at ~2.5% level.

Low gross NPAs

Few of the reasons - i) Individual housing loan = 83% of the total loan book and ii) Salaried and Professional = 74% of housing loan. That said, non-housing loan (high yield) is on gradual rise, thus need to keep a close eye on this key parameter.

i) Income tax benefit, ii) rental saving (assuming self-occupied), iii) ingrained honor system for home loan - “reputation” and iv) relatively low ticket size at reasonable interest rate (~17K EMI for ~17L average loan size) are few of the points that make housing loan lending a relatively safe bet even when the asset class is no more on steroids.

Of late competition has been poaching Can Fin accounts (high Repayments in FY16). Does it mean - indirect acknowledgment of a very strong credit appraisal system at Can Fin?

I’m not sure if the company would be issuing the NCDs at less than say 9% (caus tax free bonds come at about 7.5% hence taxable bonds wouldn’t find buyers at less than 8.5-9%). May be we can write to the company and ask what is the rate at which they issue NCDs.

Also, we may check what can be the overall borrowing by way of NCDs (it has already increased quite a lot vs earlier)

@lustkills 1. Yes, they have controlled costs really well and the cost/income ratio has been decreasing impressively. Do we have a comparison about this ratio with other comparable players?

2. On the low NPA - i think some of the other players lending to housing loans also have similar statistics yet they have higher NPAs. May be we can try tabulating a comparative analysis of like to like players?

@ayushmit --They have give interest rates in AR-2015

(i) Secured Non-Convertible Debentures

In its continuing efforts to reduce fund costs, your Company

issued Secured Redeemable Non-Convertible Non-Cumulative Taxable

Debentures (SRNCD) aggregating Rs. 300 crore (previous year Rs. 250

crore at 10.05%) in different trenches through private placement with a

coupon rate range of 8.78% to 8.80%.

The tenure of debentures is range bound to 2 to 3 years. The interest

on these debentures was serviced as and when it became due. The

aggregate borrowings by way of Secured NCDs as on March 31, 2015 was

Rs. 550 crore (previous year Rs. 250 Crore) while the overall cost was

9.72% p.a. with incremental cost at 8.84% p.a, indicating downward

trend in cost of borrowing.

Your Company is having the plans to raise Non-Convertible Debentures up to a maximum Rs. 2500 crore (last year Rs. 2,500 crore as permitted by

AGM) during the year, subject to cost benefit and asset liability

management requirements.

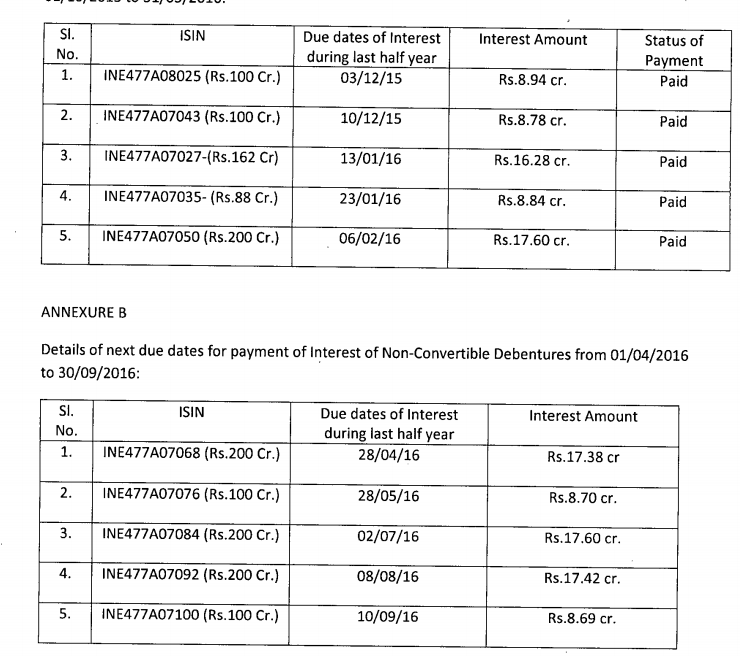

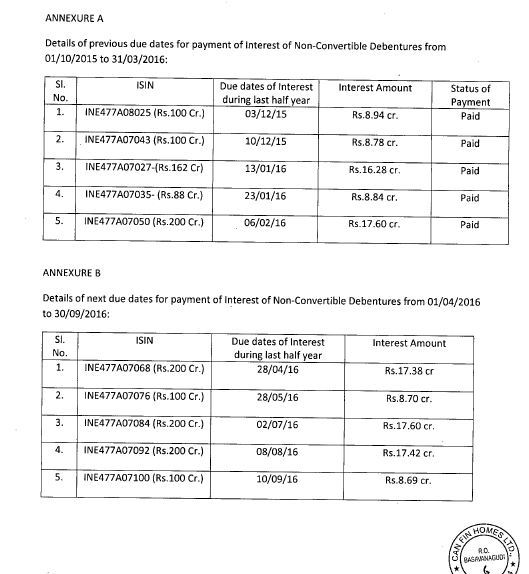

Annexures A&B give details of the NCDs and obviously we can see the falling interest rates on those NCDs.

As per annexure A, NCD worth 650 crs and as per annexure B, 800 crs matured.

Seems more and more funds were raised via NCD route.

HAPPY INVESTING

HAPPY INVESTING