Very high debt laden expansions are sure shot recipe for disaster and lead to many bankruptcies in the past.

Why one can be a bit hopeful, that they would not completely mess up the Dahej expansion is because of their past execution history. They have successfully executed mega integration towards higher sales with improved margins while managing heavy debt almost 2-2.5x of equity.

1 Like

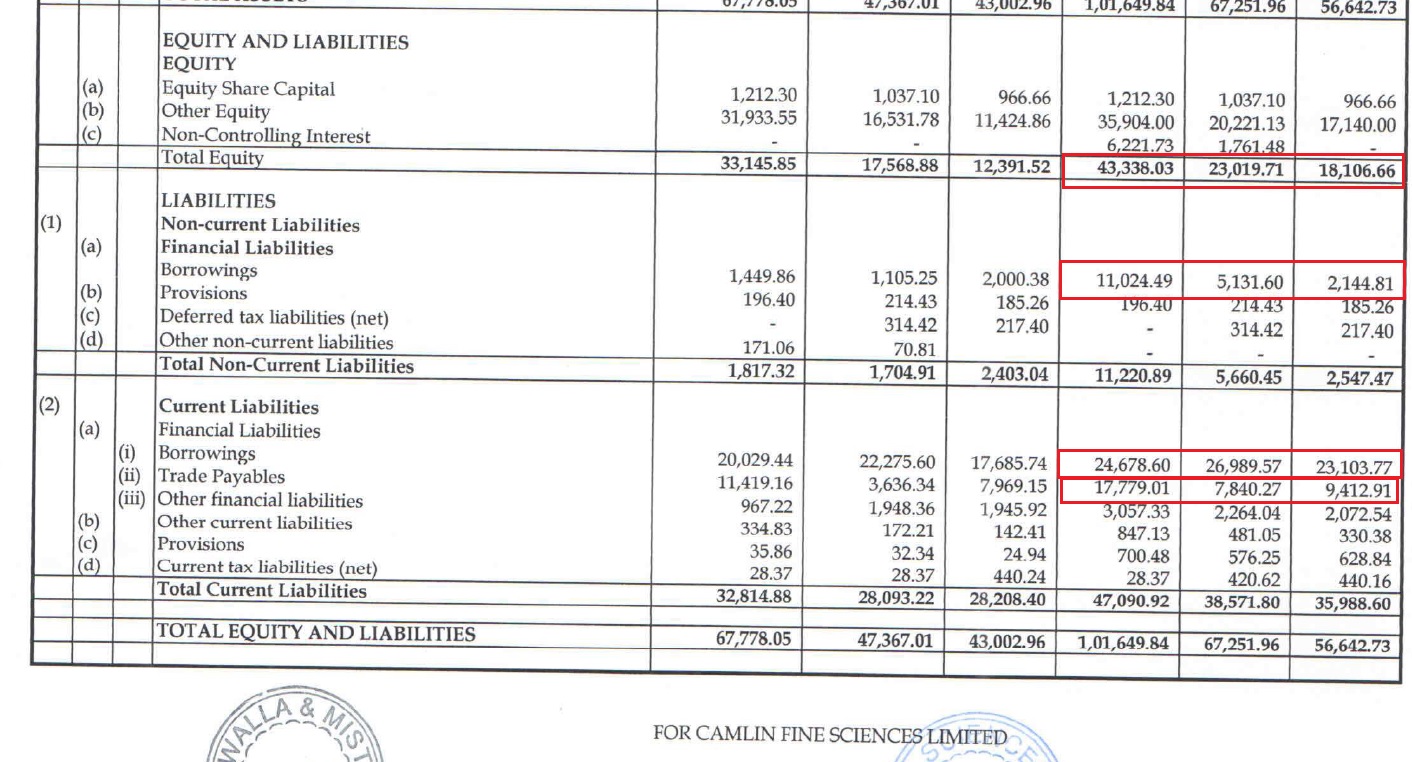

Based on the March 2018 Balance Sheet, we see the large rise in Fixed Assets as well as CWIP.

Equity raised significantly, so that gearing is somewhat balance even with elevated debt.

Also this business will remain Working Capital heavy and would need lot of working capital debt going into FY19 and FY20.

In Summary, we have a business with 13% OCF to Sales (FY2016) during business-as-usual period.

Looking at FY20 projected OCF, one is getting a chance to on-board a business at 8-10x OCF/FY20 Sales at 1121 Cr current market cap.

Disclosure : Invested

3 Likes

After a painful last couple of years, the company seems to have found its path. Thr last quarter earnings showed

back to positive at standalone level and ebitda positive at consolidated level.https://www.bseindia.com/xml-data/corpfiling/AttachHis/320c478b-ae1c-4bcc-8fb0-e1b363c12411.pdf

The outlook article summarises

httpsww.outlookbusiness.com/markets/feature/the-right-blend-4589

Things to watch out for : commencing of dahej plant in q4 , capacity utilisation of Chinese subsidiary Which is currently at 60% capacity utilisation, growth in Italian subsidiary which had a negative ebidta of -3%

1 Like

I feel the company business is getting more and more complicated to understand and too much of successive dilution. I am not tracking it for a while now as sold around Rs. 120/- sometime back.

They are doing all the right things on paper but I am not so sure about the ability to execute this multi location / multi business set up with so little skin in the game by promoter.

My opinions may be biased as I struggled understanding this company for a long time but efforts didn’t yield much fruits at the end

7 Likes

This is to inform you that on 10th October, 2018, the senior management team of the Company and that of our wholly owned subsidiary namely CFS Europe S.p.A, Italy (hereinafter referred as the Italian Plant) is hosting a video conference call with various funds and institutional investors to address certain concern raised by investors in relation to the operations/performance of the Italian Plant.

1 Like

I give up on this company’s ability to deliver projects. Debt ridden balance sheet in growing interest rates + Poor execution = Disaster for individual investor.

Does anyone see light at the end of tunnel?

2 Likes

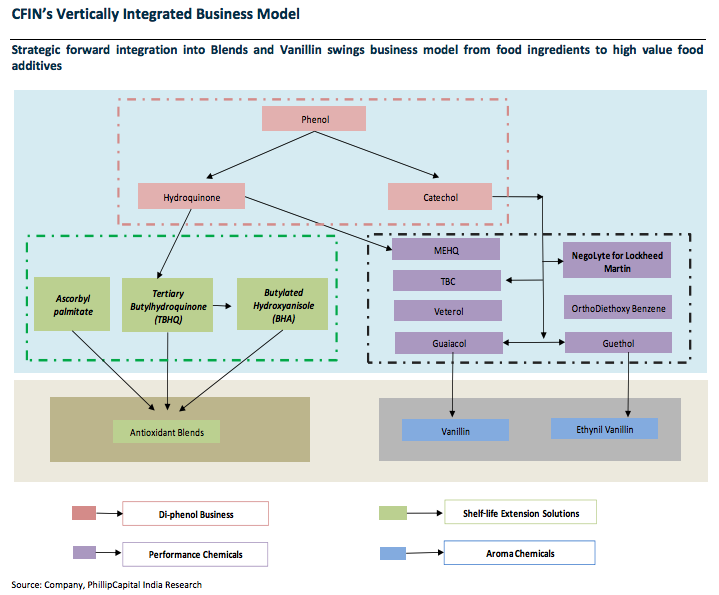

Many people are confused with the multiple moving parts as it continues the forward integration journey. The following charts gives you a simplified view of things.

Any such large massive expansion would have many problems, as things stabilize slowly much beyond the stipulated time frames. The current traction and management actions has been supportive so far. With the IDC funding and financial closure attained - the bet is entirely now on execution.

As highlighted in the thread before, they have managed such large debt laden expansion in the past and came out triumphant enjoying the fruits of the labor. I am cautiously optimistic and continue to buy slowly on the dips.

5 Likes

Hi Rudra,

It would be a great help if you can help me with two questions.

-

Was there any conflict between family members? Why other Dandekars exited completely from the company?

-

Why Ashish Dandekar (MD) has pledged 33.8% of his holdings? Any specific reason shared over conf. call?

Camlin turned PAT + at consolidated level. Good growth seen in stand-alone numbers. Dahej plant to be ready by March and to be commissioned in Q1 fy20.

That PAT is solely due to exchange profits.

@Prdnt_investor and @aveekmitra

Hi, do you still follow this company?

Today the stock has seen substantial increase in trading volumes of ~20 lakh vs 1 lakh usually. Any specific reasons you may be aware of?

Adding Q3FY19 concall transcript to an otherwise useless post.

- Breakup of blend business: Mexico-58cr, India-9cr, N.America-2cr and balance- Rest of the world

- Q4 would see significant improvement in business from N.America. Expecting a revenue of $4 million/year (??)

- Price of products in dollars: HQ- 6, Catechol- 2.5, Vanillin- 9.8 to 10, Guaiacol- 4.5, BHA- 10.5

- Dahej plant financial closure completed in Sep 2018. Mechanical completion expected by end of Q1FY20. 45 days for water trials afterwards. Delay due to increase in lead time for some equipments.

- China subsidiary top line was 62.8cr vs 18.5cr YoY. EBITDA flat at -1cr due to increase in cost of RM Glycilic acid. Business has seasonality with first two quarters being subdued. Margin will improve in FY20. China utilization is 62-63%. To become 100% in 2 years. Breakeven around 70-73%.

- India business- on standalone basis turnover went up from 118cr to 250cr. But negative impact due to rupee vs dollar fluctuation. Bought RM at 72rs/$ in the beginning of the quarter and sold at 69rs/$. This evens out on an yearly basis.

- Italy business was good. 85cr revenue. Healthy margins due to lack of fluctuation in currency. $ vs Euro. RM prices stable; phenol prices rationalized which led to improvement in margins. Should be able to maintain in Q4.

- Brazil business: Turnover of 9cr vs 12cr. Reduction due to Christmas and Chile business. Brazil business picking up. Should gro 40% in FY20. Several projects in pipeline.

- North America- Turnover of 3cr. But Q4 should see business for orders already procured.

- Mexico- 59cr revenue. EBITDA 17%. Impacted due to Peso appreciation vs dollar. Q4 should be better if currency is stable

- Getting more customers in US and hence US business should be breakeven in the first half of FY20.

- Neutraceuticals business started in Dec18. Currently using 3rd party production facilities with Gross margins 20-25%. EBITDA in early teens. Once we start producing ourselves, margins would improve.

- We make margins in the Guaiacol we supply. Done de-bottlenecking with new process. In Q4, 90% of Guaiacol will be made in that facility. 275T capacity. Will take it to 350T next Q. As cap utilization improves, we should break even in FY20.

- Other expenses would remain more or less around 70cr per quarter due to job work charges, selling expenses, tolling facilities for job work etc. It also includes forex losses of 5cr.

- Flow battery project with Lockheed Martin on track. Have some orders to fulfil in FY20 for some in-between requirements till commercial production starts. Now finalizing a contract for purchase of land near our Dahej facility. Land acquisition should be done in the next 3 months. Ultimately the project has to be executed by end of calendar year 2020. So we need to start construction and all commercial agreement by July 2019.

- TBHQ business is 46.7cr, blend 75cr, performance chemical 60cr, Vanillin/aroma business- 53.4cr. Miscellaneous is 4.5cr.

- Margin pressure in Vanillin due to two raw materials- Glycilic acid and Caustic. Both went up last Q. Former went up purely due to shutdown of two facilities in China. Supply demand gap. Caustic situation may improve due to new capex coming online. In a product of $10, $4.75 may be from Guaiacol, Glycilic acid impact is around $2.x and caustic is 70cents. Glycilic acid supply went down permanently.

- Our competitor not affected by increase in Glycilic prices since they manufacture the acid. Only one producer outside China. Solvay should also see this challenge since if prices go up by 10-15%, their supplier would re-negotiate.

- Dahej plant would bring substantial cost savings due to HQ and Catechol.

Q4 results on May 24.

Update on 20May2019:

Further creation of pledge. From 3.9 to 4.7% of share capital. Reason: Margin shortfall under borrowing- loan against shares.

1 Like

Credit Rating agency’s evaluation

Q4FY19 result summary (YoY, consolidated):

Topline grew 16% to 268cr.

Operational EBITDA margin 7.9% vs 4.9%.

Net profit approx 6cr vs -4cr (loss)

EPS 0.22 vs -0.26

Concall transcript which I noted down listening to recorded audio:

CFS-Q4FY19 concall transcript.pdf (49.2 KB)

Looks like the company is showing signs of turnaround. Dahej plant is on track, albeit delayed, and is expected to start commercial production in Q3FY20. Overall management sounds very positive.

2 Likes

Dahej is far from any water trials or even physical completion of the project. Right now even the equipment is not in place. A visit to the site can easily confirm this. The management has been consistently changing timelines.

In Q1 and Q2 FY 19, other catechol producers such as Solvay increased prices by nearly 30%. Solvay currently has an EBITDA of 28.8% in its performance chemicals division. In light of this, Camlin’ performance is abysmal, driven mostly by other income and one time events such as the general price increase of Catechol in Q1 and Q2.

With the Catechol and HQ cycle in its favour, Camlin needs to demonstrate much better performance before talking of a turnaround.

1 Like

Conversion of warrants allotted to promoters is due in August.

CMP around 55. Almost 40% below allotment price.

Company might face capital issue if warrants are expired.

some good news in consolidated results. is turnaround near?

1 Like

90,00,000 warrants forfeited due to non-payment of funds.

How will the company manage funds for working capital when Dahej kicks off?!

3df7c21b-721d-4eac-a7aa-c35a8adf0348.pdf (52.1 KB)

Company has received order from Maharashtra Pollution Board for closure of unit within 72 hrs (link)

Aparently it has happened in the past also in 2017 where the facility was started within 2-3 weeks (Link, Link)

Any insights on whether this is a recurring issue? Also, how much this affect the company?

Stock has hit lower circuit after the news

Disc: Invested

Q3 results (Link)

Posted profits versus loss in last year. Looks like the company is turning around.

Any comments from prople who are tracking the company from long would be very helpful.

Disclosure: Invested