@mihir23192 @Lynchfan

Dec and Mar are usually the best quarters of hospitality industry, given the wedding season and the holidays. I see a similar trend in Byke as well in the past 2 years. Any ideas about projections for Dec quarter? may be, i missed it in the thread or missed an interview…thx a ton, in advance

PS - tracking position @ 151

1 Like

I looked up Tripadvisor reviews of few of Byke’s properties in Matheran and Goa. Some of the customer reviews were highly critical of state of rooms, bad service, worst experience. I understand that every hospitality group get bad reviews. But when I looked at the distribution of ratings for Byke properties, it is equally spread between Excellent to Terrible. I would have preferred to have ratings tilted towards excellent.

I personally have very good experience with Tripadvisor ratings and used them to decide on hotels when I travel. Hence after reading reviews, I decided not to invest in this stock. This is my personal opinion and I am not passing any judgement about how company and its stock will do in the future.

6 Likes

The small 0.44% pledge against Kamal Poddar is released tdy

http://www.bseindia.com/corporates/ann.aspx?scrip=531373&dur=A&expandable=0

1 Like

Hi Gaurav,

Any idea how do they guarantee quality while chartering, OYO has some inspection checks i guess and also does some Point of sale branding.

Hi Jinu,

No idea on the quality check but will try to dig to get that answer for you.

As far as I know, there is neither any quality check is done like OYO nor any kind of Point of Sale branding.

The customer doesn’t know that they are getting rooms booked by Byke in bulk. All this is done through a channel of agents.

As far as Quality of Hotels and Services are concerned, I believe, it’s the expertise & experience of Byke Hospitality developed over the years in Selecting the hotels.

This is pure Wholesale to Retail business where Byke has a strong agent network and utilizing this capacity at it’s fullest to generate money.

The answer to your question is. “Bet on management!”

The second question might be, Can this Room Chartering Business be disrupted by OYORooms?

Anil Patodia says, Indian Tourism industry has a lot of room to grow and will not be impacted.

Third question might be, What about Scalability of Room Chartering Model?

They are building some online portal (backend) for agents & hotels so as to ensure timely booking and speedy work. It will also work as entry barrier for others as far as I understand this agent business. (I may be wrong)

Byke Hospitality is holding a conference all today at 2.30. These are the numbers.

022 3960 0659/022 6746 5959

CONFERENCE CALL

The Byke Hospitality

The company does not plan to raise any long term debt. Long term debt would be fully paid by FY 2018

The Byke Hospitality held conference call on 5th February 2016 to discuss its December 2015 results.

Highlights of the call:

The Byke Hospitality (Byke), is a fast growing hospitality services company. The company has presence across 50 cities. As on March 2015, the company had 519 rooms under its management, of which 102 are owned.

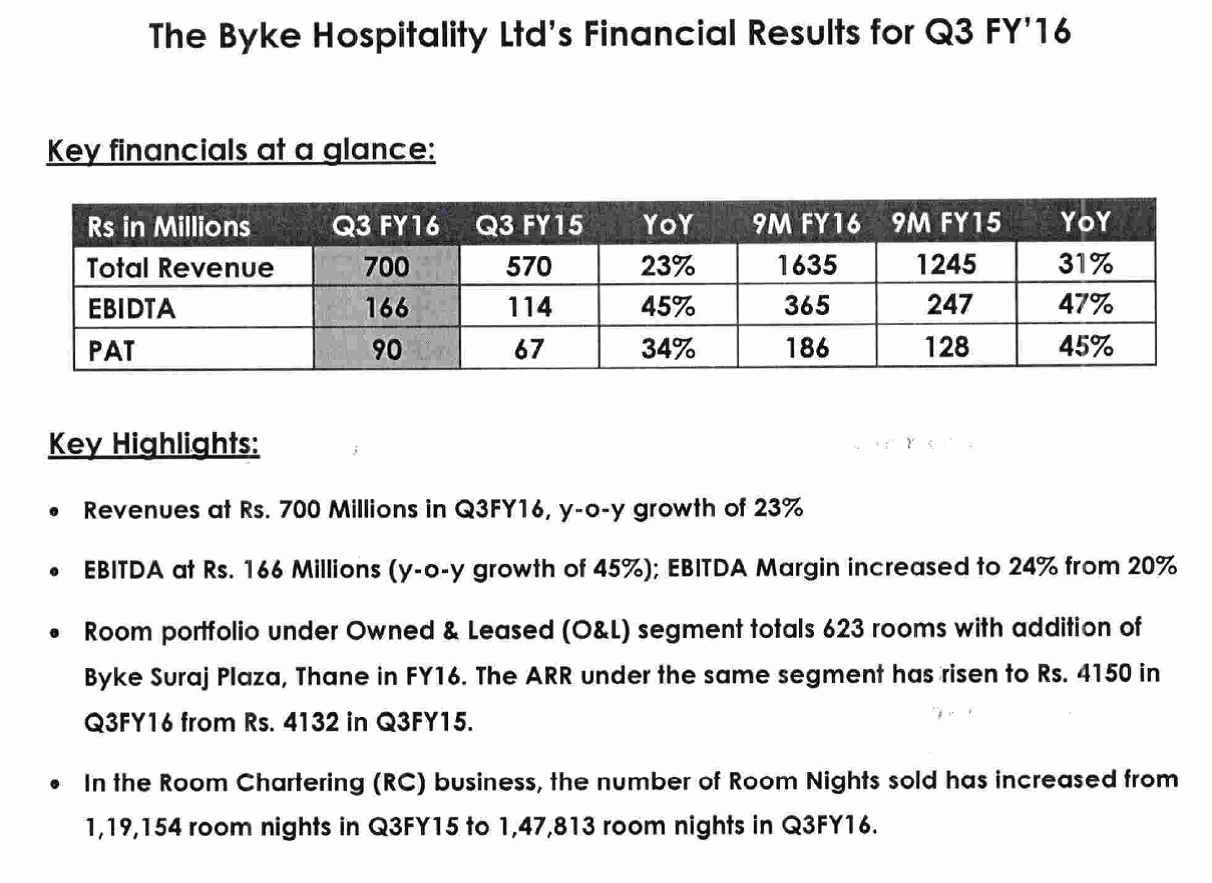

For the quarter ended December 2015, sales grew 23% to Rs 69.97 crore. OPM jumped 370 bps to 23.7% which took OP up 45% to Rs 16.57 crore. PBT jumped 62% to Rs 13.85 crore. Net profit grew 34% to Rs 9.04 crore.

For the nine months ended December 2015, sales grew 21% to Rs 163.51 crore. OPM jumped 240 bps to 22.3% which took OP up 47% to Rs 36.46 crore. PBT jumped 75% to Rs 28.45 crore. Net profit jumped 45% to Rs 18.58 crore.

The significant improvement in the company’s performance is a result of the strategic turnaround initiatives taken over the last couple of years, leading to a strong resurgence of the Byke brand in the marketplace.

For the quarter Room portfolio under owned and leased (O&L) segment totals 623 rooms with an addition of Byke Suraj Plaza thane in 2016.

For the quarter ARR in O&L has risen from Rs 4132 to Rs 4150 y-o-y.

During the quarter in Room Chartering (RC) business the number of room nights sold increased from 119154 room nights to 147813 y-o-y.

ARR in Room Charteringwas Rs 2300.

O&L registered revenues of Rs 35 crore which was around 50% of total income. Same with Room Chartering business.

For the nine months O&L registered revenues of Rs 76.0 crore which was around 47% of total income.

For the nine months Room Chartering business registered revenues of Rs 87.5 crore which was around 53% of total income.

Occupancy has posted strong growth driven by domestic demand.

Moving ahead to make a good brand in domestic market.

The company has 10 properties out of which 8 are operational.

The company sold 360000 room nights during the nine months compared to 370000 room nights whole of last year.

The company has extended its business s to 50 cities.

Occupancy level stood at 69% compared to 75% - the drop is due to new property addition.

The company hopes to add 400 rooms by FY 2018. Place and locations have been identified.

Interest cost fell due to repayment of loan. WC loan is Rs 6 crore which is intact. Term loan is on yearly repayment basis. The fall in interest cost is due to timely repayment. The company does not plan to raise any long term debt. Long term debt should be fully paid by FY 2018

F&B business has outperformed room revenues.

The company’s focus is hugely on F&B side. It is expanding in 8 locations in F&B business which have very good outlook for F&B business. This business the company can target for entire year.

Out of the total sales of Rs 70 crore sales, room revenue accounted for Rs 16 crore and Rs 17.5 crore came from F&B side and the balance came from room chartering.

RoCE in only room chartering business is more than 40%.

The company does not see any trend reversal in growth rates of room chartering business.

The company is going to add 8 more properties in next 2 years time.

After investing in owned and lease business the company will still have capital for room chartering business.

In O&L the company had occupancy of 69%.

Thane is a huge property and will add very good value into the company.

The 8 properties that the company plans to add are in Mahabaleshwar, Dalhousie, Chandigarh, Jodhpur, Udaipur, Darjeeling, Gangtok and Mahabaleshwar. If the company finalises all the top properties that it wants in these places it will add 550 rooms by 2018 and if it has to go for second best option, it will add 450 rooms.

6 Likes

They are doing wonderfully good and promoter looks very smart. He said that they buy rooms in chartering business only when they see there is a demand. They don’t believe in having more inventory. I also liked the fact that promoter understands that his focus should be more on O&L segment as other aggregators are catching up (he directly did not agree on that part but his actions say that he knows chartering business might see slowdown 5 yrs down the line as internet penetration goes up). Overall the guy looks very intelligent. The return numbers of the company are also good. Also, I loved the fact that promoter doesn’t like debt. It looked from the commentary that he will stay away from debt as much as possible. I have developed a full conviction and will buy more on Monday. I already have a very small starting position in Byke.

Thanks for penning it down Vishnu. Gr8 work.

Read Below Review in TripAdvisor & the then “FUNNY Reply” from their so called VP…

If they write like this on public place then how will visit their Hotel…After Reading this I am sure promoter will CON shareholders, as after reading comments on Trip advisor it seems they are not taking care their employee as well…

If they can not handle electricity in their 240 Rooms resorts, then god knows how they will be able to Scale up their business from here…its seems they are running a “Third Class” 1* Hotel, where you have to run around for everything… Not convincing at all…

Choose this resort only if you have a fetish of ruining your holiday mood.”

1 of 5 starsReviewed 5 October 2015

I stayed with my family in this resort from Oct,01 to Oct, 03. The resort is a pretty big property that has become a burden on the staff who aren’t able to manage it. It has a restaurant which serves only vegetarian food. The room was pretty small and uncomfortably humid and stinky with an AC whose power panel was broken - which means you have no option to control the temperature and the fan speed. In the evening of the day I checked into this resort, the power went off and know what? Their DG (diesel generator) broke down - both of them. Yes, they have 2 DG. The power was restored somewhere around 1:45 AM in the night. They never bothered to repair the DG next morning and the same thing happened the next day too. Power went off at 6 in the evening and came back around 11 in the night. During this time people gathered in the reception area and were shouting at the staff who just stood there like dumb with their heads down. They said the higher management have switched off their phones and there’s no way we can contact them. He even shared the number of the technician which when I dialed found it to be switched off. We spent two evenings of our planned Goa holiday in the dark fighting heat and mosquitoes. Overall the experience has been terrible and I would advice people to stay away from this resort.

Room Tip: Stay away if you wish not to spoil your mood

See more room tips

Stayed October 2015, travelled with family

4 of 5 stars

Location

1 of 5 stars

Sleep Quality

2 of 5 stars

Service

Helpful? 1 Thank loneworker

Report

Ask loneworker about The Byke Old Anchor Resort

This review is the subjective opinion of a TripAdvisor member and not of TripAdvisor LLC

THEBYKE, Director of Sales at The Byke Old Anchor Resort, responded to this review, 12 October 2015

Dear Guest ,

It is indeed unfortunate that your holiday experience wasn’t as per your expectations.

We are no. 1 in Gujarati and Rajasthani Food.

Regarding the electricity, please note that as in most of the holiday destinations, even in Goa, there occurs drop in the supply sometimes, however, our 24 hours generator restores the power went off for a long time from the Power House . We all were very much concern , our team was trying too hard to restore the power from the main Power Station .Mr. Soni (G.M) along with Mr. Ashish (Accountant ), went personally and had a tough time convincing the Government . Officials and had arguments with them , later after a long conversation it was resolved and power restored at .1:00 hrs . We tried a lot D.G (Diesel Generator) Sets ‘ parts were not repaired in – house and were sent out . Mean while we were in constant touch with the DG Suppliers (on hire), we finally arranged for 01 DG Set by Day 2 evening , later things were under control .

As regards higher managements cell switching off we disagree , as we all are senior people and know our responsibilities , The GM was in constant touch with ME , MD & VICE VERSA therefore, the question does not arise . May be our staff safe guarded us , as we were busy arranging for resolving the issue .

Mr. Jack (FOM ), himself came to maintaince department . with few representatives of the guest staying in – house to show the work in progress , as per their request around 21:15 hrs ,a t that moment outsourced Generator connections work on .

The entire team works very hard to ensure guest satisfaction, however, during certain periods they may have not reached to all the guests demands. We will certainly improvise on our services further.

Mihir Sarkar – VP,

The Byke Group of Hotels.

Report response as inappropriate

Disclaimer: Not Invested

3 Likes

I have seen a few lousy reviews on Trip Advisor in the past and took a long time before I took up a small position in the stock. What worries me is the dissonance between the reviews and the company’s results. Is it that only the ones who are disgruntled are posting reviews? Or something “hidden” in the quarterly numbers?

Discl: I have a small position in the stock and am planning to add to it should the price correct.

1 Like

I have stayed in Royal Orchid in Goa 9K per night and wasn’t impressed. It could be that Goa is very expensive and even then still can’t get good hotels.

Not intending to bias in anyway. Just expressing my view on hospitality in general.

Disc: Small tracking position

@ash7979 I agree that there some bad reviews regarding service of Byke. But you will find that every hotel will have such reviews. One can’t make decision based on such reviews.

The perfect example is Royal Enfield Brand.

Sir, You ask any person using any of the Royal Enfield Models, you will hear that oil leakage from engine is unsolvable issue, service from service centers are not proper, chains get loose very quickly and swing arm bush in rear wheels needs to be changed too often. These are the real issues. I am user myself.

Still, Eicher is beating all the estimates and performing well.

I appreciate your scuttlebut efforts of checking reviews on net but I feel this cannot be base the decision making. Rest is your call.

Disc : Invested (I may be biased)

2 Likes

@mihir23192 I am not saying the review are BAD…I am more concerned about the reply from the Hotel Manager (in this case VP) on TripAdvisor (Which is most widely used website for honest comments & I myself use Tripadvisor before bokking any unknown Brand/hotel & most of time I find its almost accurate…

Just see the language of the VP in his reply…instead of politely accepting their mistake he could have written we will try to improve on this next time, but he has explained it details like he wanted to debate with customer on this…Like this "We all were very much concern , our team was trying too hard to restore the power from the main Power Station .Mr. Soni (G.M) along with Mr. Ashish (Accountant ), went personally and had a tough time convincing the Government . Officials and had arguments with them ".

Why the hell you need to write this on Tripadvisor…They are is hospitality industry, but I dont think their staff is trained for that & most of comments are like they dont have adequate staff at their Goa property which is whopping 240 rooms property & management accepted those claims as well in their reply (Point to point which again I feel not necessary)…

So, I am not saying their numbers are not correct, but if they are having such a lousy service at their BIGGEST property big is earning them almost half the hotel revenue then go knows how they are managing their small properties…

I am not invested & I dont feel its a stock for long term…So my opinions are biased, but ppls who has invested hace you ever tried their hotels in any location, preferably their GOA property that will help us to get more insight into their hotel operation, as comments on Tripadvisor does not inspire me to invest in Byke …

4 Likes

My 2 cents- Trip advisors review are the first hand experience of the customers, We sud n’t brush off so many bad reviews as mere exceptions, they are indicating u a lot about the company perception and its future, In fact the current financials are merely a indicator of past efforts.

1 Like

With this correlation i guess the East India and Indian Hotels should do exceedingly well!!!, Reviews should be watched in totality. I agree on the feedback from VP should have been more polite however the underlying intention was ok. Coming to the Customer, he was even not aware that Byke only serves Veg food!!! in Hospitality expectation Vs performance plays a great role. They never claim that they r Star rated and their services are star rated.

They always claim that they are non rated chain of hotels.

2 Likes

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/4FA45159_28D4_47A8_BC1D_F46957FE57EF_143228.pdf

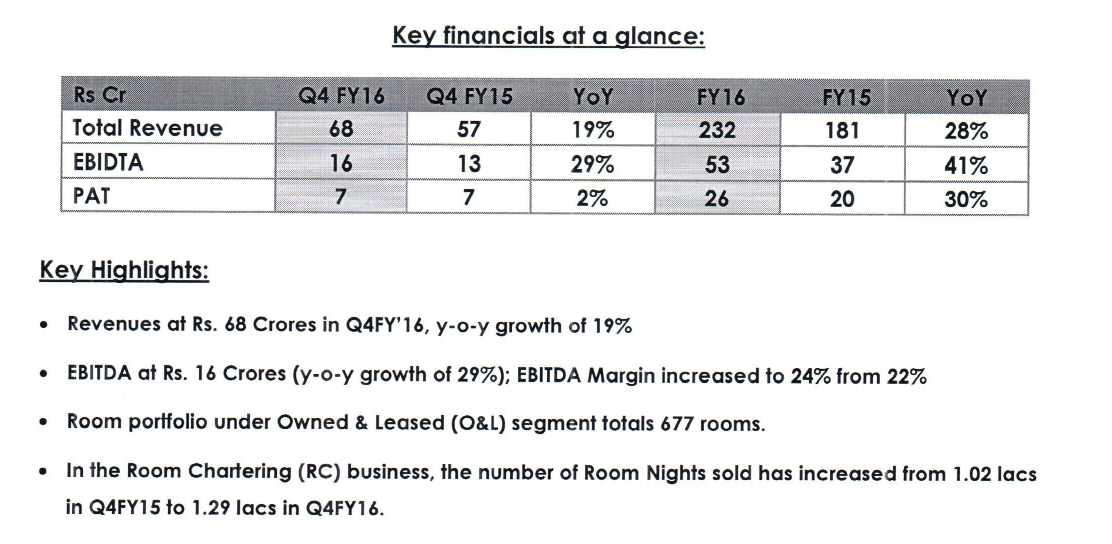

Results came out just now. Can’t find fault but can’t fall off the chair kind of result. let us see what Mr.Market does

Phenomenal numbers from Byke.

Top line growth - 28% YOY

Bottom line growth - 30% YOY

Dividend - Rs.1 per share. That makes it Rs.2 per share for whole year.

Key financials at a glance:

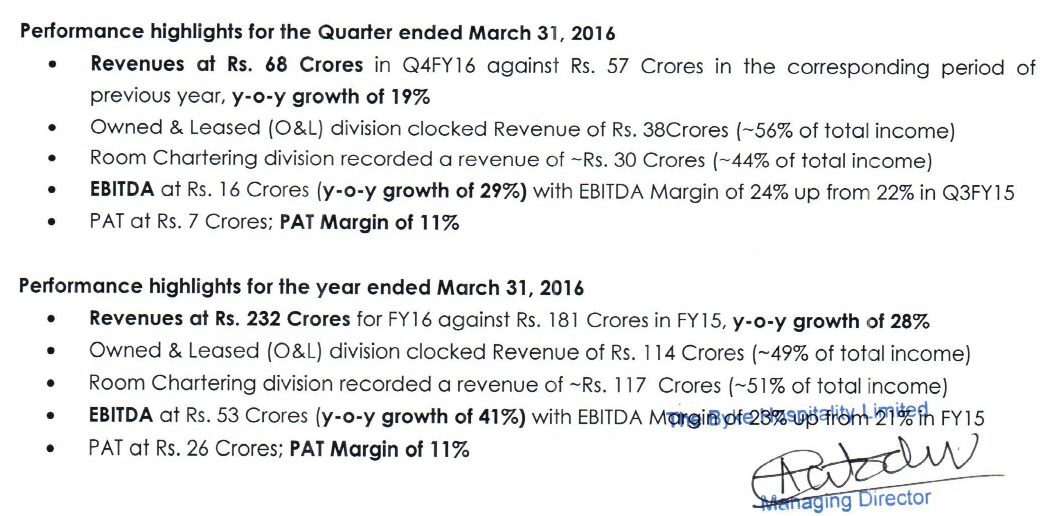

Developments in last year:

- “Bike Vijoya” operations are started containing 54 rooms in Puri, Odisha. On track of what they have promised about starting new operations in Thane(Byke Suraj) & Puri.

- Paid good amount of tax for FY’16.

Things to look out for:

- Employee expenses in Q416 has increased more than 100% compared against Q415. Overall increase of 64% in employee expenses. Could be because of new expansions they made last year?

- There is a reduction of ~4% in number of pledged shares. Still there is about 6% of promoter shares are pledged?

- Long term borrowings are reduced from 3.75 cr to 2.17 cr.

Long term loans and advances are stand 8.6 cr against 5.45 last year. I don’t know if that’s a good or bad. Explanation by somebody is much appreciated.

In spite of it’s growth I see that stock is dead rubber at 140-170 levels since 9 quarters or so.

What could be the reasons for not having a momentum in stock in spite of good quarters? View are welcome.

Disc: ~14% of my very small portfolio at an average price of Rs. 154.15