Nice rounding bottom on colgate followed by a platform and ofc a breakout to all time highs on huge volumes.

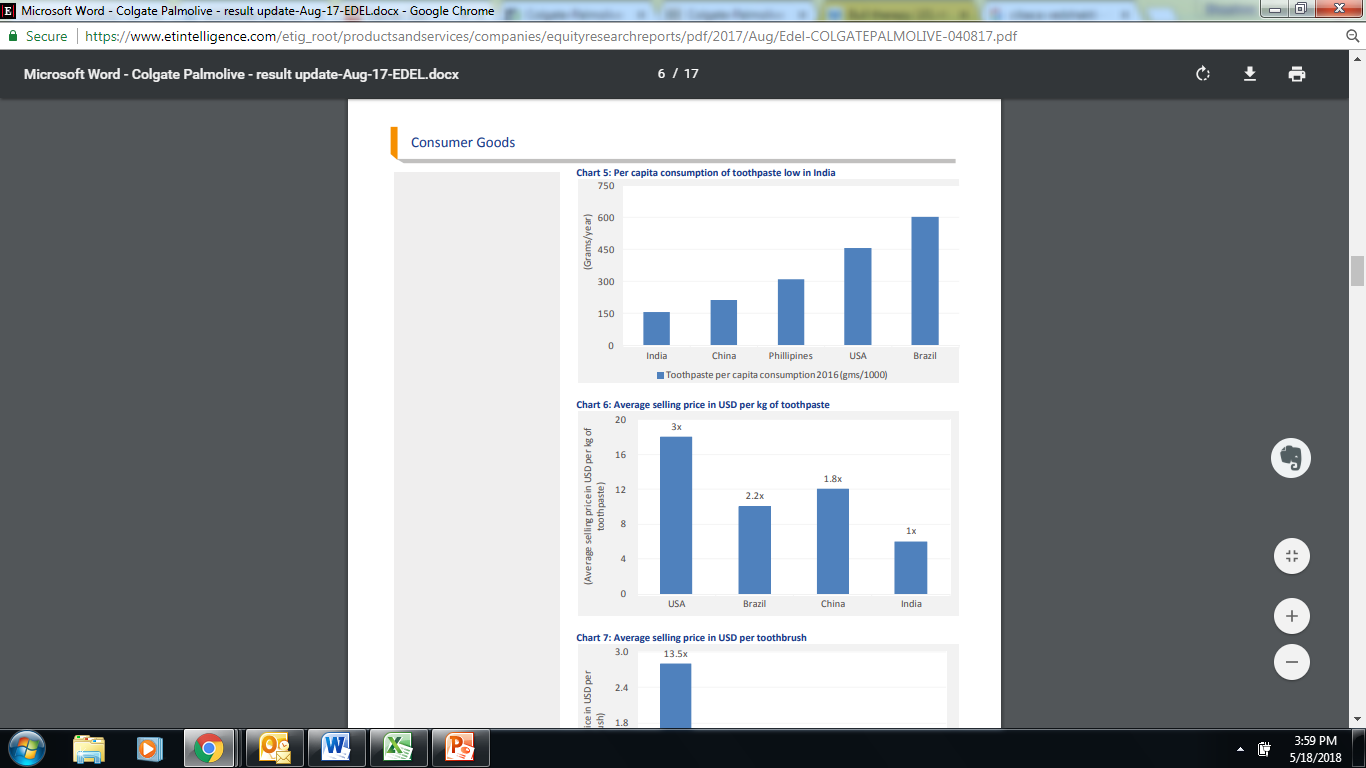

What is happening in the toothpaste industry is quite interesting. The herbal segment - popularized by Patanjali - has increased the pricing power for all players in India. The margins have really improved for Colgate and all other players. The average price of a 100 gm herbal toothpaste (average of all 4 players Colgate, HUL, Dabur and Patanjali) is currently Rs 55. Colgate has priced its offering intelligently and is currently the cheapest player in the high end herbal segment and low end herbal segment with its Vedshakti brand so there room to catch up on prices. It launched its Cibaca Vedshakti brand at Rs 32 per 100 gm and it is now up to 45-46.

In general, the gap in both toothpaste consumption and toothpaste prices is pretty high between India and other nations. The other thing about colgate is its FA turnover which is slowly improving compared to its historical average. It may not hit its peaks though so it remains to be seen.

the historic price action is very very manipulated in hcl info,

personally i was very interested in the scrip looking at the current chart pattern, but have decided to say away from it…

but after this phase E of this ongoing distribution is complete, the curious case will be what the composite group will do after this, if there is redistribution then more downside might be coming… it will be interesting to watch the price action…

recent development…

allotment of 150000 Equity Share Warrants Convertible into Equity Shares, to

Promoter / Promoter Group at an exercise price of Rs. 550 per equity share on Preferential Allotment basis

Presently[AO march18] the promoter holding is 42.42%

Currently catering to 43 countries strive to spread to 70 countries in next three years

planning to strengthen the distribution network by tie up with Homestyle and plan to add new 100 galleries and 34 more distributor.

Homestyle is a UK based company in which acrysil has acquired 98.75% stake recently.

Also opened office in Dubai to cater Middle East and African Market

niche play-

1.Globally there are only 4 players producing Quartz

Sinks. 95% of the industry makes use of Stainless

Steel and only 5% makes use of Quartz Sinks…Acrysil is one of them, presently distributing to 43 countries and counting.Only company in asia.

2.Entry into designing and manufacturing of 3D concrete wall tiles [technology provided by an hungarian company] and capacity expansion in fy19

Disclaimer… invested and accumulating , plan to allocate 15% gradually

The stock is trading in a perfect channel in the monthly charts and band around 280 is crucial.if the stock holds this 270-280 there could be a “W” formation on monthly charts, which is bullish.

Mayur uniquoters…

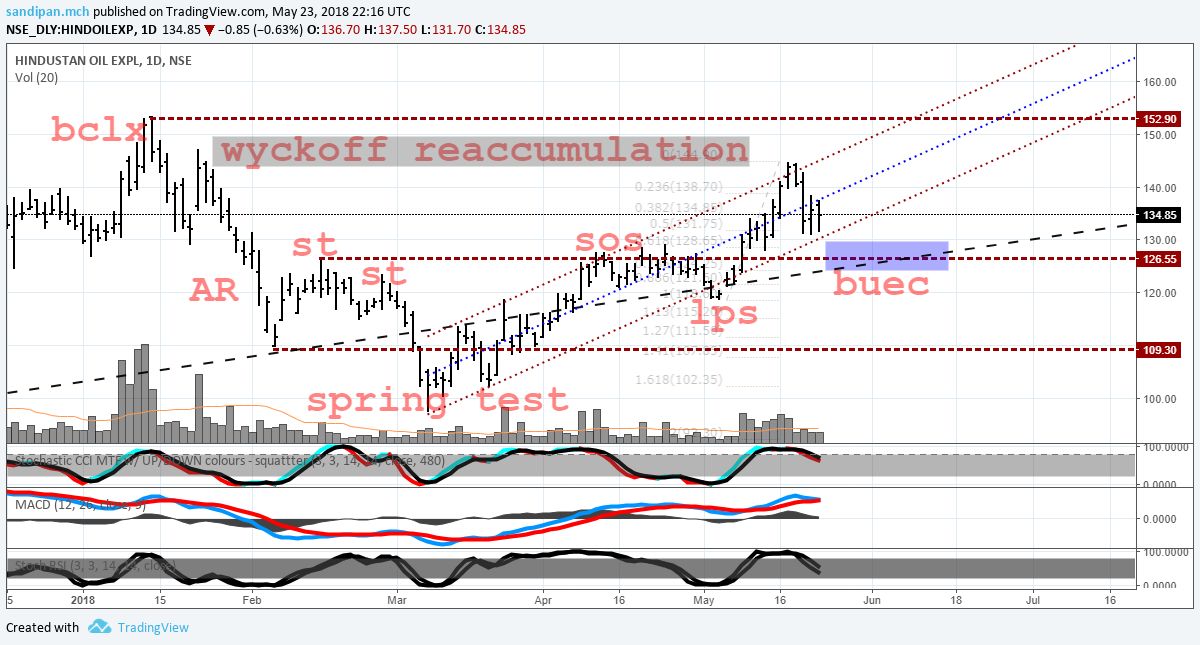

An excellent spring broke the supply line and complete change of character followed into a show of strength above the trading range…

Now forming a Last point of support in the wyckoff reaccumulation schematics…

And cherry on the cake is a symmetrical triangle, which might turn out to be a continuation pattern…

Elliott Wave working perfectly in SpiceJet (indeed it works perfectly almost every time). It’s just that I got the wave count correctly. When SpiceJet was trading at 135, posted that it should go down below 100, which it did today.Triangle formed in wave 4 and a ending diagonal formed in wave 5. That was a clear giveaway that 5 waves up completed and a huge correction (at least 38.2% retracement of 5 waves) was about to be done.

Fundamentally, crude oil price and weak Q4 acted as catalysts for the fall of SpiceJet.

Ashok Leyland - Posted a month ago when it was trading at 156 that it was approaching a major peak, and should peak out around 165, completing 5 waves up, and set for huge correction.

After 3 weeks, it peaked at 167.9. And despite posting very good Q4, it’s crashing. Now at 138.

The oscillators, decribe a little correction is left though, forming the “back up at the edge of creek” BUEC ,of the wyckoff reaccumualtion schematics…

The daily chart of Kolte Patil indicates that the prices have tested the 61.8% fib level multiple times. This level also coincides with the 200d MA where the prices are at this point. This could present a good buying opportunity.

The management commentary was very upbeat about the business prospects and has guided for 2.5M-3M sqft of presales in FY19. For the past two yrs there have been no new launches and hence the focus was on liquidating the existing inventory and bringing it to a revenue recognition which they have been successful in doing. The have two projects in Bangalore , both with high EBITDA margins of 60% , 1 of which is going to hit revenue recognition in FY19. The management also has also said that FY19 is going to be the launch year so there is an expectation of launches. They have a 6-7M sqft launch pipeline. They have created a funding platform of 700 crs to help them grab opportunities that come along their way via distressed projects. They expect to do some transactions via this platform in FY19. All in all there seem so be multiple triggers and the price chart seems to reflect that in my view.

FDC…

After looking at the chart i tried too find out for any fundamental developments , didnt find anything massive out there…

But a debt free company, with no observation reports offlate, mainly a domestic player…

the roce is at 27% , altmann z score of 15…

Also i noted there was some mutual fund buying going on in the shp…

ned to dig a bit deeper…

but the chart has a positive structure, with some short term, correction due…

Could people with knowledge of technical analysis take a look at Lupin, Glenmark and Sun and suggest a good entry point. I have been trying to understand the fundamentals of these companies and also been doing SIP in them, but don’t know when or where they would bottom out.

This is the daily chart of bajaj finance. The stock has broken out of a six month long consolidation pattern. Last when it broke out of similar pattern it gave a whopping 50% rally ignoring lot of market noise. Even the range breakout from 1550 to 1950 suggest a target of 2350 . It can be a excellent techno funda pick wherein the stock is expected to perform excellent in the core business as well. I am keeping 2050 - 2000 closing on a weekly basis as stop loss. Other technofunda picks I am tracking is Titan and indusind bank.

Regards

Divyansh

Titans charts are basically higher highs and higher lows. It has been outperforming the index as a whole for quite some time. Buying at RSI levels of 30-40 tends to give decent short term gains with decent margin of safety.

rushil decor on a downtrend post distribution, good chance of testing the yearly support…

Capacity addition in mdf segment[present capacity at 90pc utilization, expansion planned to 3x capacity]

and wpc vertical launch[jan 2018], together with massive underpenetration of both the commodities into the indian plywood alternative industry [visa via other developed markets] , raises a suspicion of the oncoming upcycle…

There is also a laminates division which has reached its optimum capacity[90pc]…

The debt to equity is 0.5…

There has been recent equity infusion by nonpromoters…

the stock is traking ar 32.86 price to earnings and 9 times the book value…

not cheap, was never cheap, given the concentration of big names both in the FPI and domestic institutions invested here…