Does it mean investors need to brace for more turbulence ahead?

From the article:

“SGX has numerous alternatives. SGX can go to a mom-and-pop index provider who makes a Nifty-like index: an index where 49 of the 50 stocks are the same as those in Nifty. SGX can shift to the MSCI India index, and MSCI can gently move closer to the Nifty composition.

If, somehow, SGX is prevented from having an effective exchange-traded Nifty product, the business will just go OTC.

Conclusion

Let’s not lose sight of what is going on. There is a trading venue that offers lower costs in investing/trading on Indian assets. We are discussing tools for protectionism through which the cost of participating in the Indian economy is driven up. This is not in India’s interests.

Our course of action should lie in solving the Indian policy mistakes of capital controls, financial regulation and taxation.”

Rgds

RR

2 Likes

I wanted some clarity around the cash and investments on the balance sheet of BSE. Please refer the calculations below.

From the March 2017 balance sheet (all figures in INR cr):

Non current investments: 1,491 (comprised of bonds and NCDs and debt mutual funds)

Current investments: 331 (comprised of debt mutual funds)

Current portion of long term investments: 170 (NCDs and debt mutual funds)

Cash and cash equivalents: 1,163

Bank balances other than cash and cash equivalents: 1,262

Total: 4,417

So that would mean that the cash and investments are more than the current market capitalization of BSE?

Others have mentioned much smaller amount of cash and investments? Am I missing something?

Even if some of the funds are earmarked for investor security, the fact remains that the cash is still with BSE and they can invest it in interest bearing investments?

1 Like

Q3FY18 Conference Call Notes

Consolidated PAT of 58.67 cr, yoy growth of 35%.

Accordingly, BSE proposed to buy back 15 lakh that is 1.5 million shares or more amounting to about 2.8% of the paid-up capital of the company at market price subject to maximum buyback price of Rs. 1100 per equity share subject to maximum buyback amount of Rs. 166 crore. The buyback has commenced on February 1, 2018.

INX

INX listed IFRC and NTPC green bonds. In talks with other PSUs.

BSE promoted India International Exchange at the GIFT to the Gandhinagar Gujarat had achieved the highest turnover of $405 million and the highest number of contracts 23,108 on January 16, 2018, to around 18. The India International Exchange has 26 active members as on date and over 100 various stages of memberships processes. As on date, 122 products have been introduced on the exchange for trading in commodity derivatives, equity derivatives and currency derivatives. The average number of contracts traded daily for the quarter ended December 31, 2017, was Rs. 6,319. India INX continues to be the market leader in this segment and the market share for the month of December stood at 71%.

INX has basically incurred a cost of around Rs. 12 crores in the entire period of nine months and that is in line with our expectation. We expect about Rs 2.5 crores to Rs. 3 crores spend on the Liquidity Enhancement Scheme side.

So in terms of the INX project, when we actually took the board approval last year from BSE, so we had put in a business plan wherein we are looking at a break-even period of between three years to five years.

So incidentally yesterday in the budget there have been quite a few SOPs which have been given to the IFSC exchanges, so which will benefit the INX. One of the big things was that in Singapore, foreign investors when they traded in derivatives, they didn’t have to pay any kind of capital gain, neither long-term or short-term. Now the same benefits have been extended from April 1, 2018, in the IFSC exchanges, so India INX will now get a level playing parity with Singapore. So now we can actually look at competing with them on a level playing basis.

LES - Liquidity Enhance Scheme

So on the India International Exchange side – this is Bala here so we have taken a approval from the board for about Rs. 4.42 crores for spending till April 15, but we are actually spending much lesser than that. So depending upon the competition and the situation and what the regulator does, at that time we will react to it.

I actually earlier answered regarding some budget announcements. If you will listen to the budget speech I think they have introduced couple of provisions. One is they have said that basically all the capital gains which will be applicable on our transactions in IFSC exchange will not be applicable in IFSC. So there will be no long-term capital gain, nor short-term capital gain on either derivatives or any depository receipt or any bond. And second move is they also said is that to make IFSC more competitive, the government is also looking at bringing a single financial market regulator there to be more focused to expedite things in the IFSC. So these are two moves which will help us in stemming the flow to Singapore Exchange and also this gives us a level playing field vis-a-vis SGX and other kind of markets.

BSE STAR MF

Introduced e-mandate which will reduce approval time to 3 days from 10 days.

Our mutual fund segment, which is an electronic online order aggregation platform for investment and redemption of units of mutual funds through broking members and authorized representatives including MFI and MFDs, has been showing superlative growth since past few years and continues to be another high growth area for BSE. This segment has seen growth of 163% on a year-on-year basis this year. The average monthly number of orders processed during the quarter ending December 31, 2017 were 14.7 lakhs as compared to 5.6 lakhs in the quarter ending December 31, 2016. BSE continues to be market leader in this segment and the market share for the quarter ending December 31, 2017, stood at 77%. On January, 10 BSE STAR MF received a record 3.1 lakh transaction on single day worth Rs. 685 crores. I am glad to inform you that BSE started receiving fees from some of the mutual funds for its services recently.

8 AMCs have agreed to pay us despite AMFI not wanting them to pay. Almost all of them are on BSE. And so, it’s ultimately – you are a member of a club, right. Member of a club, when club says, not pay to your milkman. And if you are unethical you will tell your milkman that I don’t want to pay you the cost, although I will drink your milk but I don’t want to pay you because my club has said, I will not pay you. And the agreement is between your milkman and yourself, not between milkman and your club. So it’s basically that’s the process in which some people have said that okay, we will

become unethical and if you drink the milk from you, we’ll pay you for the milk, that’s how it is happening, right?

AMFI does protest every day, but this eight guys somehow have decided one of the reason seems to be that when we were doing IPO probably we were 8% on the market, today we seem to be 20% of the market. And probably as for the indications, we are probably 50% of the new customers coming in. So that gives us some sort of level playing fields so to say against people who want other people to act unethically.

We have slab based charges, so if a fund sort of transfers less number of orders through us, then we charge them say, Rs. 25 or Rs. 30 per transaction. And if it’s very large it could down to Rs. 6 per transaction. So it’s not an exorbitant number, it is basically saving them close to Rs. 200 to Rs. 300 per transaction but somehow – sometimes clubs flex that just to look fit and stay secure.

Currently, we do around Rs.19 lakh transactions in a month, which is people tell me it’s close to 20% in terms of the value accounts of the overall sort of inflow and outflow of mutual fund industry, but I could be off the mark by some points.

BSE SME

BSE SME platform has 218 listed companies on its platform on January 15, 2018. 18 companies were listed on this platform during the quarter ended December 31, 2017, as compared to nine in the corresponding quarter in the previous year. BSE’s market share in SME segment stood at 66% as at December 31, 2017.

So SME basically in a sense the market share is declining, but absolute terms are increasing because NSE has also picked up well and that’s a good sign for the overall scheme of things. That absolute number will continue to expand going forward.

BSE Bond

During the quarter ended December 31, 2017, BSE’s platform for electronic book mechanism, BSE bond for issuance of the securities on private placement basis has completed 105 issues of bond raising Rs. 43,680 crores using BSE net platform. Total number of issues completed in this platform since July 1, 2016, is 766. The total amount through this platform raised has been more than Rs. 353,000 crore.

Equity Segment

In the equity segment, the average daily turnover grew by 57% from Rs. 3,042 crores in the quarter ending December 31, 2016 to Rs. 4,781 crore in the quarter ending December 2017. Further the average number of trades grew by 3% from Rs. 15.5 lakhs in the quarter ending December to 15.01 lakhs in the quarter ending December 31, 2017.

Currency Derivatives

The average daily turnover in our currency derivative segment grew by 38% from Rs. 12,588 crore to Rs. 17,999 crore in quarter ending December 31, 2017. BSE’s market share in currency derivatives segment for the quarter was 45%, and in the month of January 2018 it was more than 50%.

We are directly into organized what I called standardized market, so what remains OTC may still remain, but some of that overflows into the organized market like ours and that is true internationally, so most transactions on – in terms of values may happen on OTC basis, but many of them are then reflected on to the organized markets because of the ability or need for agent by the people who are giving those transactions to their customers, that is largely banks and others, so that’s how this business works internationally.

New Initiatives

Marketplace Tech Infra Services, a 100% subsidiary of BSE signed an MOU with Thomson Reuters to offer value-added service to its members. Through this partnership, BSE members will be able to avail Thomson Reuters-powered solutions proTRade, i3 Algos and Bracket Order on mobile device as well as dealer terminal.

Earlier in 2017, BSE deployed BEST, BSE’s electronic smart trader, a robust state of the art hosted trading solution built on Thomson Reuters’ Omnesys NEST for BSE members and customers and trading segment of NSE for equity derivatives, currency and other segments.

SEBI announced that the country would have unified action regime from October 2018. In line with preparing ourselves to launch commodity derivatives transaction, BSE started to hold mock trading session for such products recently. Trading in commodity derivatives shall be conducted on the BOLT Plus trading platform, our new generation trading system.

Universal Exchange

Basically we plan to start as soon as we are allowed which looks to be possible earliest by October 1. We have prepared ourselves for last two and a half years and have been waiting and now that it is looking possible, we have started doing the mock trading and it will give people hands on understanding of how it’s going to happen in BSE, but we don’t have any idea of what kind of numbers that will be attracted to BSE vis-à-vis, other exchanges. In terms of growth we do not currently see any possibilities, but if any opportunity arises, we’ll have to evaluate based on the merit of the case and we may have to figure out, but currently we have not on the lookout.

Our current strategy is to run the new markets on our own technology platform. So our marginal cost of implementing technology for the commodities is going to be pretty close to nil, going forward. At the same time to attract volumes we might have to basically do marketing and sales. And as of when we’re getting to that business that framework may evolve, but it is safe to say that we may end up spending Rs. 5 crore to Rs. 10 crore a year on the marketing and sales for commodities for next three, four years going forward.

And if you get a good traction then we maybe able to recover our money and make more profits out of that.

On being asked whether we will introduce a LES and will charges be introduced, mgmt. said, when the opening comes closer we will have to decide what is allowed. These are highly, highly, highly regulated activities. So in certain area they allow us to do a liquidity enhancement scheme, certain areas they don’t, and so we’ll have to figure out what is possible, what is not and also what is commercially prudent and then we would move around according to that.

How do we plan to attract clients?

So we think we have a good technology. We think we have similar types of number as so called large player and so effectively our cost of technology also very low compared to incumbents, and we think the current incumbents don’t have great technology. And they are also struggling with the technology providers. Put together this is one area where we think we are able to score even in currencies where there are two incumbents.

And today we are larger than both incumbents. And so we think it’s possible to do and so technology seems to be our main differentiating factors and our distribution framework of stock brokers across the country is going to be another differentiating factor and they’re now sort of ability to trade on easily on BSE because there use to be a technology might attract them to BSE compared to other incumbents currently trading this market.

What is the technological advantage?

Currently our scale of operations is possibly one of the largest. We can handle 500,000 order per second. And so those kind of orders requires – basically they require the speed at which we offer this kind of scale is around 6 microseconds. In one second there are 10 lakh microseconds, 1 million. So we have response in 150,000 per second is the fastest in the world. Nearest fast exchange is around 60 microseconds at Singapore. And so we are severely fast, severely scalable. Why it is required? Because in auctions market… And so literally you have 60 orders getting, 60 or 120 orders getting canceled and new orders getting in. And if the software of a company or an exchange is not tuned for that, then it becomes very difficult to handle for them options business.

To give you an example, suppose you go to – I mean you must be familiar with Bombay, so if you go to say Phoenix Mills, which is house to Big Bazaar. Every – or at least they are getting 2 lakh customers or 2 lakh walk-ins in a weekend and 40,000 people buy, that means orders to trade ratio is around 5:1, 2 lakh by 40,000. Imagine suddenly on a weekend 2 crore people come and 40,000 people buy, that is the order to trade ratio has become 5 to 500, when your income remains still the same.

So you’ll have to change the entire structure of the Phoenix Mills otherwise it will stumping, right? And that is what happens in a technology also, our stock exchange when will start trading auctions, that you are used to 5:1 or 2:1 or 3:1 kind of order to trade ratio in futures and stocks. And suddenly you’re going to 1,000:1, 2,000:1 kind of numbers. And for that the number of computers required, the speed required on different caliber, right? So that’s broadly – although not exactly, but broadly an explanation of why the technology is slightly different at that scheme.

This will be using the existing BOLT Plus system, our marginal cost of setting up the commercial market will be close to zero.

The clearing operation is reasonably capitalized, so there is no expected marginal increase from our side to be paid there at least in the beginning. We will start with non-agri commodities.

Market share expectations in 3-5 years in commodities?

Usually we don’t target anything, we just want high. So we will have the base technology, base systems, lowest cost and hope people come in, and to give you a perspective on currencies people were asking us and of course they’re all laughing on the block in front of us, I think whatever these guys say or not because they have been pretty much a failure, but somehow over three years, we’ve become larger than NSE. And let’s hope we look at – we don’t predict, we don’t anticipate, we just do hard work.

Mock Trading Response

Our technology is actually used by them every day for the currencies and other equities and other areas, so they are comfortable with that it just how the trading in commodities will look like. I mean how to setup a contract and stuff like that which again were used in currencies also and equities also. So it’s not very different or in fact it’s not different at all.

And so they are going to have on the same screen even commodity is coming up. So whoever gets the time in the evening, ends up logging in and I can you tell you that they maybe trading infinite amounts but those infinite amounts are actually of no consequence because they’re fake. Maybe mock trading, if you take those things seriously then it’s – what I call is it’s like Bitcoin being taken as a currency.

Market Expansion in Commodities

It should expand, but remains to be seen, I mean, these are all hopes because of which what tries to get into that business, but it should. We have seen it in currencies, we have taken the market share, but other peoples absolute numbers have not gone down much, so overall there has been increase.

LTCG Introduction

It reduces our compliance and operational cost drastically because earlier problems of tax evasion where we post on BSE because it was not capped – if you cap the share for more than a year then the capital gain tax was exempt. So lot of small company prices were moving up and each time anyone claimed a capital gain tax exemption, BSE was blamed by everyone including the CBDTs, Central Board of Direct Taxes officers who were assessing and they were sending us lot of queries, even now every day we would be answering at least 50 to 100 queries from income tax on variety of customers.

And so that’s – probably once they start paying, this entire cost should come down because then the department doesn’t have to take us as BSE as people who are encouraging such tax revision methods and we think it’s going to be a great relief to us going forward.

Whether LTCG will increase trading volumes is anyone’s guess, what the future brings is completely unpredictable. AC has no view on this.

I mean, STT going – STT is the largest friction that is there for last so many years and if STT goes away, basically helps in the liquidity and overall industry,

Growth Expectations

On being asked what are the growth drivers BSE mgmt. is looking to ensure 25-30% or more CAGR in next 3-5 years.

We have not given anyone any indication that there’s going to be CAGR of X%, or Y% or Z%. So that might be sort of a conclusion you might have derived out of your own imagination, but BSE has not such indication given to anyone.

Have 1600 cr of unencumbered cash on BS, a part of which will be used in buyback and dividend.

Interoperability of Clearing Corporations

This is basically an outcome of the K.V. Kamath Committee which was set up around five years back, which submitted their report around 1.5 years or two years back, and so these are all long-term processes and it’s not easy to predict actual implementation and them getting converted into regulations in a short time.

Basically interoperability is a standard practice now mandated by regulators in Europe, to some extent in U.S. and to some extent the Hong Kong-China interconnect and all are working on the similar principles. There are models available working which are working well and so there are no apprehensions, but usually an income monopolist would run a fix, and the non-monopolist, the smaller ones will want to average. And so depending on who is able to sort of convince the regulators and how the regulators see the situation, things get sort of implemented or not.

De-listings

These companies which we’ve delisted were not paying listing fees for more than seven years and they had been suspended, that is they were not even trading and they were not compliant. So effectively they were not spending, I mean, giving us any revenues nor any kind of trading at all.

Market Share loss in Equity

So basically I’ll tell you, there are around nine or 10 markets we work on. One of them is equities. Other is equity derivatives, third is IPOs. Fourth is listing. Fifth is offer to buy. Sixth is offer to sell. Seventh is SME. Eighth is mutual fund distribution through exchanges. Ninth is BSE bonds. Tenth is currency with derivatives. Eleventh is interest rate derivatives. And there are probably two or three more. Other than equity and its derivatives we are actually gaining market share in almost all areas. Okay, or we have very large incumbent if we are not getting the market share. Out of 12, 11 or 12 areas you got one and you have made a statement which is correct in a way, but it is also just wanted to show reflection and saying back kindly look at all the areas and figuring out.

@kashif_1461 management states in concall that unencumbered cash is 1600 cr.

8 Likes

I think they are referring to cash and bank balances of 2,425 (1,163+1,262). Out of this amount, 1,600 is unencumbered cash.

But there are additional investments (in NCDs and MFs) amounting to 1,992. These investments can also be considered as cash equivalents.

From a valuation perspective both the cash and investments provide a downside protection. Even if I remove the encumbered cash, there are still cash and investments of 3,600cr on their balance sheet. And that still leave out the following:

- The core business

- 25% stake is CDSL

- International Exchange at Gift City

3 Likes

Hi Kashif,

Tried to do some digging into the FY17 and H2FY18 Balance sheet numbers. Sharing for the benefit of discussion here because I am not 100% sure if what my calculations reveal is the true unencumbered cash.

At the end of the post are the excel file with the calculations and the AR where I have highlighted the figures used. The excel sheet also contains the page numbers from which the adjustment figures have been taken.

On the asset side of the balance sheet I found some 1570 cr of funds which have been earmarked. Pg 127 of the AR defines these funds as representing deposits, margins etc held for specific purpose.

So in the middle table in the excel I simply calculate for cash that is left after these earmarked funds.

Now on the balance sheet I also found 1945 cr of current other financial liabilities and other current liabilities. These are significant amounts, having a look into their footnotes, I found that these are mainly liabilities arising from clearing and settlement segment, namely, deposits from clearing banks, deposits and margins from members and settlement obligation payable.

Now a portion of these liabilities have already been earmarked in investments and current accounts as the sub-footnotes mention. Therefore when calculating these liabilities I remove these earmarked funds so as to not double count these earmarked funds.

From these calculations, the unencumbered cash comes out to be 1271 cr & 1080 cr in FY17 and H2FY18 respectively.

Now as I said before that I am not 100% certain that this is the true unencumbered cash because the earmarked funds in assets and liabilities do not match. I am not even sure if they should match.

If anyone cares to have a look/perform their own calculations, please do. Would be happy to be proved wrong.

BSE Cash.xlsx (10.6 KB)

PS: AR FY17 file size was too big to be uploaded here.

1 Like

Thanks for this Abhinav. From your calculations, the net cash after earmarking comes to 2849cr at the end of FY17. I would take this as the cash and investments for my purpose. I would not further subtract the liabilities from this.

Because although these are listed as liabilities on the B/S, but are they real liabilities? Meaning does the company really have to give this cash back to its creditors? I dont think so. Because you can see from the balance sheet that these liabilities have continued to accumulate over the last 3 years. It is in the nature of the business that these liabilities will always be there. Its like advances from customers for a good real estate company. These are listed as liabilities but are not real liabilities. These are in fact quasi-equity as Warren Buffet has argued for the case of Blue Chip Stamps.

Finally, from our purpose what is important is what is the cash which the company can deploy in its operations or for for any potential acquisitions. From note 14.1 and 14.2 in the annual report, it seems like restricted cash is only 53cr (out of the earmarked cash of 1543cr). The remaining amount can be used for business purposes. But I may be wrong in interpreting this. Anyway i look at it, the minimum cash which is unencumbered and can be used for business operations is 2848cr or possibly more.

Kashif, you could be right about the liabilities never actually coming fully due. Will have a look back 10 years or more to see how this goes. You are right that 53 cr of earmarked funds restricted for specified purposes which are mentioned in their IPO DHRP.

While these liabilities may never come due, the funds balancing these liabilities will have to remain on the balance sheet in the form of liquid securities. We may have different opinions on this but ultimately what matters is how the management views this situation as.

I believe when Mr. Ashish Chauhan in the Q3FY18 con call said we have 1600 cr of unencumbered cash he meant that is what can be used for operations, capital allocation etc. This would obviously mean they are not treating cash against these liabilities as unencumbered.

The funds against the liabilities will stay on the B/S providing investment return for the foreseeable future.

We may agree to disagree here, it was a fun exercise to understand an exchange’s balance sheet.

Cheers.

Disclosure - Invested.

I would be keen to understand how the figure of 1600cr is arrived at by the management. Can you write to the investor relations seeking a response. I’m not yet invested, hence cannot do that.

In addition, there is no regulation that requires the company to maintain cash in the form of liquid securities to balance the short term (or long term) liabilities. I’m not sure if there are any specific regulations with regard to exchanges.

And now the exchanges and SEBI are sure to be running helter-skelter, sadly realising they can’t take monopolistic decisions. This strongly worded press release is indeed very insulting for them.

The best we can hope is to accumulate BSE if it falls over next few days and becomes a no-brainer

Rgds

RR

Yeah, I am waiting for the FY18 to finish, and AR to arrive before contacting them. We will get audited financial statements and would also see the cash impact of CDSL sale. We do not have the earmarked fund quarterly figures to build a model on.

About the regulatory requirements to maintain cash for liabilities, I wrote about the nature of these liabilities in my 1st post. When the cash is arising out of such obligations, the usage of cash will surely be regulated.

“I found that these are mainly liabilities arising from clearing and settlement segment, namely, deposits from clearing banks, deposits and margins from members and settlement obligation payable.”

These are similar to liabilities of an insurance firm, the premiums they receive to insure the risk, they keep this cash as investments on their books and earn returns on this float, but I believe IRDAI mandates the asset allocation of such encumbered cash.

Similarly, a float could be accumulating (as you have suggested) in the exchange business model, as deposits and margin paying clients increase in both number and value. Although on a smaller scale compared to insurance businesses.

2 Likes

SEBI the regulator has pulled the plug its not the Bse or Nse who wanted to cancel the licence. The Indian regulator is the one doing the arm twisting

It is also understandable as every country want to make themselves a financial hub. India gains nothing by making Singapore a financial hub. Makes more sense to give preferential treatment to the GIFT City.

1 Like

What is the risk of float income getting adversely impacted?

This is the excerpt from conference call conducted on May 5, 2017. Company’s management indicated about paying interest on members’ deposits. Any idea, on what amount such interest is to be paid?

3 Likes

Some useful updates on business from the man himself.

Rgds

RR

BSE is making all efforts towards commodities platform. I hope at least one of their new initiatives (Commodities, Mutual Fund, Insurance, International Exchange) will become big enough to take BSE to next level.

Disc: Invested.

2 Likes

This is one very interesting information. I can see that the trend is continuing from the time @azardeen posted this first about 15 days back. Let see if this can become a trend going forward. I would say as Indian market matures more and more players will start spreading the trade between NSE and BSE(simply for the purpose of mitigating risk of possible technological glitch - remember the day when NSE had to call off nearly a full days trade last year). It would be interesting to know the real reason behind this bridge.

Disclosure: Invested in BSE and adding on every dip!

AJ

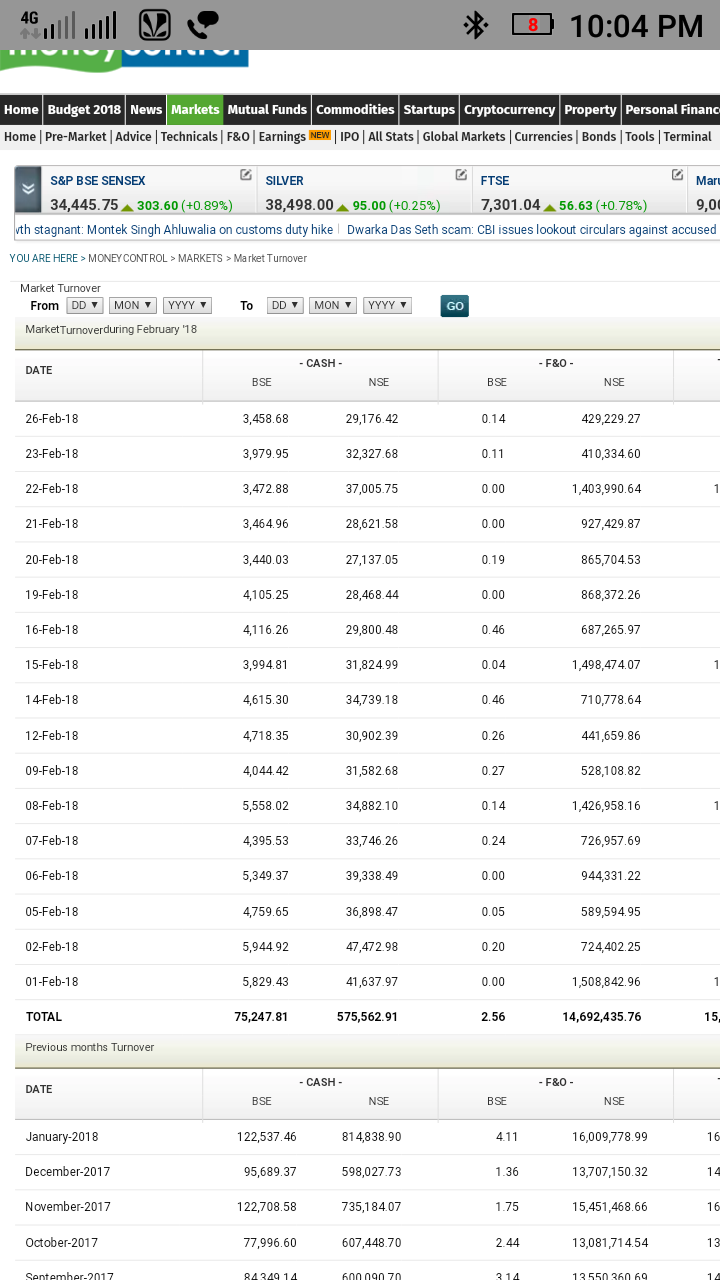

I have seen volumes on money control but is showing difference in data which the website link you have mentioned.

Thanks for pointing. Now I checked in BSE website itself. It shows same data as moneycontrol. I am not sure why way2wealth website shows different figure.

https://www.bseindia.com/markets/keystatics/Keystat_turnoverequity.aspx

What is the expected dividend yield for BSE? Moneycontrol shows 3.5% but I believe that is because of the 23rs dividend last year. Was that a one-off dividend due to CDSL stake sale? 3.5pc is very attractive but I believe its not a correct reflection of expected dividend yield.