Guess, with interest rates hardening, it would have MTM loss on bond/fixed income securities portfolio.

Further, considering markets are correcting, it affects transaction fee income from Equities and F&O. And obviously, sentiments are down overall in markets with mid-caps and small cap correction, leading to correction in all stocks.

Ian Cassel posted this on Twitter which relavent to question you asked.

“Few things test your conviction like falling stock prices.”

Check out @iancassel’s Tweet: https://twitter.com/iancassel/status/1039867114495127553?s=09

1 Like

This think most of the reasons you mentioned are already factored into the price , worst profits will dip to 150Cr.

I bought it considering the liquid fund kind of return (7-8% if nothing of its hidden assets play out) in 2017 when everything was expensive … Everything is priced as per DCF as per interests rates by RBI.

now on raising interest rates environment stocks will adjust.

so, it was a bad decision in think overall in expensive market. Now my only hope is the hidden assets to play out.

I still believe the returns going to be around 7-8 % in the stock very safely. I would say don’t look at the price, look at the dividend yield and the business overall.

BSE has been improving under new CEO, Lets hope INX plays out real good.

I am going to double down at Rs 650 ( so, there is a short term painful hope inside me for further correction ).

2 Likes

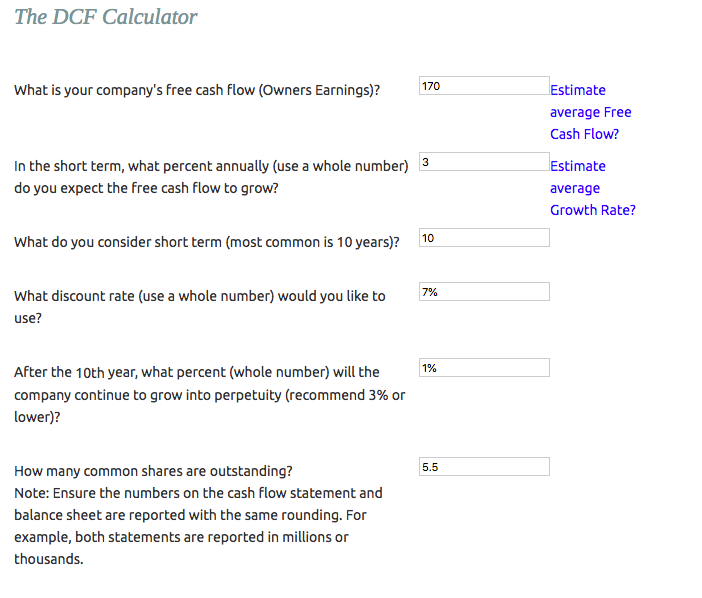

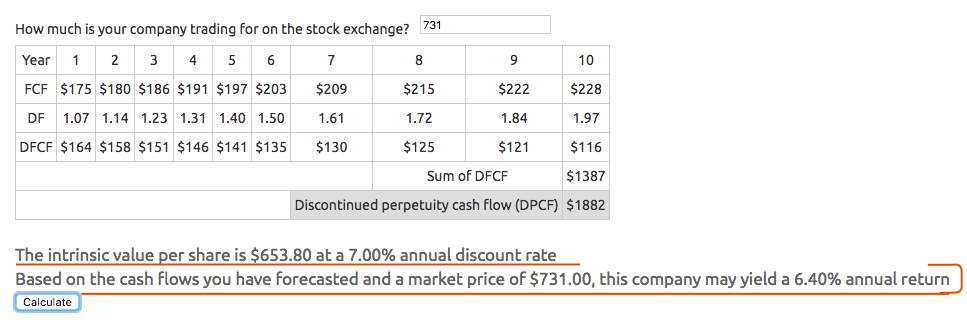

The intrinsic value coming out to be around - Rs 650 /- share

Figures are in Rs Cr.

My assumption -

BSE will keep making Rs 170 Cr /- Net profits. ( Cyclically averaged )

3% growth for 10 years.

Discount rate 7% (GOI bond - This is going up - Stock will adjust)

Used this Calculator - http://buffettsbooks.com/howtoinvestinstocks/course3/intrinsic-value-formula.html#sthash.v5XjfDFM.FoygrH8B.dpbs

So, with so much of conservative assumptions i see investors at current MCap should make minimum of 6.4% returns. If hidden assets won’t click then this may not be satisfactory return for an stock market investor.

Let me know your views on it.

In 2013 they have made as low as Rs 109 Cr /- , So its if one takes 150 Cr /- as average profits per year for next 10 year then intrinsic value going to be around Rs 570-590 / share.

I don’t think BSE is screaming buy even at today’s Mcap.

What folks think here about the value at today’s mCap ?

Thanks,

Amit

1 Like

My 2 cents - With all this DCF discussion here, people are missing amazing optionality elements which Ashish Chouhan is trying to bring to BSE.

He talks about revenue streams for next 20 years. Emphasizes that next 20 years will be a lot different than past 20 yrs for exchanges. We should not forget that this is the guy who built derivative business at NSE from scratch in early 2000s! He knows this game inside out and is a real industry veteran. He is incubating ideas which would result is much larger revenue stream for BSE over next decade.

In this interview he gives passing reference to blue ocean strategy, where returns are very very large for very little investments due to limited competition.

There can be arguments for and against BSE due to its cyclicality and being seen as a distant second to NSE in equities, but then BSE is now not just equity. In fact, equity will be one of the many revenue streams for BSE 3-5-7 years down the line.

Disclaimer: Invested.

23 Likes

Superb Interview. Thanks for posting.

Hi Mridul,

Very nice perspective.

Thank you for sharing the interview link. Extremely engaging.

Regards

Disc: Invested

I wish investing to be this easy , just agreeing to the prospective of promoters. ( i avoid meeting to the promoters)

Throw me DATA ? I would love to listen how big M.F Start going to be. My calculations earlier shows not as big as Rs 20 Cr in 4-5 year.

Tell me why INX going to be hit and in how much time ?

Tell me why EBIX going to be hit ? in how much time ? what will be the revenue share model with EBIX ?

how big EBIX and INX going to be ?

I am looking for rough numbers from community members.

I am invested in BSE. There are two reasons i am asking these …

- Should we double down now ?

- Should we hold ?

- Should we just sell it as its going to be yielding just 7% for years to come .

Thanks,

Amit.

Any idea what’s causing the 5%+ spurt in price today with a strong volume?

Couldn’t find any news per se

now finally investors are going defensive … selling HDFC twins and buying high dividend yielding stocks with stable businesses

1 Like

Let’s assume we get the answers like how big star MF is or how INX or EBIX going to be and also in how much time as well as revenue share model then won’t the stock price start reflecting same and it will start trading at 30 40 PE. In investing either we have all the data or we have discount in the price. I have yet to see a stock where both are obvious.

Though that is my personal way of seeing things and I might be wrong.

5 Likes

your edge will always be analyzing out all these probabilities better than anybody, At least one should think about how much future growth expectation is already built into the prices.

you are kind of talking about efficient market theory , stocks should price in all the available information but most of the buyers and sellers in market are emotional just couple of days ago BSE was all time low and now suddenly 6% up in falling market.( if these movements are not emotional then what it is )

but in long run how all these star MF is or how INX or EBIX going to pan out going to decide the destiny of stock price.

we can bring collective intelligence here to gauge how big each of them could become ( best case scenario ) to what if nothing will click …

If nothing will click then stock is trading expensive today for sure but generally reality lies in between.

Agree. Warren Buffett once said, Investing is art of making decisions before all FACTS are IN. This echoes ur view.

2 Likes

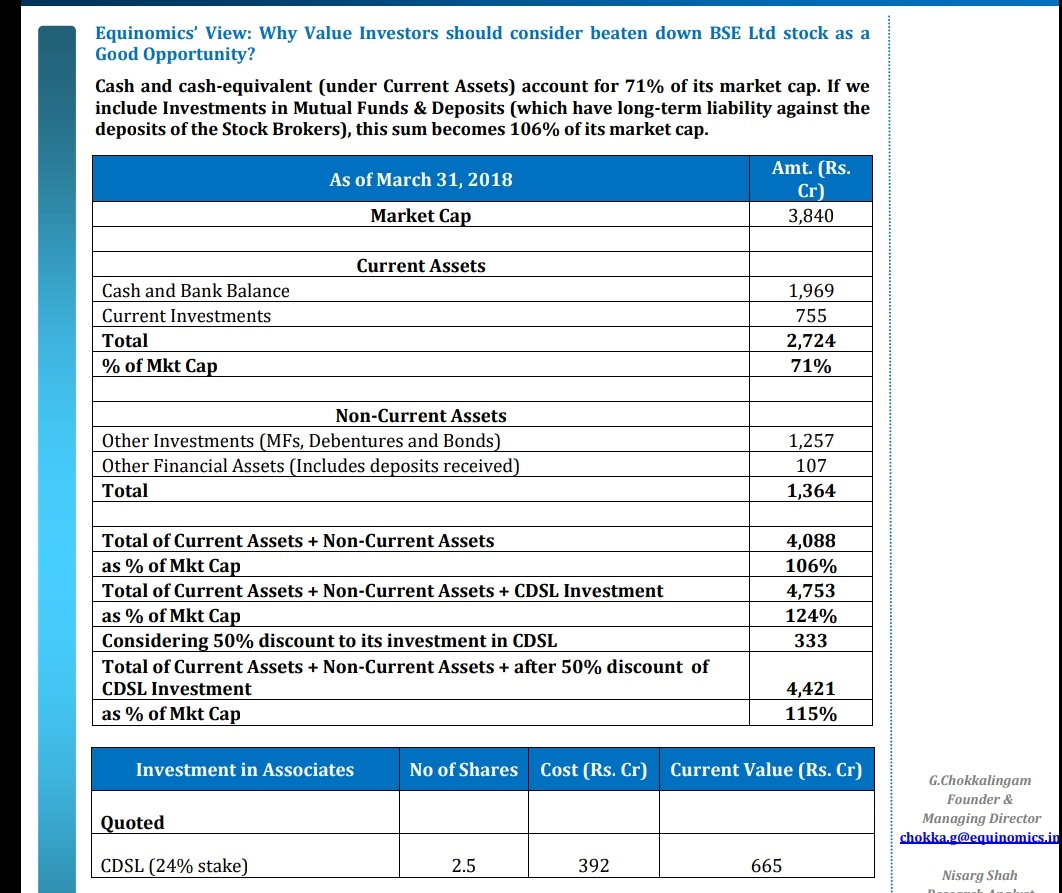

Have not verified independently. But this is the note from eqinomics with some facts about BSE.

Disc.

- Invested in BSE

- Subscribed to Equinomincs - Morning Insights

- This is not a regular note; Which is only for paid subscribers. Part of this for benefit of others.

2 Likes

“The more the cash that builds up in the treasury, the greater the pressure to piss it away.” - Peter Lynch.

Companies like CSL and BSE have massive cash investments in their books. But that does not provide investors with any kind of Margin of Safety. Cash and cash equivalents are just another part of a company’s value.

It’s in the nature of companies to hold cash in the absence of investment opportunities. But holding cash that’s in excess of 30% of the Market Cap is alarming and indicates an acute lack of reinvestment opportunities.

3 Likes

Dear sir,

Agreed. But with my limited understanding

Excess cash & Subdued growth (not path beating) are inherent part of any exchanges.

Opportunities to deploy cash is limited by the regulatory requirements itself.

Excess cash, on periodic basis can be transmitted to shareholders benefit.

1 Like

No , They didn’t talk about how much that cash is Unencumbered ?

Actually some of the Cash ( i think may be 40-50% or so … double check ) is encumbered , they received as a float from from brokerages, listed companies etc as membership fee that they cannot spend …

forget the dream of cash comping back to you … i did a analysis they can return 1000Cr of cash if they want to comfortably.

Most of it was earned through sale of CDSL … that market was expecting could be returned to shareholders but they decided not to bcoz of INX and future projects they are betting on. .

Instead of liquid fund its a good bet as you mentioned in ur post … bcoz those cash assets yielding the same in Gov Securities.

but r u in equity to earn 7% is the main question ?

1 Like

Around 1000 Cr. is “encumbered” cash - regulatory capital. For FY18, BSE has paid a handsome dividend, and bought back shares to the tune of 166 Cr. (maximum permitted, I think).

Disc: Invested; views biased.

2 Likes